Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeThe Pseudo-Dimension of Contracts

Jan 24, 2025

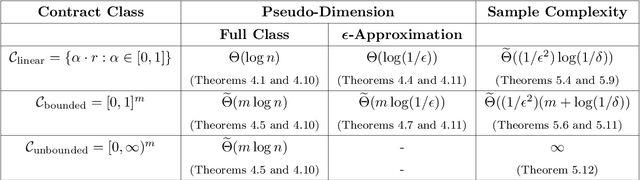

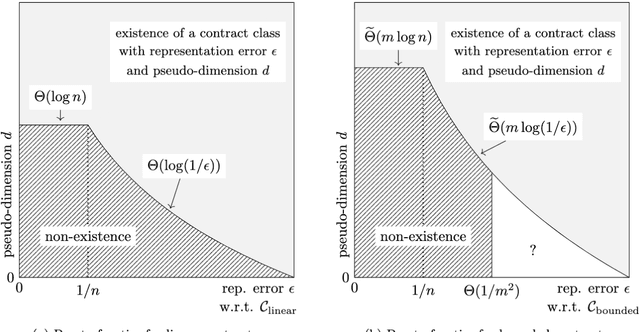

Algorithmic contract design studies scenarios where a principal incentivizes an agent to exert effort on her behalf. In this work, we focus on settings where the agent's type is drawn from an unknown distribution, and formalize an offline learning framework for learning near-optimal contracts from sample agent types. A central tool in our analysis is the notion of pseudo-dimension from statistical learning theory. Beyond its role in establishing upper bounds on the sample complexity, pseudo-dimension measures the intrinsic complexity of a class of contracts, offering a new perspective on the tradeoffs between simplicity and optimality in contract design. Our main results provide essentially optimal tradeoffs between pseudo-dimension and representation error (defined as the loss in principal's utility) with respect to linear and bounded contracts. Using these tradeoffs, we derive sample- and time-efficient learning algorithms, and demonstrate their near-optimality by providing almost matching lower bounds on the sample complexity. Conversely, for unbounded contracts, we prove an impossibility result showing that no learning algorithm exists. Finally, we extend our techniques in three important ways. First, we provide refined pseudo-dimension and sample complexity guarantees for the combinatorial actions model, revealing a novel connection between the number of critical values and sample complexity. Second, we extend our results to menus of contracts, showing that their pseudo-dimension scales linearly with the menu size. Third, we adapt our algorithms to the online learning setting, where we show that, a polynomial number of type samples suffice to learn near-optimal bounded contracts. Combined with prior work, this establishes a formal separation between expert advice and bandit feedback for this setting.

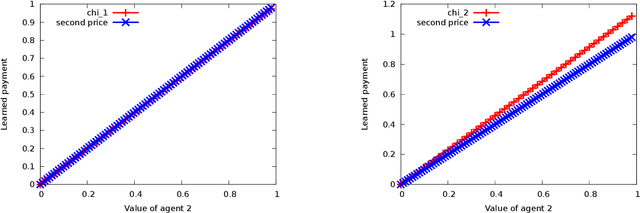

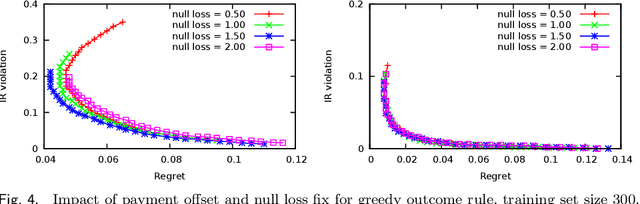

Payment Rules through Discriminant-Based Classifiers

Aug 06, 2012

In mechanism design it is typical to impose incentive compatibility and then derive an optimal mechanism subject to this constraint. By replacing the incentive compatibility requirement with the goal of minimizing expected ex post regret, we are able to adapt statistical machine learning techniques to the design of payment rules. This computational approach to mechanism design is applicable to domains with multi-dimensional types and situations where computational efficiency is a concern. Specifically, given an outcome rule and access to a type distribution, we train a support vector machine with a special discriminant function structure such that it implicitly establishes a payment rule with desirable incentive properties. We discuss applications to a multi-minded combinatorial auction with a greedy winner-determination algorithm and to an assignment problem with egalitarian outcome rule. Experimental results demonstrate both that the construction produces payment rules with low ex post regret, and that penalizing classification errors is effective in preventing failures of ex post individual rationality.