Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeGraph Dimension Attention Networks for Enterprise Credit Assessment

Paper and Code

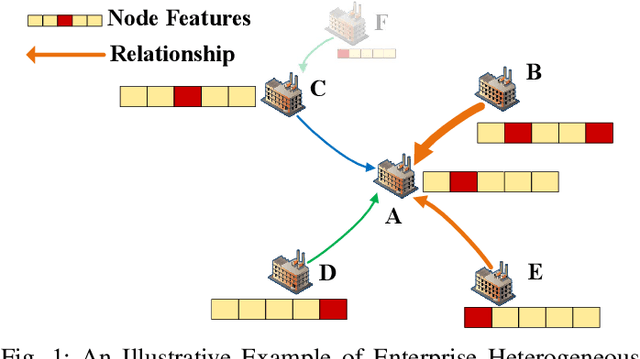

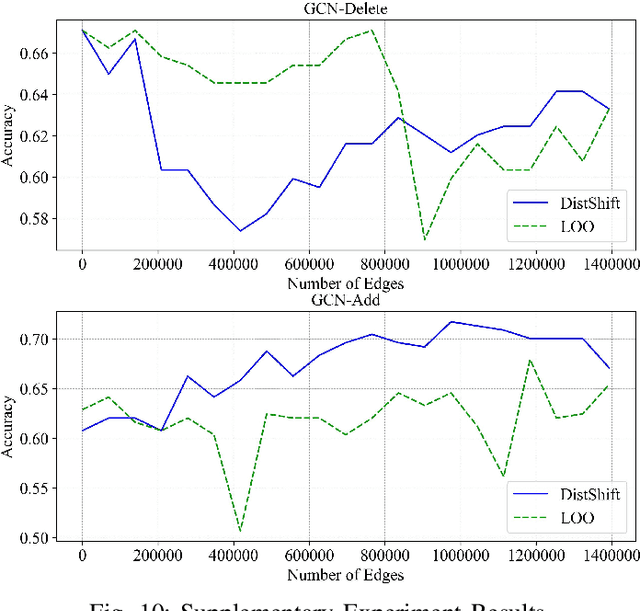

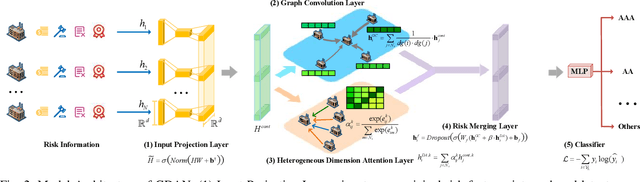

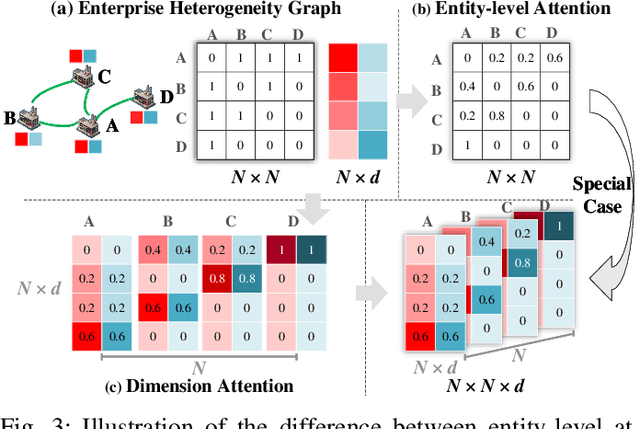

Enterprise credit assessment is critical for evaluating financial risk, and Graph Neural Networks (GNNs), with their advanced capability to model inter-entity relationships, are a natural tool to get a deeper understanding of these financial networks. However, existing GNN-based methodologies predominantly emphasize entity-level attention mechanisms for contagion risk aggregation, often overlooking the heterogeneous importance of different feature dimensions, thus falling short in adequately modeling credit risk levels. To address this issue, we propose a novel architecture named Graph Dimension Attention Network (GDAN), which incorporates a dimension-level attention mechanism to capture fine-grained risk-related characteristics. Furthermore, we explore the interpretability of the GNN-based method in financial scenarios and propose a simple but effective data-centric explainer for GDAN, called GDAN-DistShift. DistShift provides edge-level interpretability by quantifying distribution shifts during the message-passing process. Moreover, we collected a real-world, multi-source Enterprise Credit Assessment Dataset (ECAD) and have made it accessible to the research community since high-quality datasets are lacking in this field. Extensive experiments conducted on ECAD demonstrate the effectiveness of our methods. In addition, we ran GDAN on the well-known datasets SMEsD and DBLP, also with excellent results.