Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeCLVSA: A Convolutional LSTM Based Variational Sequence-to-Sequence Model with Attention for Predicting Trends of Financial Markets

Paper and Code

Apr 08, 2021

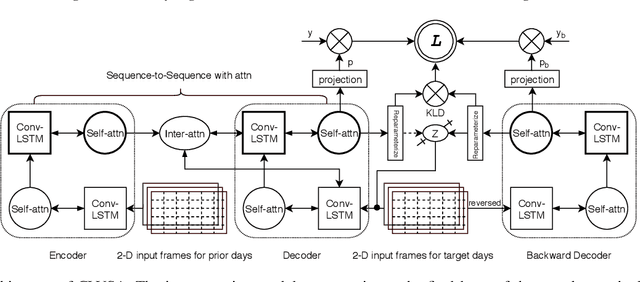

Financial markets are a complex dynamical system. The complexity comes from the interaction between a market and its participants, in other words, the integrated outcome of activities of the entire participants determines the markets trend, while the markets trend affects activities of participants. These interwoven interactions make financial markets keep evolving. Inspired by stochastic recurrent models that successfully capture variability observed in natural sequential data such as speech and video, we propose CLVSA, a hybrid model that consists of stochastic recurrent networks, the sequence-to-sequence architecture, the self- and inter-attention mechanism, and convolutional LSTM units to capture variationally underlying features in raw financial trading data. Our model outperforms basic models, such as convolutional neural network, vanilla LSTM network, and sequence-to-sequence model with attention, based on backtesting results of six futures from January 2010 to December 2017. Our experimental results show that, by introducing an approximate posterior, CLVSA takes advantage of an extra regularizer based on the Kullback-Leibler divergence to prevent itself from overfitting traps.