Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLearning the Efficient Frontier

Oct 13, 2023

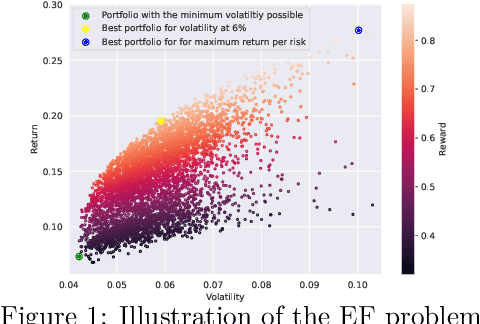

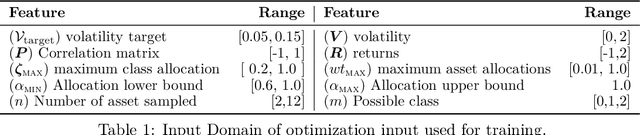

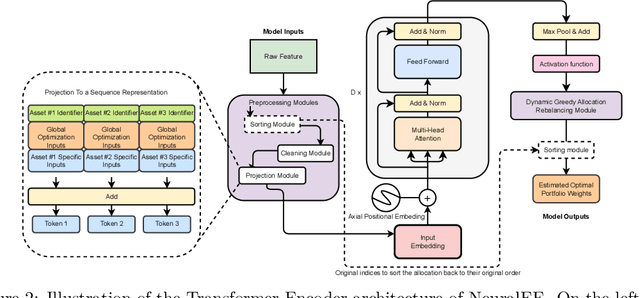

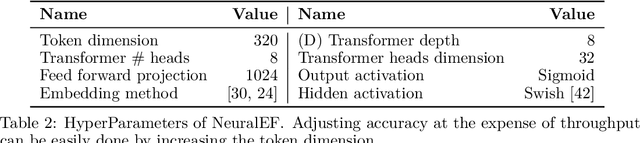

The efficient frontier (EF) is a fundamental resource allocation problem where one has to find an optimal portfolio maximizing a reward at a given level of risk. This optimal solution is traditionally found by solving a convex optimization problem. In this paper, we introduce NeuralEF: a fast neural approximation framework that robustly forecasts the result of the EF convex optimization problem with respect to heterogeneous linear constraints and variable number of optimization inputs. By reformulating an optimization problem as a sequence to sequence problem, we show that NeuralEF is a viable solution to accelerate large-scale simulation while handling discontinuous behavior.

Robust and Active Learning for Deep Neural Network Regression

Jul 28, 2021

We describe a gradient-based method to discover local error maximizers of a deep neural network (DNN) used for regression, assuming the availability of an "oracle" capable of providing real-valued supervision (a regression target) for samples. For example, the oracle could be a numerical solver which, operationally, is much slower than the DNN. Given a discovered set of local error maximizers, the DNN is either fine-tuned or retrained in the manner of active learning.

Deeply Learning Derivatives

Oct 17, 2018

This paper uses deep learning to value derivatives. The approach is broadly applicable, and we use a call option on a basket of stocks as an example. We show that the deep learning model is accurate and very fast, capable of producing valuations a million times faster than traditional models. We develop a methodology to randomly generate appropriate training data and explore the impact of several parameters including layer width and depth, training data quality and quantity on model speed and accuracy.