Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeFighting Sampling Bias: A Framework for Training and Evaluating Credit Scoring Models

Jul 17, 2024

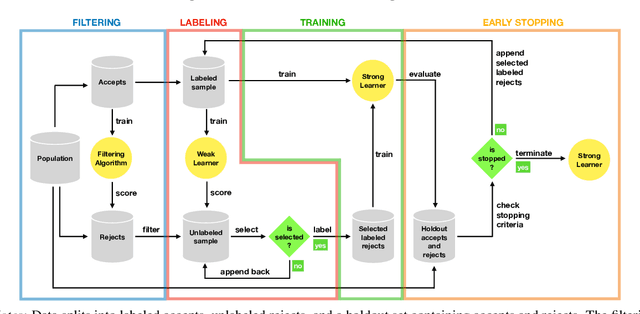

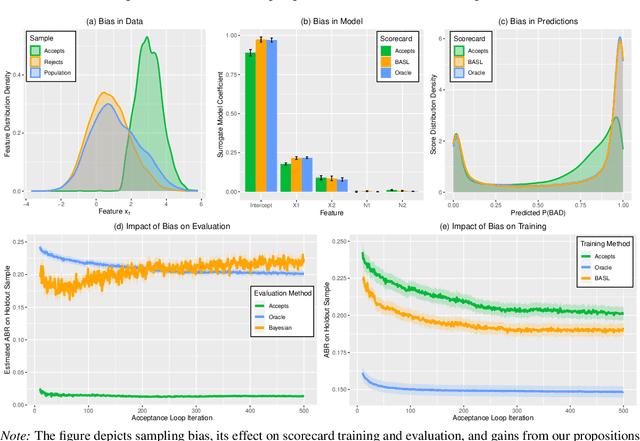

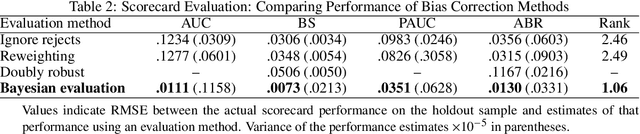

Scoring models support decision-making in financial institutions. Their estimation and evaluation are based on the data of previously accepted applicants with known repayment behavior. This creates sampling bias: the available labeled data offers a partial picture of the distribution of candidate borrowers, which the model is supposed to score. The paper addresses the adverse effect of sampling bias on model training and evaluation. To improve scorecard training, we propose bias-aware self-learning - a reject inference framework that augments the biased training data by inferring labels for selected rejected applications. For scorecard evaluation, we propose a Bayesian framework that extends standard accuracy measures to the biased setting and provides a reliable estimate of future scorecard performance. Extensive experiments on synthetic and real-world data confirm the superiority of our propositions over various benchmarks in predictive performance and profitability. By sensitivity analysis, we also identify boundary conditions affecting their performance. Notably, we leverage real-world data from a randomized controlled trial to assess the novel methodologies on holdout data that represent the true borrower population. Our findings confirm that reject inference is a difficult problem with modest potential to improve scorecard performance. Addressing sampling bias during scorecard evaluation is a much more promising route to improve scoring practices. For example, our results suggest a profit improvement of about eight percent, when using Bayesian evaluation to decide on acceptance rates.

Shallow Self-Learning for Reject Inference in Credit Scoring

Sep 13, 2019

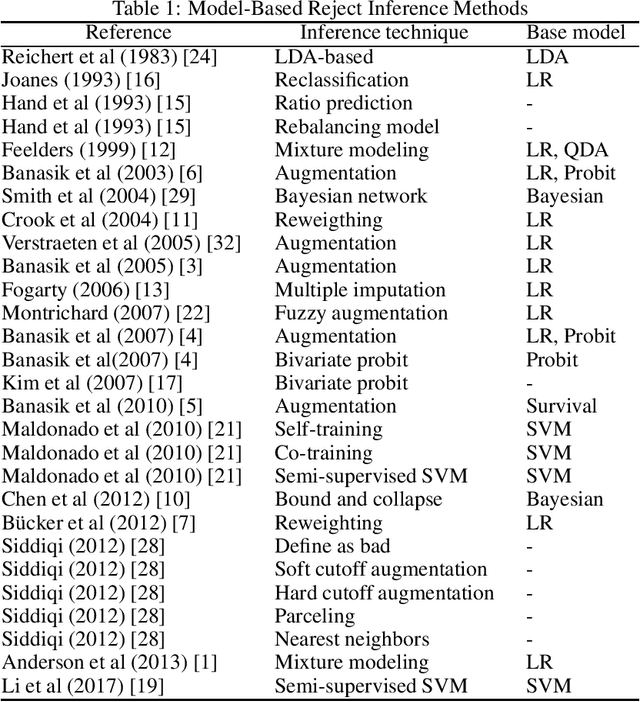

Credit scoring models support loan approval decisions in the financial services industry. Lenders train these models on data from previously granted credit applications, where the borrowers' repayment behavior has been observed. This approach creates sample bias. The scoring model (i.e., classifier) is trained on accepted cases only. Applying the resulting model to screen credit applications from the population of all borrowers degrades model performance. Reject inference comprises techniques to overcome sampling bias through assigning labels to rejected cases. The paper makes two contributions. First, we propose a self-learning framework for reject inference. The framework is geared toward real-world credit scoring requirements through considering distinct training regimes for iterative labeling and model training. Second, we introduce a new measure to assess the effectiveness of reject inference strategies. Our measure leverages domain knowledge to avoid artificial labeling of rejected cases during strategy evaluation. We demonstrate this approach to offer a robust and operational assessment of reject inference strategies. Experiments on a real-world credit scoring data set confirm the superiority of the adjusted self-learning framework over regular self-learning and previous reject inference strategies. We also find strong evidence in favor of the proposed evaluation measure assessing reject inference strategies more reliably, raising the performance of the eventual credit scoring model.