Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeSBBTS: A Unified Schrödinger-Bass Framework for Synthetic Financial Time Series

Apr 08, 2026We study the problem of generating synthetic time series that reproduce both marginal distributions and temporal dynamics, a central challenge in financial machine learning. Existing approaches typically fail to jointly model drift and stochastic volatility, as diffusion-based methods fix the volatility while martingale transport models ignore drift. We introduce the Schrödinger-Bass Bridge for Time Series (SBBTS), a unified framework that extends the Schrödinger-Bass formulation to multi-step time series. The method constructs a diffusion process that jointly calibrates drift and volatility and admits a tractable decomposition into conditional transport problems, enabling efficient learning. Numerical experiments on the Heston model demonstrate that SBBTS accurately recovers stochastic volatility and correlation parameters that prior SchrödingerBridge methods fail to capture. Applied to S&P 500 data, SBBTS-generated synthetic time series consistently improve downstream forecasting performance when used for data augmentation, yielding higher classification accuracy and Sharpe ratio compared to real-data-only training. These results show that SBBTS provides a practical and effective framework for realistic time series generation and data augmentation in financial applications.

LightSBB-M: Bridging Schrödinger and Bass for Generative Diffusion Modeling

Jan 27, 2026The Schrodinger Bridge and Bass (SBB) formulation, which jointly controls drift and volatility, is an established extension of the classical Schrodinger Bridge (SB). Building on this framework, we introduce LightSBB-M, an algorithm that computes the optimal SBB transport plan in only a few iterations. The method exploits a dual representation of the SBB objective to obtain analytic expressions for the optimal drift and volatility, and it incorporates a tunable parameter beta greater than zero that interpolates between pure drift (the Schrodinger Bridge) and pure volatility (Bass martingale transport). We show that LightSBB-M achieves the lowest 2-Wasserstein distance on synthetic datasets against state-of-the-art SB and diffusion baselines with up to 32 percent improvement. We also illustrate the generative capability of the framework on an unpaired image-to-image translation task (adult to child faces in FFHQ). These findings demonstrate that LightSBB-M provides a scalable, high-fidelity SBB solver that outperforms existing SB and diffusion baselines across both synthetic and real-world generative tasks. The code is available at https://github.com/alexouadi/LightSBB-M.

Regret Analysis of Learning-Based Linear Quadratic Gaussian Control with Additive Exploration

Nov 05, 2023In this paper, we analyze the regret incurred by a computationally efficient exploration strategy, known as naive exploration, for controlling unknown partially observable systems within the Linear Quadratic Gaussian (LQG) framework. We introduce a two-phase control algorithm called LQG-NAIVE, which involves an initial phase of injecting Gaussian input signals to obtain a system model, followed by a second phase of an interplay between naive exploration and control in an episodic fashion. We show that LQG-NAIVE achieves a regret growth rate of $\tilde{\mathcal{O}}(\sqrt{T})$, i.e., $\mathcal{O}(\sqrt{T})$ up to logarithmic factors after $T$ time steps, and we validate its performance through numerical simulations. Additionally, we propose LQG-IF2E, which extends the exploration signal to a `closed-loop' setting by incorporating the Fisher Information Matrix (FIM). We provide compelling numerical evidence of the competitive performance of LQG-IF2E compared to LQG-NAIVE.

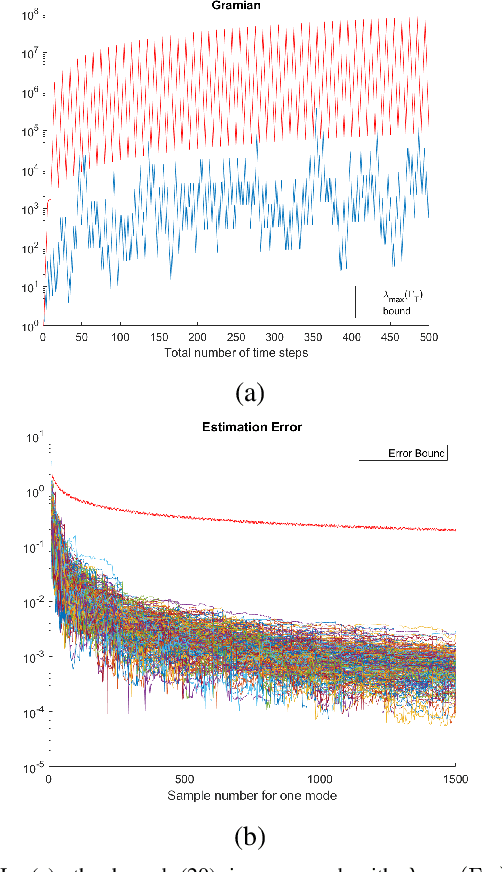

Finite-sample analysis of identification of switched linear systems with arbitrary or restricted switching

Mar 18, 2022

This work aims to derive a data-independent finite-sample error bound for the least-squares (LS) estimation error of switched linear systems when the state and the switching signal are measured. While the existing finite-sample bounds for linear system identification extend to the problem under consideration, the Gramian of the switched system, an essential term in the error bound, depends on the measured switching signal. Therefore, data-independent bounds on the spectrum of the Gramian are developed for globally asymptotically and marginally stable switched systems when the switching is arbitrary or subject to an average dwell time constraint. Combining the bounds on the spectrum of the Gramian and the preliminary error bound extended from linear system identification leads to the error bound for the LS estimate of the switched system.

Efficient learning of hidden state LTI state space models of unknown order

Feb 03, 2022The aim of this paper is to address two related estimation problems arising in the setup of hidden state linear time invariant (LTI) state space systems when the dimension of the hidden state is unknown. Namely, the estimation of any finite number of the system's Markov parameters and the estimation of a minimal realization for the system, both from the partial observation of a single trajectory. For both problems, we provide statistical guarantees in the form of various estimation error upper bounds, $\rank$ recovery conditions, and sample complexity estimates. Specifically, we first show that the low $\rank$ solution of the Hankel penalized least square estimator satisfies an estimation error in $S_p$-norms for $p \in [1,2]$ that captures the effect of the system order better than the existing operator norm upper bound for the simple least square. We then provide a stability analysis for an estimation procedure based on a variant of the Ho-Kalman algorithm that improves both the dependence on the dimension and the least singular value of the Hankel matrix of the Markov parameters. Finally, we propose an estimation algorithm for the minimal realization that uses both the Hankel penalized least square estimator and the Ho-Kalman based estimation procedure and guarantees with high probability that we recover the correct order of the system and satisfies a new fast rate in the $S_2$-norm with a polynomial reduction in the dependence on the dimension and other parameters of the problem.

Non asymptotic estimation lower bounds for LTI state space models with Cramér-Rao and van Trees

Sep 17, 2021We study the estimation problem for linear time-invariant (LTI) state-space models with Gaussian excitation of an unknown covariance. We provide non asymptotic lower bounds for the expected estimation error and the mean square estimation risk of the least square estimator, and the minimax mean square estimation risk. These bounds are sharp with explicit constants when the matrix of the dynamics has no eigenvalues on the unit circle and are rate-optimal when they do. Our results extend and improve existing lower bounds to lower bounds in expectation of the mean square estimation risk and to systems with a general noise covariance. Instrumental to our derivation are new concentration results for rescaled sample covariances and deviation results for the corresponding multiplication processes of the covariates, a differential geometric construction of a prior on the unit operator ball of small Fisher information, and an extension of the Cram\'er-Rao and van Treesinequalities to matrix-valued estimators.

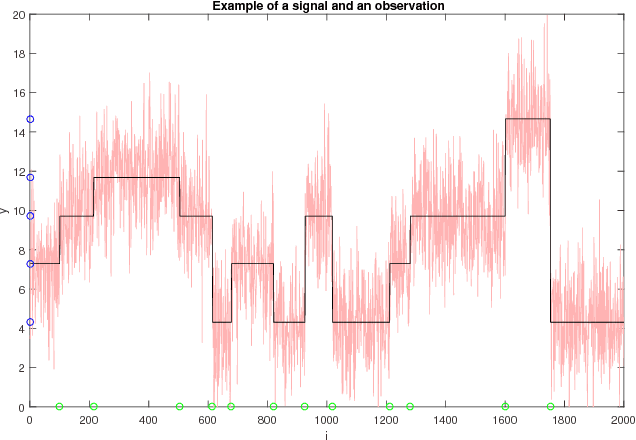

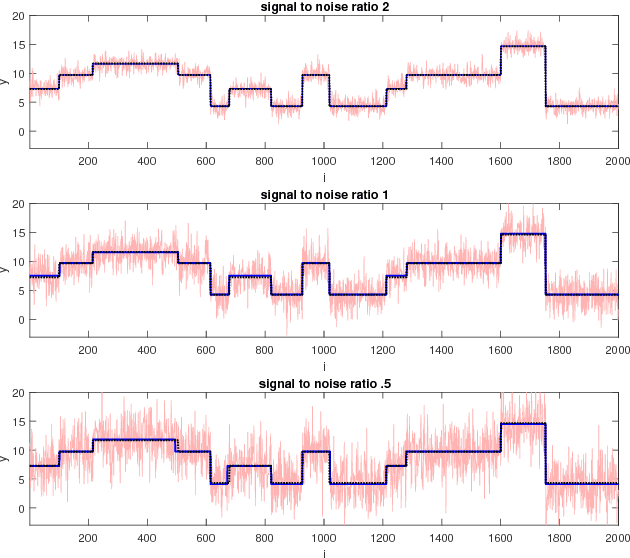

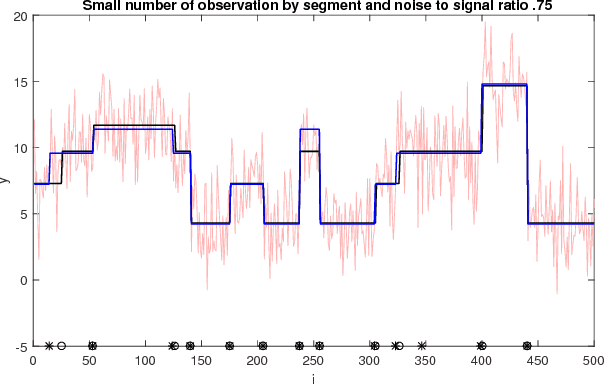

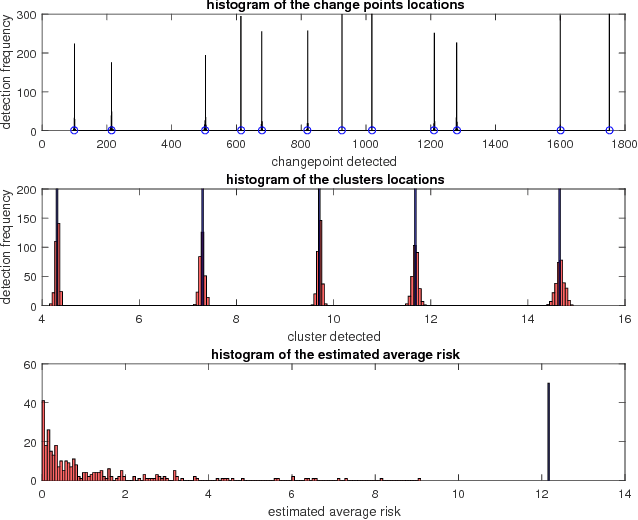

Bayesian Model Selection for Change Point Detection and Clustering

Dec 03, 2019

We address the new problem of estimating a piece-wise constant signal with the purpose of detecting its change points and the levels of clusters. Our approach is to model it as a nonparametric penalized least square model selection on a family of models indexed over the collection of partitions of the design points and propose a computationally efficient algorithm to approximately solve it. Statistically, minimizing such a penalized criterion yields an approximation to the maximum a posteriori probability (MAP) estimator. The criterion is then analyzed and an oracle inequality is derived using a Gaussian concentration inequality. The oracle inequality is used to derive on one hand conditions for consistency and on the other hand an adaptive upper bound on the expected square risk of the estimator, which statistically motivates our approximation. Finally, we apply our algorithm to simulated data to experimentally validate the statistical guarantees and illustrate its behavior.