Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeCost-aware Stopping for Bayesian Optimization

Jul 16, 2025In automated machine learning, scientific discovery, and other applications of Bayesian optimization, deciding when to stop evaluating expensive black-box functions is an important practical consideration. While several adaptive stopping rules have been proposed, in the cost-aware setting they lack guarantees ensuring they stop before incurring excessive function evaluation costs. We propose a cost-aware stopping rule for Bayesian optimization that adapts to varying evaluation costs and is free of heuristic tuning. Our rule is grounded in a theoretical connection to state-of-the-art cost-aware acquisition functions, namely the Pandora's Box Gittins Index (PBGI) and log expected improvement per cost. We prove a theoretical guarantee bounding the expected cumulative evaluation cost incurred by our stopping rule when paired with these two acquisition functions. In experiments on synthetic and empirical tasks, including hyperparameter optimization and neural architecture size search, we show that combining our stopping rule with the PBGI acquisition function consistently matches or outperforms other acquisition-function--stopping-rule pairs in terms of cost-adjusted simple regret, a metric capturing trade-offs between solution quality and cumulative evaluation cost.

The Gittins Index: A Design Principle for Decision-Making Under Uncertainty

Jun 12, 2025The Gittins index is a tool that optimally solves a variety of decision-making problems involving uncertainty, including multi-armed bandit problems, minimizing mean latency in queues, and search problems like the Pandora's box model. However, despite the above examples and later extensions thereof, the space of problems that the Gittins index can solve perfectly optimally is limited, and its definition is rather subtle compared to those of other multi-armed bandit algorithms. As a result, the Gittins index is often regarded as being primarily a concept of theoretical importance, rather than a practical tool for solving decision-making problems. The aim of this tutorial is to demonstrate that the Gittins index can be fruitfully applied to practical problems. We start by giving an example-driven introduction to the Gittins index, then walk through several examples of problems it solves - some optimally, some suboptimally but still with excellent performance. Two practical highlights in the latter category are applying the Gittins index to Bayesian optimization, and applying the Gittins index to minimizing tail latency in queues.

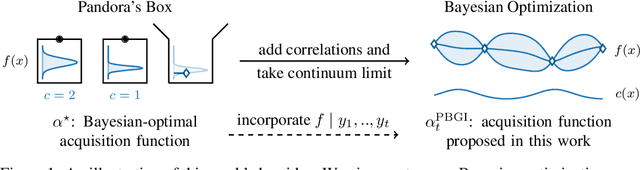

Cost-aware Bayesian optimization via the Pandora's Box Gittins index

Jun 28, 2024

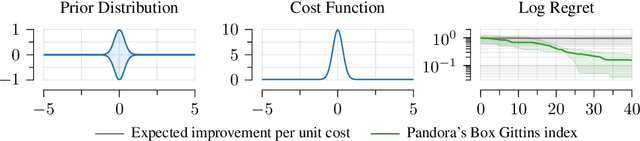

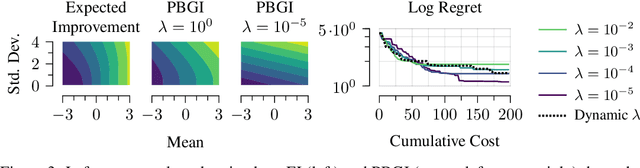

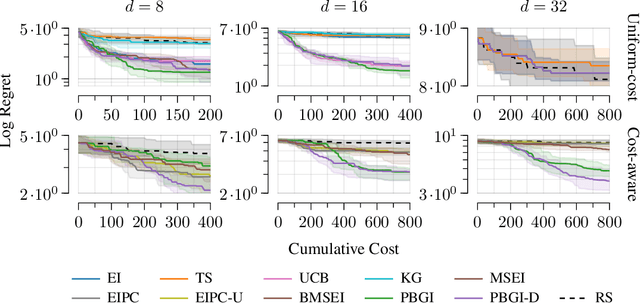

Bayesian optimization is a technique for efficiently optimizing unknown functions in a black-box manner. To handle practical settings where gathering data requires use of finite resources, it is desirable to explicitly incorporate function evaluation costs into Bayesian optimization policies. To understand how to do so, we develop a previously-unexplored connection between cost-aware Bayesian optimization and the Pandora's Box problem, a decision problem from economics. The Pandora's Box problem admits a Bayesian-optimal solution based on an expression called the Gittins index, which can be reinterpreted as an acquisition function. We study the use of this acquisition function for cost-aware Bayesian optimization, and demonstrate empirically that it performs well, particularly in medium-high dimensions. We further show that this performance carries over to classical Bayesian optimization without explicit evaluation costs. Our work constitutes a first step towards integrating techniques from Gittins index theory into Bayesian optimization.