Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeTackling Decision Processes with Non-Cumulative Objectives using Reinforcement Learning

May 22, 2024

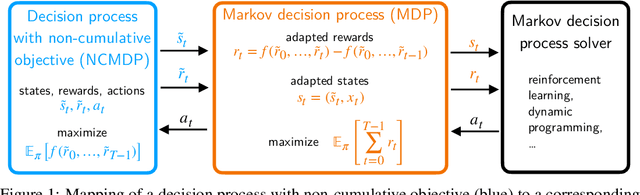

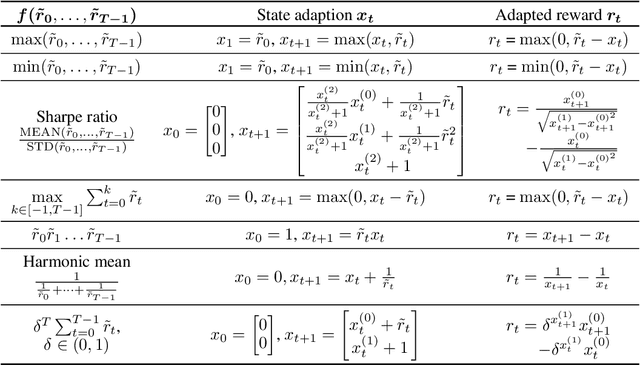

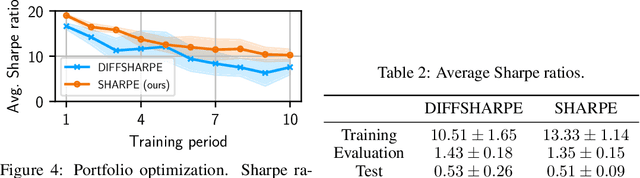

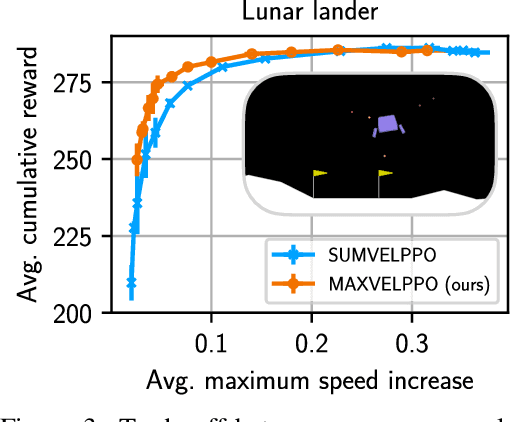

Markov decision processes (MDPs) are used to model a wide variety of applications ranging from game playing over robotics to finance. Their optimal policy typically maximizes the expected sum of rewards given at each step of the decision process. However, a large class of problems does not fit straightforwardly into this framework: Non-cumulative Markov decision processes (NCMDPs), where instead of the expected sum of rewards, the expected value of an arbitrary function of the rewards is maximized. Example functions include the maximum of the rewards or their mean divided by their standard deviation. In this work, we introduce a general mapping of NCMDPs to standard MDPs. This allows all techniques developed to find optimal policies for MDPs, such as reinforcement learning or dynamic programming, to be directly applied to the larger class of NCMDPs. Focusing on reinforcement learning, we show applications in a diverse set of tasks, including classical control, portfolio optimization in finance, and discrete optimization problems. Given our approach, we can improve both final performance and training time compared to relying on standard MDPs.

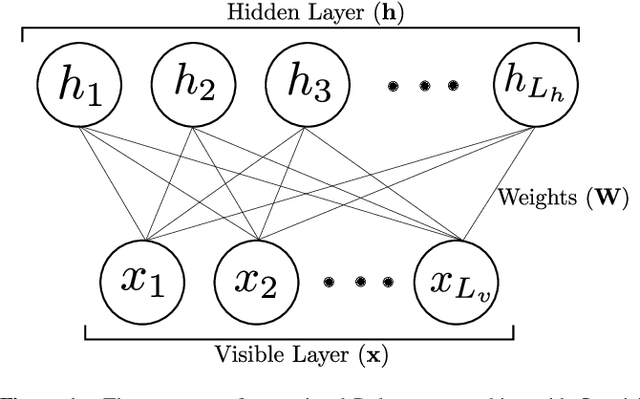

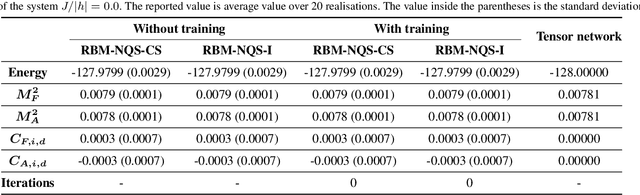

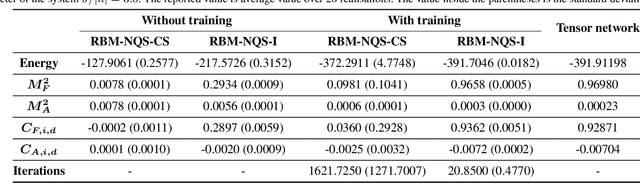

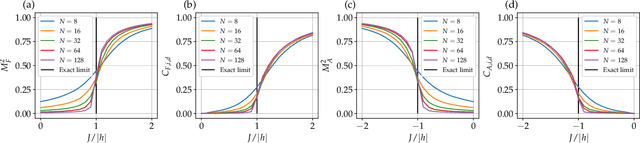

Finding Quantum Critical Points with Neural-Network Quantum States

Feb 07, 2020

Finding the precise location of quantum critical points is of particular importance to characterise quantum many-body systems at zero temperature. However, quantum many-body systems are notoriously hard to study because the dimension of their Hilbert space increases exponentially with their size. Recently, machine learning tools known as neural-network quantum states have been shown to effectively and efficiently simulate quantum many-body systems. We present an approach to finding the quantum critical points of the quantum Ising model using neural-network quantum states, analytically constructed innate restricted Boltzmann machines, transfer learning and unsupervised learning. We validate the approach and evaluate its efficiency and effectiveness in comparison with other traditional approaches.