Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeBreaking the Gradient Barrier: Unveiling Large Language Models for Strategic Classification

Nov 10, 2025Strategic classification~(SC) explores how individuals or entities modify their features strategically to achieve favorable classification outcomes. However, existing SC methods, which are largely based on linear models or shallow neural networks, face significant limitations in terms of scalability and capacity when applied to real-world datasets with significantly increasing scale, especially in financial services and the internet sector. In this paper, we investigate how to leverage large language models to design a more scalable and efficient SC framework, especially in the case of growing individuals engaged with decision-making processes. Specifically, we introduce GLIM, a gradient-free SC method grounded in in-context learning. During the feed-forward process of self-attention, GLIM implicitly simulates the typical bi-level optimization process of SC, including both the feature manipulation and decision rule optimization. Without fine-tuning the LLMs, our proposed GLIM enjoys the advantage of cost-effective adaptation in dynamic strategic environments. Theoretically, we prove GLIM can support pre-trained LLMs to adapt to a broad range of strategic manipulations. We validate our approach through experiments with a collection of pre-trained LLMs on real-world and synthetic datasets in financial and internet domains, demonstrating that our GLIM exhibits both robustness and efficiency, and offering an effective solution for large-scale SC tasks.

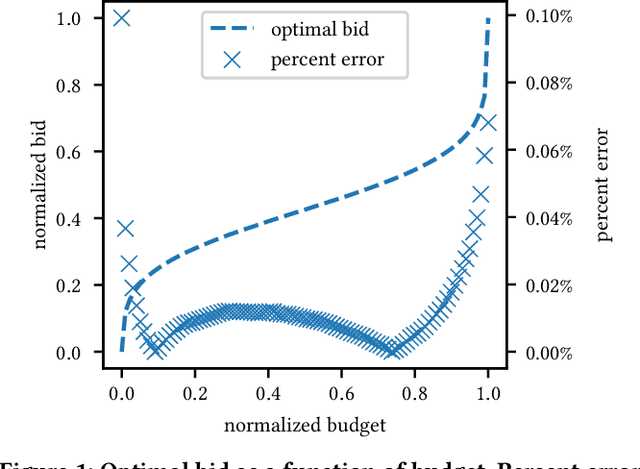

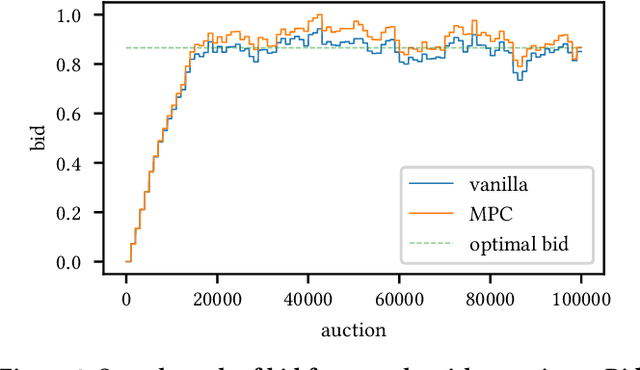

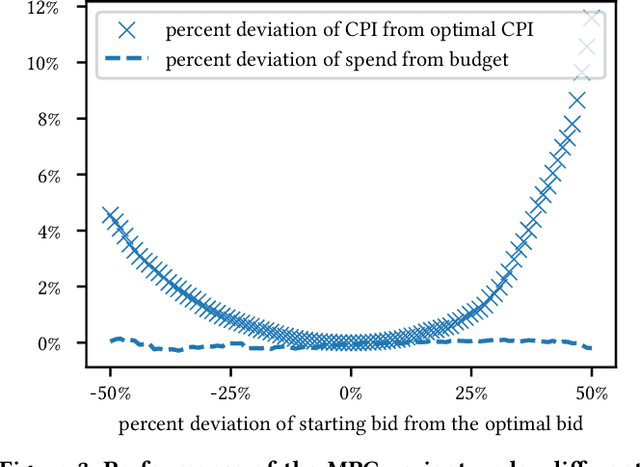

Bidding Agent Design in the LinkedIn Ad Marketplace

Feb 25, 2022

We establish a general optimization framework for the design of automated bidding agent in dynamic online marketplaces. It optimizes solely for the buyer's interest and is agnostic to the auction mechanism imposed by the seller. As a result, the framework allows, for instance, the joint optimization of a group of ads across multiple platforms each running its own auction format. Bidding strategy derived from this framework automatically guarantees the optimality of budget allocation across ad units and platforms. Common constraints such as budget delivery schedule, return on investments and guaranteed results, directly translates to additional parameters in the bidding formula. We share practical learnings of the deployed bidding system in the LinkedIn ad marketplace based on this framework.

On the convergence of optimistic policy iteration for stochastic shortest path problem

Aug 30, 2018In this paper, we prove some convergence results of a special case of optimistic policy iteration algorithm for stochastic shortest path problem. We consider both Monte Carlo and $TD(\lambda)$ methods for the policy evaluation step under the condition that the termination state will eventually be reached almost surely.