Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLearning Quantile Functions without Quantile Crossing for Distribution-free Time Series Forecasting

Paper and Code

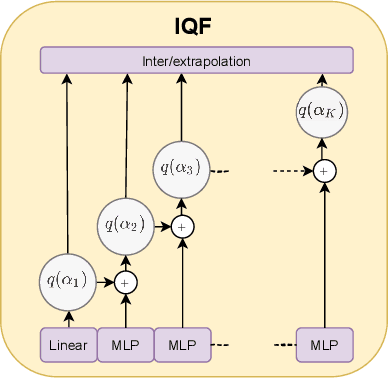

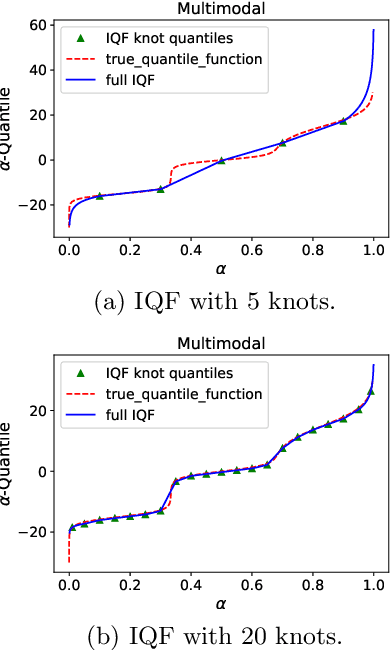

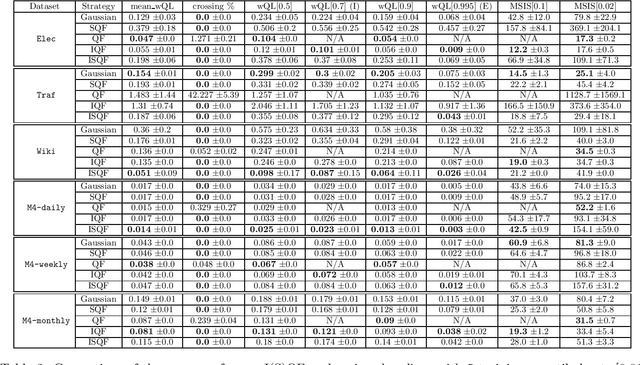

Quantile regression is an effective technique to quantify uncertainty, fit challenging underlying distributions, and often provide full probabilistic predictions through joint learnings over multiple quantile levels. A common drawback of these joint quantile regressions, however, is \textit{quantile crossing}, which violates the desirable monotone property of the conditional quantile function. In this work, we propose the Incremental (Spline) Quantile Functions I(S)QF, a flexible and efficient distribution-free quantile estimation framework that resolves quantile crossing with a simple neural network layer. Moreover, I(S)QF inter/extrapolate to predict arbitrary quantile levels that differ from the underlying training ones. Equipped with the analytical evaluation of the continuous ranked probability score of I(S)QF representations, we apply our methods to NN-based times series forecasting cases, where the savings of the expensive re-training costs for non-trained quantile levels is particularly significant. We also provide a generalization error analysis of our proposed approaches under the sequence-to-sequence setting. Lastly, extensive experiments demonstrate the improvement of consistency and accuracy errors over other baselines.