Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeMultivariate Online Linear Regression for Hierarchical Forecasting

Feb 22, 2024

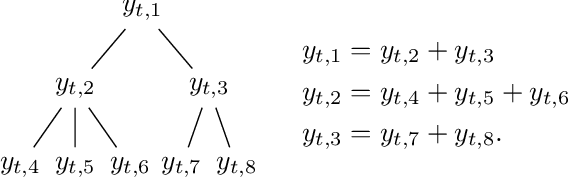

In this paper, we consider a deterministic online linear regression model where we allow the responses to be multivariate. To address this problem, we introduce MultiVAW, a method that extends the well-known Vovk-Azoury-Warmuth algorithm to the multivariate setting, and show that it also enjoys logarithmic regret in time. We apply our results to the online hierarchical forecasting problem and recover an algorithm from this literature as a special case, allowing us to relax the hypotheses usually made for its analysis.

Online Inventory Problems: Beyond the i.i.d. Setting with Online Convex Optimization

Jul 12, 2023

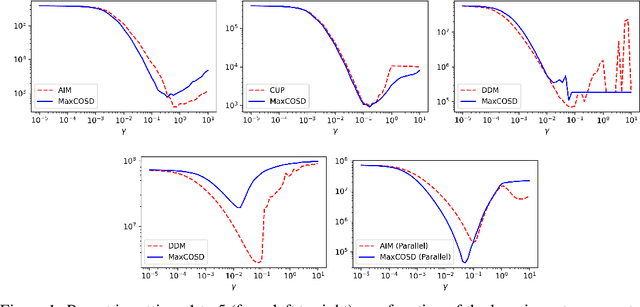

We study multi-product inventory control problems where a manager makes sequential replenishment decisions based on partial historical information in order to minimize its cumulative losses. Our motivation is to consider general demands, losses and dynamics to go beyond standard models which usually rely on newsvendor-type losses, fixed dynamics, and unrealistic i.i.d. demand assumptions. We propose MaxCOSD, an online algorithm that has provable guarantees even for problems with non-i.i.d. demands and stateful dynamics, including for instance perishability. We consider what we call non-degeneracy assumptions on the demand process, and argue that they are necessary to allow learning.