Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDistributional neural networks for electricity price forecasting

Jul 06, 2022

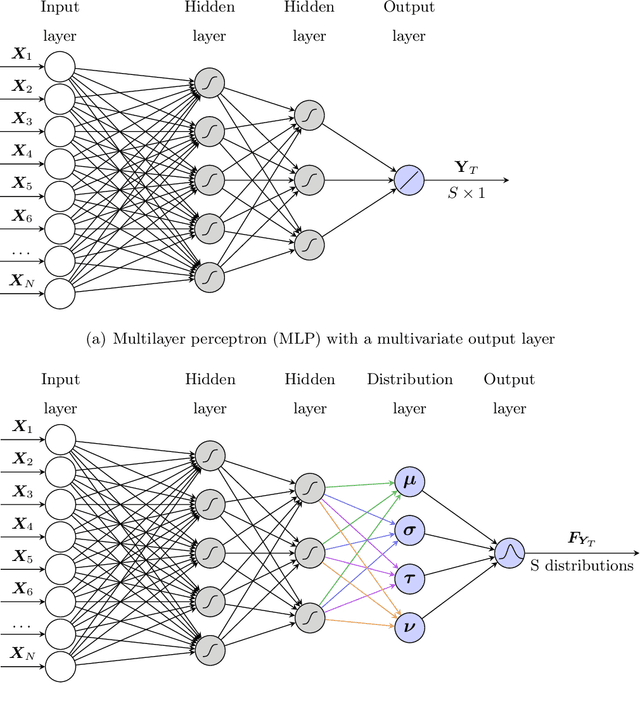

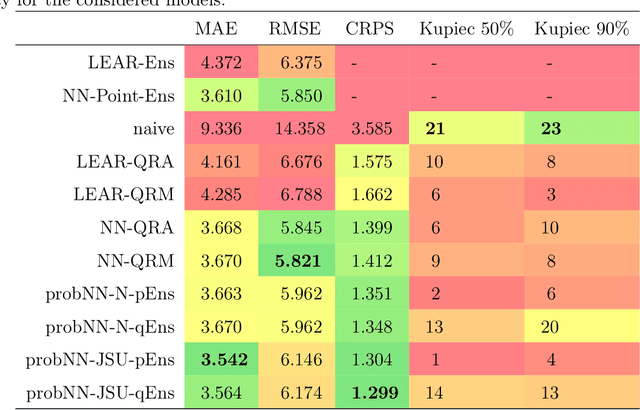

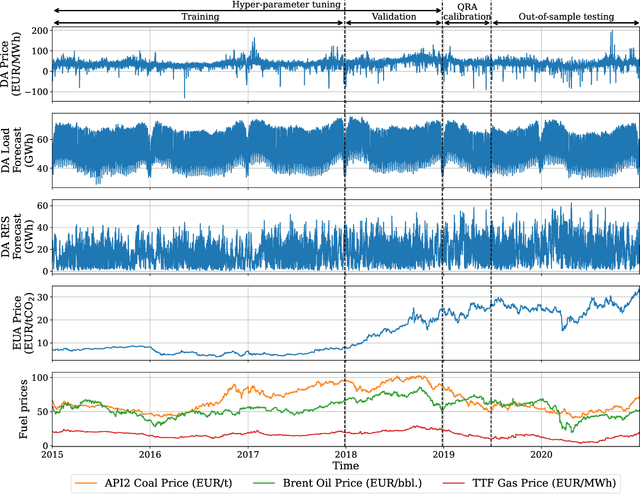

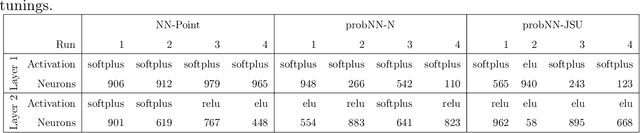

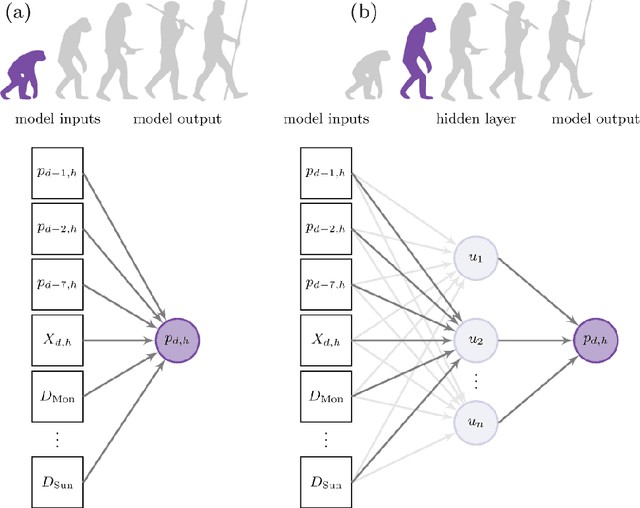

We present a novel approach to probabilistic electricity price forecasting (EPF) which utilizes distributional artificial neural networks. The novel network structure for EPF is based on a regularized distributional multilayer perceptron (DMLP) which contains a probability layer. Using the TensorFlow Probability framework, the neural network's output is defined to be a distribution, either normal or potentially skewed and heavy-tailed Johnson's SU (JSU). The method is compared against state-of-the-art benchmarks in a forecasting study. The study comprises forecasting involving day-ahead electricity prices in the German market. The results show evidence of the importance of higher moments when modeling electricity prices.

Electricity Price Forecasting: The Dawn of Machine Learning

Apr 02, 2022

Electricity price forecasting (EPF) is a branch of forecasting on the interface of electrical engineering, statistics, computer science, and finance, which focuses on predicting prices in wholesale electricity markets for a whole spectrum of horizons. These range from a few minutes (real-time/intraday auctions and continuous trading), through days (day-ahead auctions), to weeks, months or even years (exchange and over-the-counter traded futures and forward contracts). Over the last 25 years, various methods and computational tools have been applied to intraday and day-ahead EPF. Until the early 2010s, the field was dominated by relatively small linear regression models and (artificial) neural networks, typically with no more than two dozen inputs. As time passed, more data and more computational power became available. The models grew larger to the extent where expert knowledge was no longer enough to manage the complex structures. This, in turn, led to the introduction of machine learning (ML) techniques in this rapidly developing and fascinating area. Here, we provide an overview of the main trends and EPF models as of 2022.

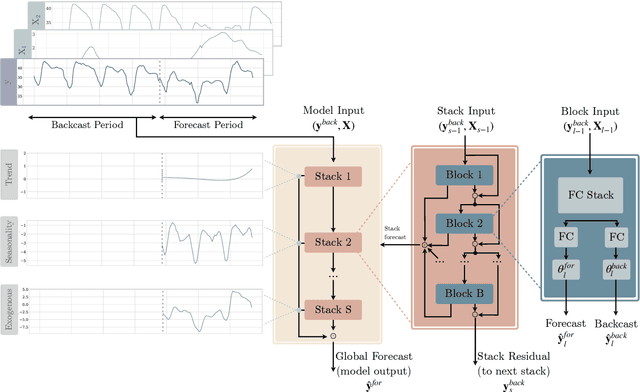

Neural basis expansion analysis with exogenous variables: Forecasting electricity prices with NBEATSx

Apr 23, 2021

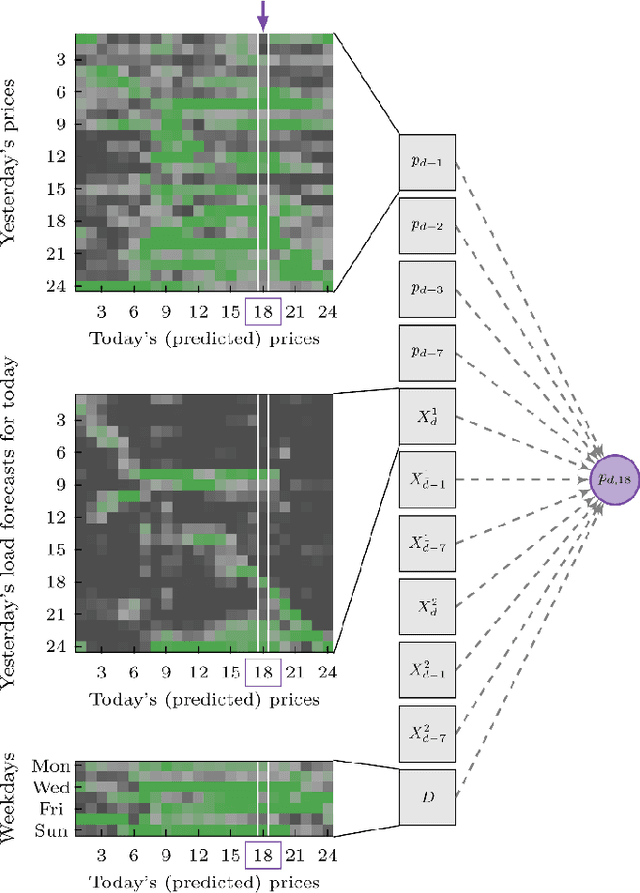

We extend the neural basis expansion analysis (NBEATS) to incorporate exogenous factors. The resulting method, called NBEATSx, improves on a well performing deep learning model, extending its capabilities by including exogenous variables and allowing it to integrate multiple sources of useful information. To showcase the utility of the NBEATSx model, we conduct a comprehensive study of its application to electricity price forecasting (EPF) tasks across a broad range of years and markets. We observe state-of-the-art performance, significantly improving the forecast accuracy by nearly 20% over the original NBEATS model, and by up to 5% over other well established statistical and machine learning methods specialized for these tasks. Additionally, the proposed neural network has an interpretable configuration that can structurally decompose time series, visualizing the relative impact of trend and seasonal components and revealing the modeled processes' interactions with exogenous factors. To assist related work we made the code available in https://github.com/cchallu/nbeatsx.

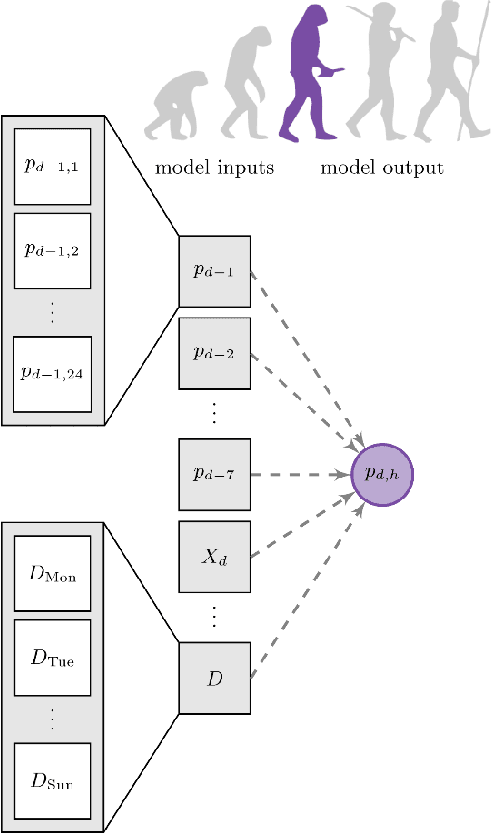

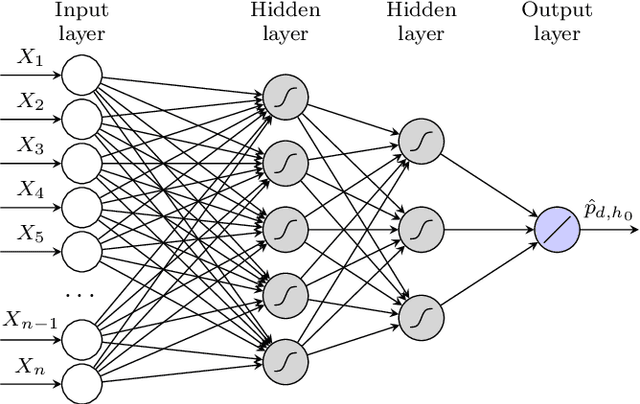

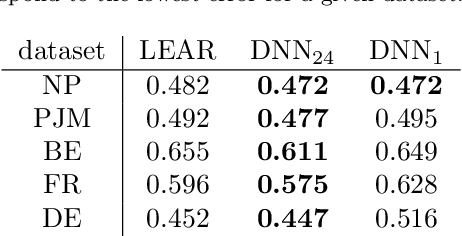

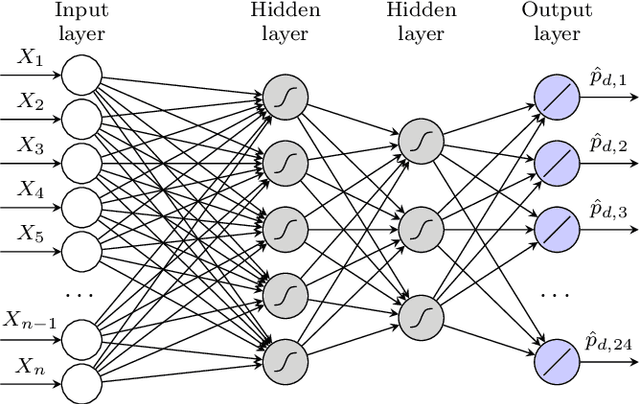

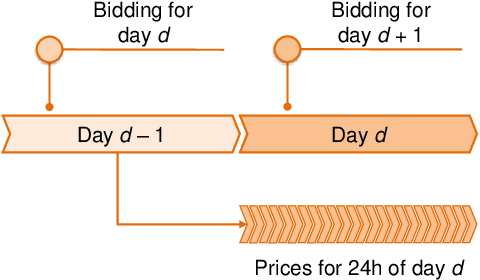

Neural networks in day-ahead electricity price forecasting: Single vs. multiple outputs

Aug 18, 2020

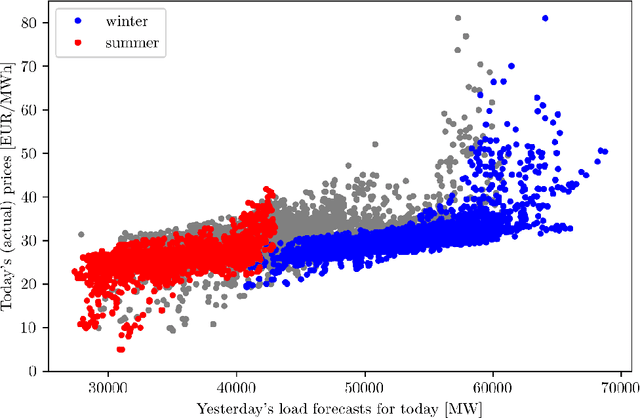

Recent advancements in the fields of artificial intelligence and machine learning methods resulted in a significant increase of their popularity in the literature, including electricity price forecasting. Said methods cover a very broad spectrum, from decision trees, through random forests to various artificial neural network models and hybrid approaches. In electricity price forecasting, neural networks are the most popular machine learning method as they provide a non-linear counterpart for well-tested linear regression models. Their application, however, is not straightforward, with multiple implementation factors to consider. One of such factors is the network's structure. This paper provides a comprehensive comparison of two most common structures when using the deep neural networks -- one that focuses on each hour of the day separately, and one that reflects the daily auction structure and models vectors of the prices. The results show a significant accuracy advantage of using the latter, confirmed on data from five distinct power exchanges.

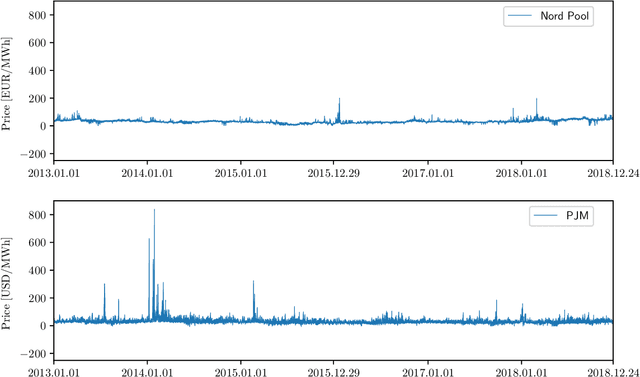

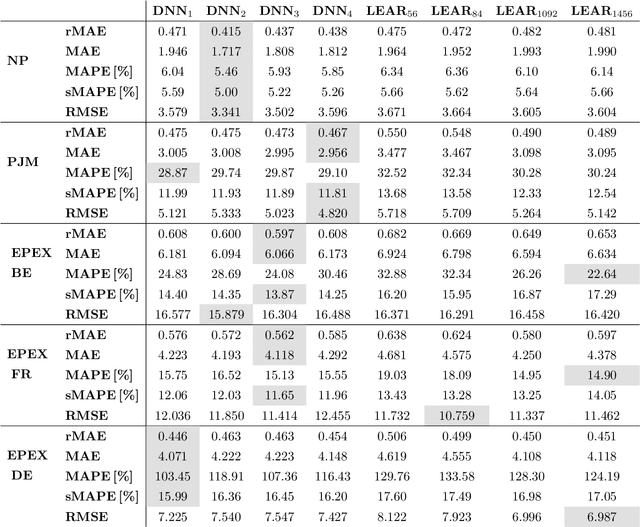

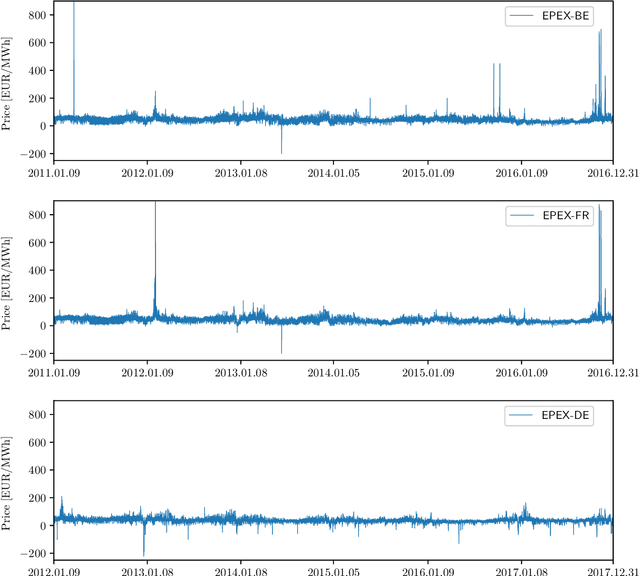

Forecasting day-ahead electricity prices: A review of state-of-the-art algorithms, best practices and an open-access benchmark

Aug 18, 2020

While the field of electricity price forecasting has benefited from plenty of contributions in the last two decades, it arguably lacks a rigorous approach to evaluating new predictive algorithms. The latter are often compared using unique, not publicly available datasets and across too short and limited to one market test samples. The proposed new methods are rarely benchmarked against well established and well performing simpler models, the accuracy metrics are sometimes inadequate and testing the significance of differences in predictive performance is seldom conducted. Consequently, it is not clear which methods perform well nor what are the best practices when forecasting electricity prices. In this paper, we tackle these issues by performing a literature survey of state-of-the-art models, comparing state-of-the-art statistical and deep learning methods across multiple years and markets, and by putting forward a set of best practices. In addition, we make available the considered datasets, forecasts of the state-of-the-art models, and a specifically designed python toolbox, so that new algorithms can be rigorously evaluated in future studies.