Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeFinRL-Meta: A Universe of Near-Real Market Environments for Data-Driven Deep Reinforcement Learning in Quantitative Finance

Dec 13, 2021

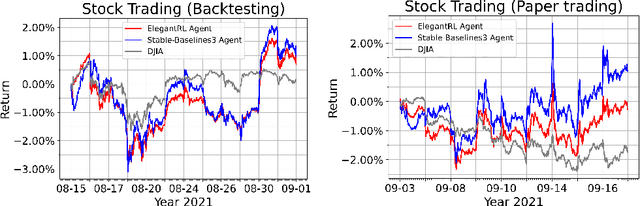

Deep reinforcement learning (DRL) has shown huge potentials in building financial market simulators recently. However, due to the highly complex and dynamic nature of real-world markets, raw historical financial data often involve large noise and may not reflect the future of markets, degrading the fidelity of DRL-based market simulators. Moreover, the accuracy of DRL-based market simulators heavily relies on numerous and diverse DRL agents, which increases demand for a universe of market environments and imposes a challenge on simulation speed. In this paper, we present a FinRL-Meta framework that builds a universe of market environments for data-driven financial reinforcement learning. First, FinRL-Meta separates financial data processing from the design pipeline of DRL-based strategy and provides open-source data engineering tools for financial big data. Second, FinRL-Meta provides hundreds of market environments for various trading tasks. Third, FinRL-Meta enables multiprocessing simulation and training by exploiting thousands of GPU cores. Our codes are available online at https://github.com/AI4Finance-Foundation/FinRL-Meta.