Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeThe Value of Big Data for Credit Scoring: Enhancing Financial Inclusion using Mobile Phone Data and Social Network Analytics

Paper and Code

Feb 23, 2020

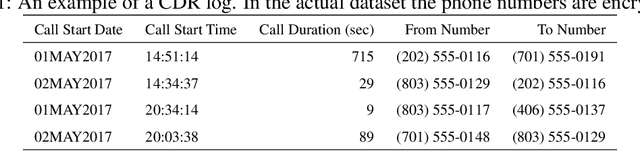

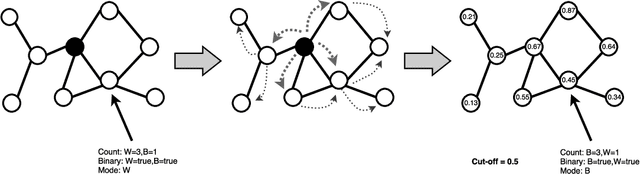

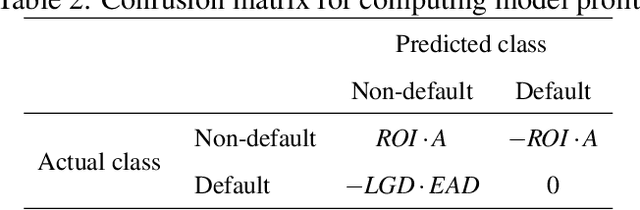

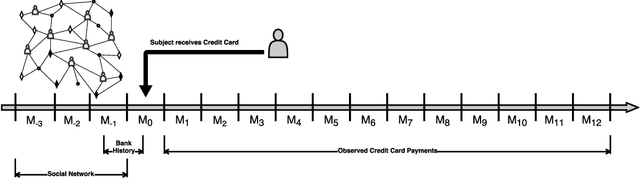

Credit scoring is without a doubt one of the oldest applications of analytics. In recent years, a multitude of sophisticated classification techniques have been developed to improve the statistical performance of credit scoring models. Instead of focusing on the techniques themselves, this paper leverages alternative data sources to enhance both statistical and economic model performance. The study demonstrates how including call networks, in the context of positive credit information, as a new Big Data source has added value in terms of profit by applying a profit measure and profit-based feature selection. A unique combination of datasets, including call-detail records, credit and debit account information of customers is used to create scorecards for credit card applicants. Call-detail records are used to build call networks and advanced social network analytics techniques are applied to propagate influence from prior defaulters throughout the network to produce influence scores. The results show that combining call-detail records with traditional data in credit scoring models significantly increases their performance when measured in AUC. In terms of profit, the best model is the one built with only calling behavior features. In addition, the calling behavior features are the most predictive in other models, both in terms of statistical and economic performance. The results have an impact in terms of ethical use of call-detail records, regulatory implications, financial inclusion, as well as data sharing and privacy.