Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeUBER-GNN: A User-Based Embeddings Recommendation based on Graph Neural Networks

Paper and Code

Aug 06, 2020

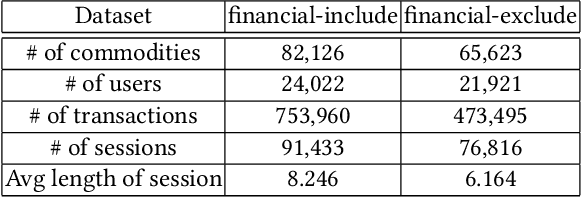

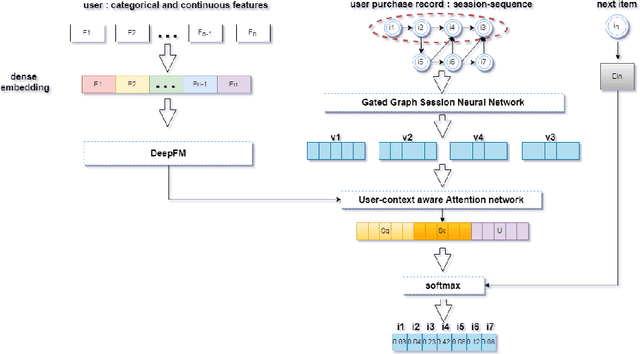

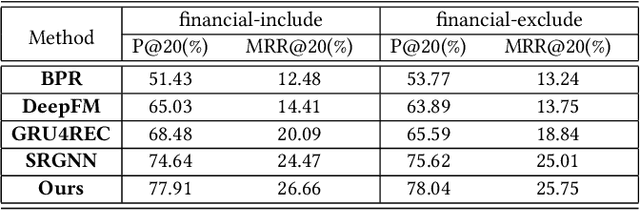

The problem of session-based recommendation aims to predict user next actions based on session histories. Previous methods models session histories into sequences and estimate user latent features by RNN and GNN methods to make recommendations. However under massive-scale and complicated financial recommendation scenarios with both virtual and real commodities , such methods are not sufficient to represent accurate user latent features and neglect the long-term characteristics of users. To take long-term preference and dynamic interests into account, we propose a novel method, i.e. User-Based Embeddings Recommendation with Graph Neural Network, UBER-GNN for brevity. UBER-GNN takes advantage of structured data to generate longterm user preferences, and transfers session sequences into graphs to generate graph-based dynamic interests. The final user latent feature is then represented as the composition of the long-term preferences and the dynamic interests using attention mechanism. Extensive experiments conducted on real Ping An scenario show that UBER-GNN outperforms the state-of-the-art session-based recommendation methods.