Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeAsymmetries in Financial Spillovers

Oct 21, 2024This paper analyzes nonlinearities in the international transmission of financial shocks originating in the US. To do so, we develop a flexible nonlinear multi-country model. Our framework is capable of producing asymmetries in the responses to financial shocks for shock size and sign, and over time. We show that international reactions to US-based financial shocks are asymmetric along these dimensions. Particularly, we find that adverse shocks trigger stronger declines in output, inflation, and stock markets than benign shocks. Further, we investigate time variation in the estimated dynamic effects and characterize the responsiveness of three major central banks to financial shocks.

Nowcasting in a Pandemic using Non-Parametric Mixed Frequency VARs

Sep 08, 2020

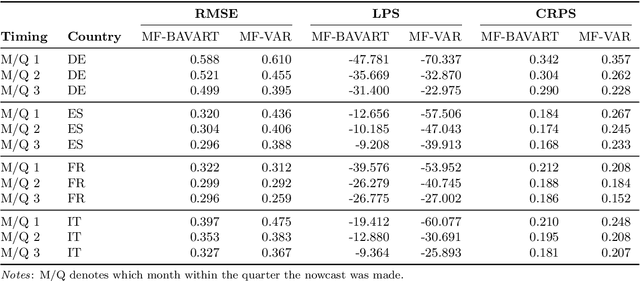

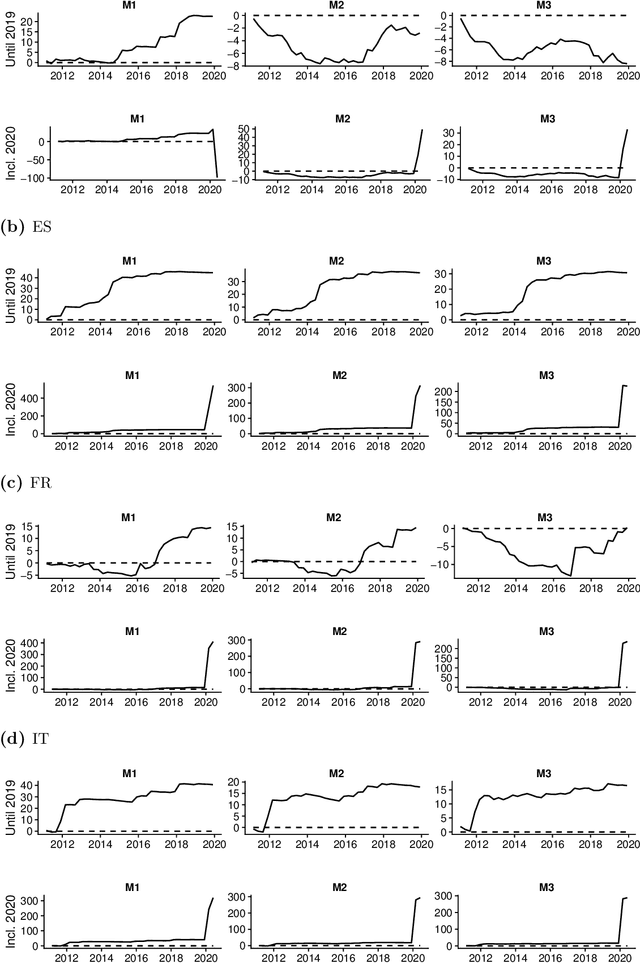

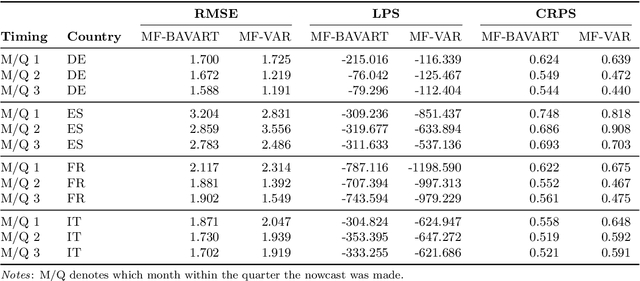

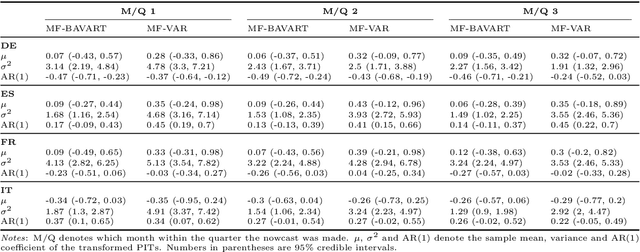

This paper develops Bayesian econometric methods for posterior and predictive inference in a non-parametric mixed frequency VAR using additive regression trees. We argue that regression tree models are ideally suited for macroeconomic nowcasting in the face of the extreme observations produced by the pandemic due to their flexibility and ability to model outliers. In a nowcasting application involving four major countries in the European Union, we find substantial improvements in nowcasting performance relative to a linear mixed frequency VAR. A detailed examination of the predictive densities in the first six months of 2020 shows where these improvements are achieved.