Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeEvolution of AI in Education: Agentic Workflows

Apr 25, 2025

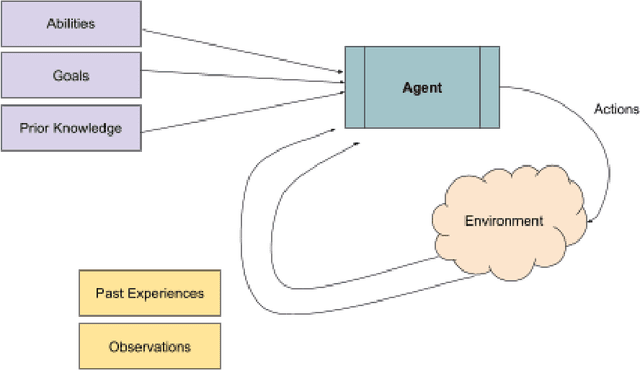

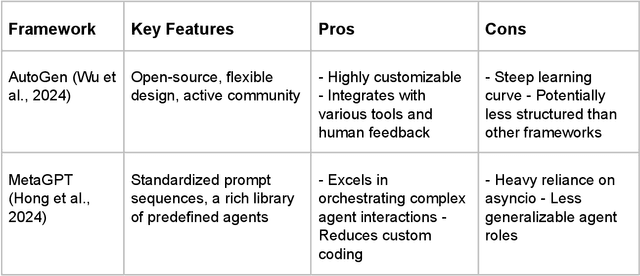

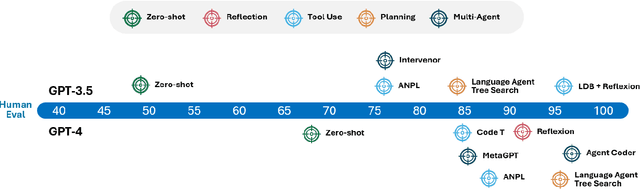

Artificial intelligence (AI) has transformed various aspects of education, with large language models (LLMs) driving advancements in automated tutoring, assessment, and content generation. However, conventional LLMs are constrained by their reliance on static training data, limited adaptability, and lack of reasoning. To address these limitations and foster more sustainable technological practices, AI agents have emerged as a promising new avenue for educational innovation. In this review, we examine agentic workflows in education according to four major paradigms: reflection, planning, tool use, and multi-agent collaboration. We critically analyze the role of AI agents in education through these key design paradigms, exploring their advantages, applications, and challenges. To illustrate the practical potential of agentic systems, we present a proof-of-concept application: a multi-agent framework for automated essay scoring. Preliminary results suggest this agentic approach may offer improved consistency compared to stand-alone LLMs. Our findings highlight the transformative potential of AI agents in educational settings while underscoring the need for further research into their interpretability, trustworthiness, and sustainable impact on pedagogical impact.

Stock price forecast with deep learning

Mar 21, 2021

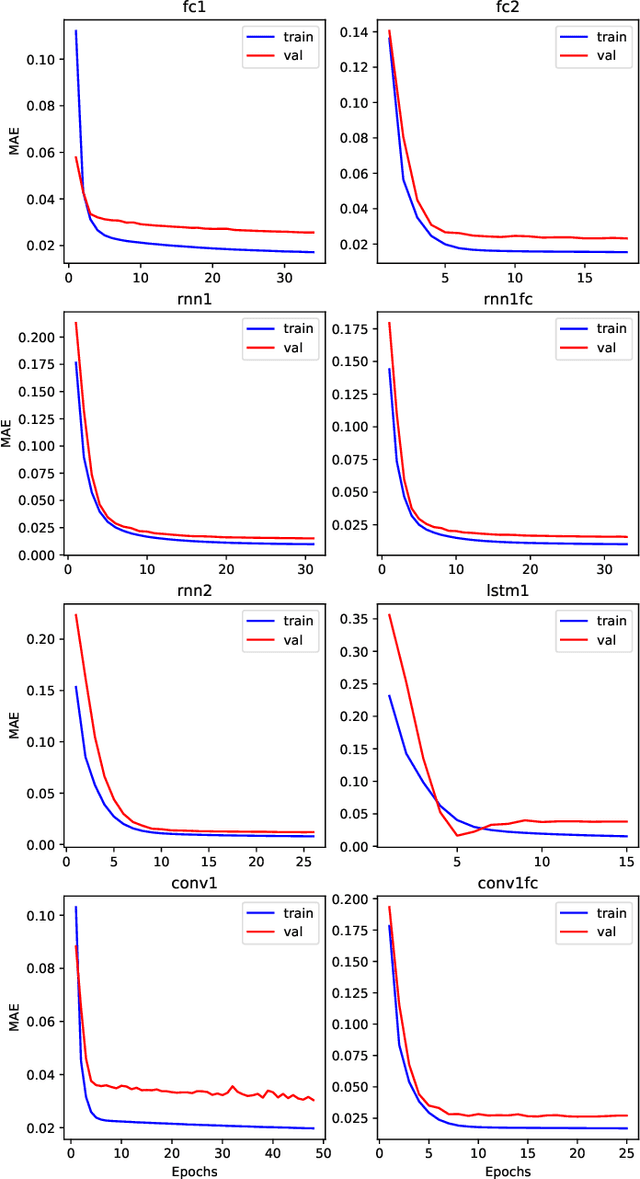

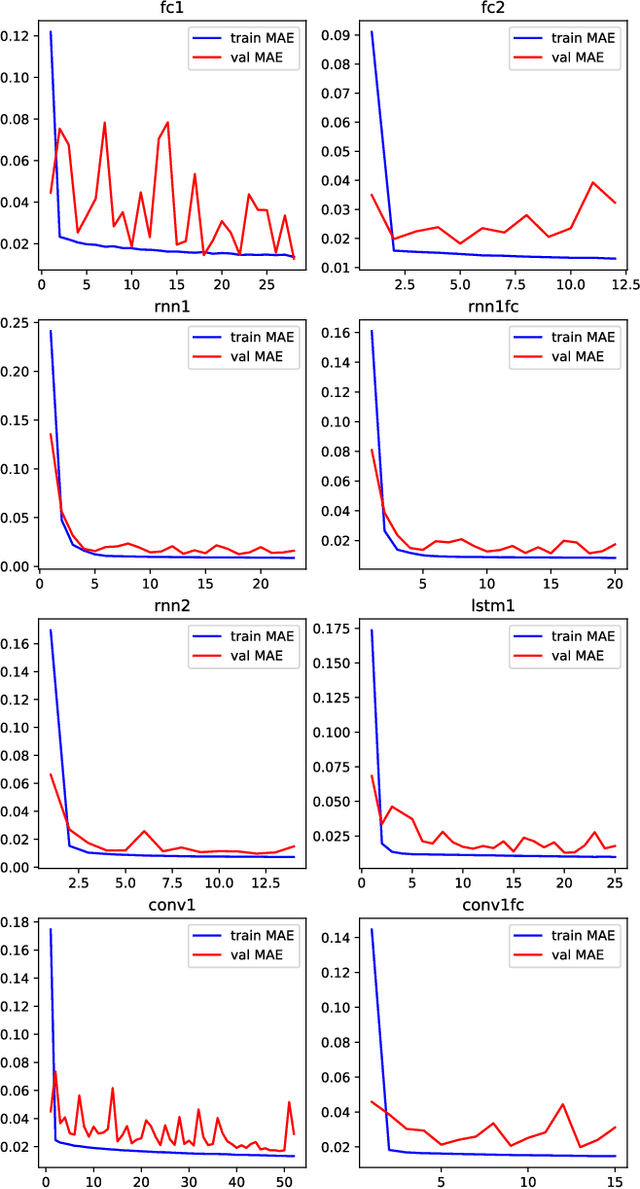

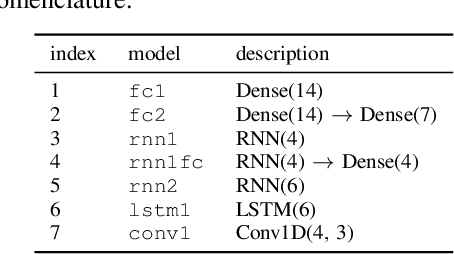

In this paper, we compare various approaches to stock price prediction using neural networks. We analyze the performance fully connected, convolutional, and recurrent architectures in predicting the next day value of S&P 500 index based on its previous values. We further expand our analysis by including three different optimization techniques: Stochastic Gradient Descent, Root Mean Square Propagation, and Adaptive Moment Estimation. The numerical experiments reveal that a single layer recurrent neural network with RMSprop optimizer produces optimal results with validation and test Mean Absolute Error of 0.0150 and 0.0148 respectively.

Forecasting with Deep Learning: S&P 500 index

Mar 21, 2021

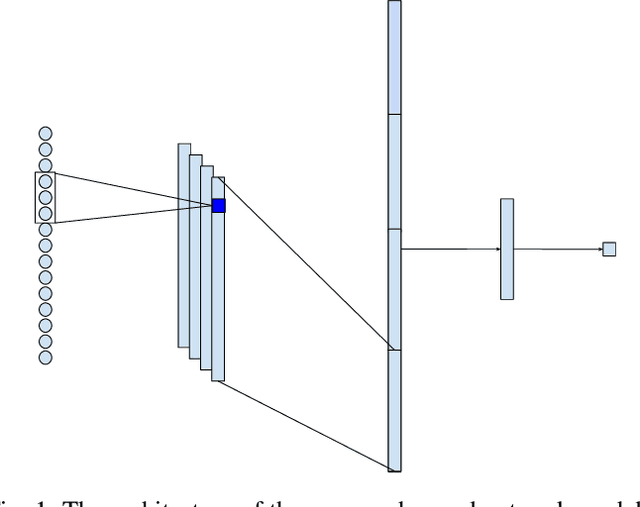

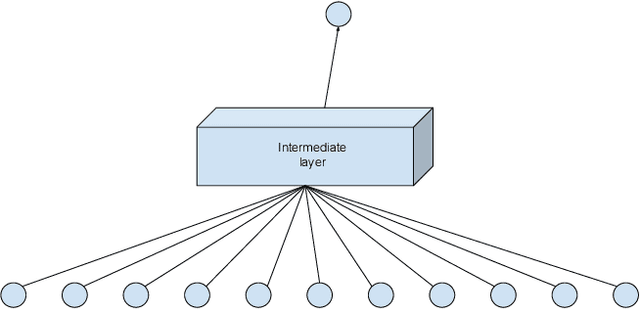

Stock price prediction has been the focus of a large amount of research but an acceptable solution has so far escaped academics. Recent advances in deep learning have motivated researchers to apply neural networks to stock prediction. In this paper, we propose a convolution-based neural network model for predicting the future value of the S&P 500 index. The proposed model is capable of predicting the next-day direction of the index based on the previous values of the index. Experiments show that our model outperforms a number of benchmarks achieving an accuracy rate of over 55%.