Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeStock price forecast with deep learning

Paper and Code

Mar 21, 2021

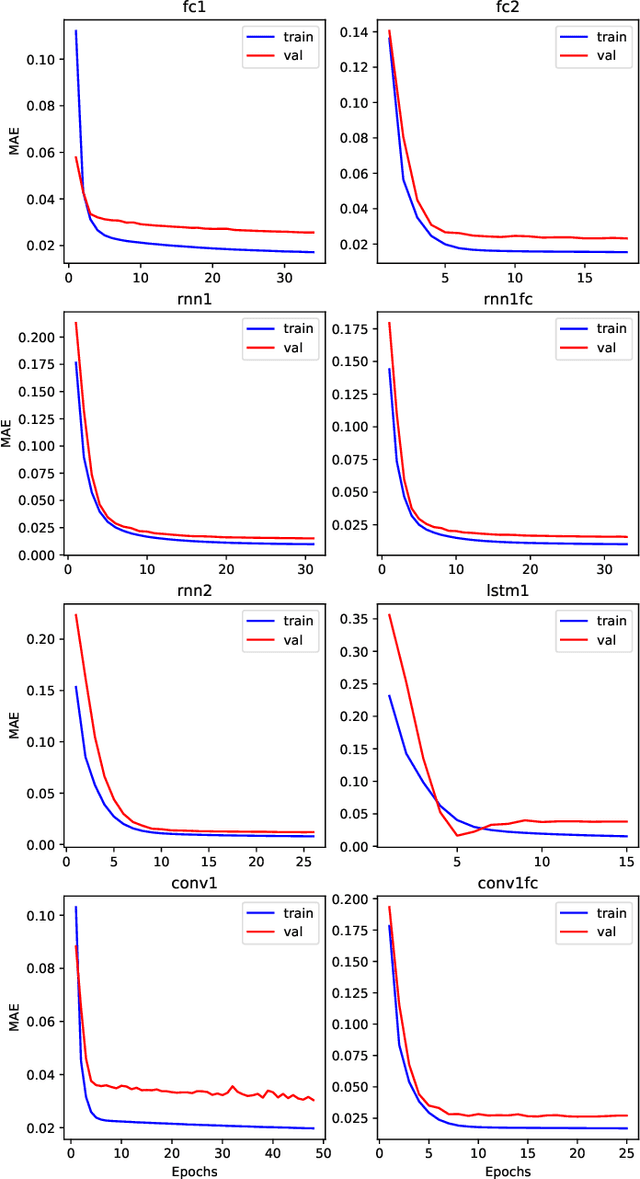

In this paper, we compare various approaches to stock price prediction using neural networks. We analyze the performance fully connected, convolutional, and recurrent architectures in predicting the next day value of S&P 500 index based on its previous values. We further expand our analysis by including three different optimization techniques: Stochastic Gradient Descent, Root Mean Square Propagation, and Adaptive Moment Estimation. The numerical experiments reveal that a single layer recurrent neural network with RMSprop optimizer produces optimal results with validation and test Mean Absolute Error of 0.0150 and 0.0148 respectively.

* Published in: 2020 International Conference on Decision Aid Sciences

and Application (DASA)

View paper on