Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeASAT: Adaptively Scaled Adversarial Training in Time Series

Paper and Code

Aug 20, 2021

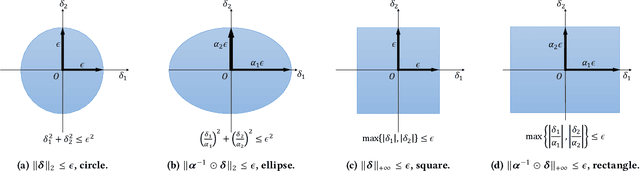

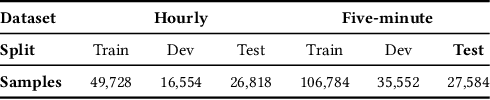

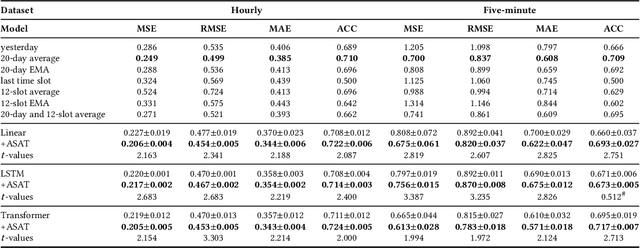

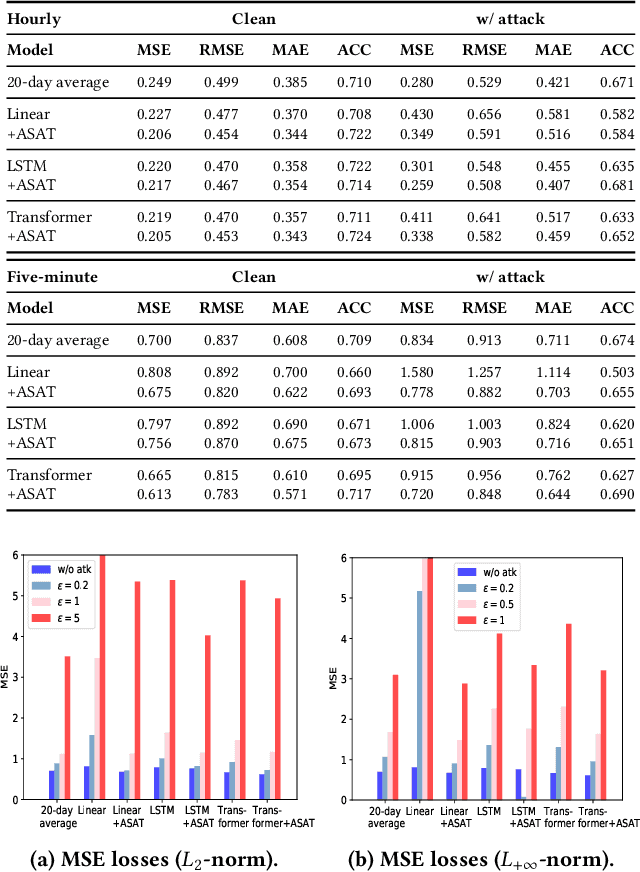

Adversarial training is a method for enhancing neural networks to improve the robustness against adversarial examples. Besides the security concerns of potential adversarial examples, adversarial training can also improve the performance of the neural networks, train robust neural networks, and provide interpretability for neural networks. In this work, we take the first step to introduce adversarial training in time series analysis by taking the finance field as an example. Rethinking existing researches of adversarial training, we propose the adaptively scaled adversarial training (ASAT) in time series analysis, by treating data at different time slots with time-dependent importance weights. Experimental results show that the proposed ASAT can improve both the accuracy and the adversarial robustness of neural networks. Besides enhancing neural networks, we also propose the dimension-wise adversarial sensitivity indicator to probe the sensitivities and importance of input dimensions. With the proposed indicator, we can explain the decision bases of black box neural networks.