Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeHATS: A Hierarchical Graph Attention Network for Stock Movement Prediction

Paper and Code

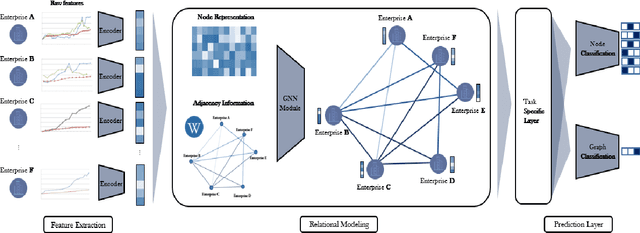

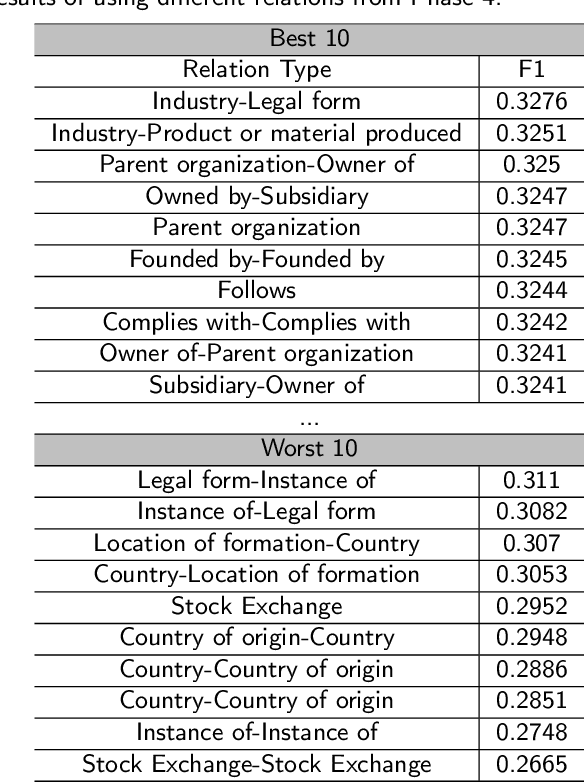

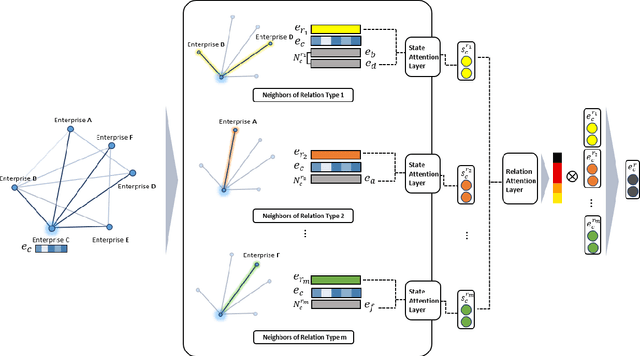

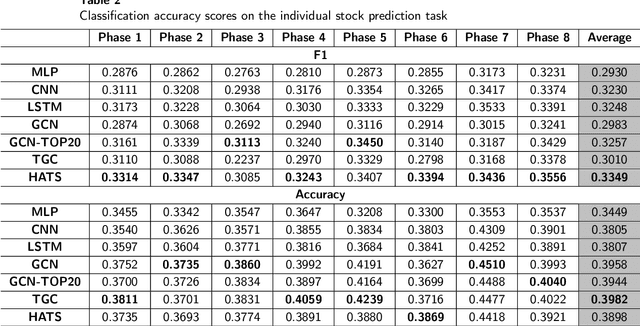

Many researchers both in academia and industry have long been interested in the stock market. Numerous approaches were developed to accurately predict future trends in stock prices. Recently, there has been a growing interest in utilizing graph-structured data in computer science research communities. Methods that use relational data for stock market prediction have been recently proposed, but they are still in their infancy. First, the quality of collected information from different types of relations can vary considerably. No existing work has focused on the effect of using different types of relations on stock market prediction or finding an effective way to selectively aggregate information on different relation types. Furthermore, existing works have focused on only individual stock prediction which is similar to the node classification task. To address this, we propose a hierarchical attention network for stock prediction (HATS) which uses relational data for stock market prediction. Our HATS method selectively aggregates information on different relation types and adds the information to the representations of each company. Specifically, node representations are initialized with features extracted from a feature extraction module. HATS is used as a relational modeling module with initialized node representations. Then, node representations with the added information are fed into a task-specific layer. Our method is used for predicting not only individual stock prices but also market index movements, which is similar to the graph classification task. The experimental results show that performance can change depending on the relational data used. HATS which can automatically select information outperformed all the existing methods.