Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeStock price forecast with deep learning

Mar 21, 2021

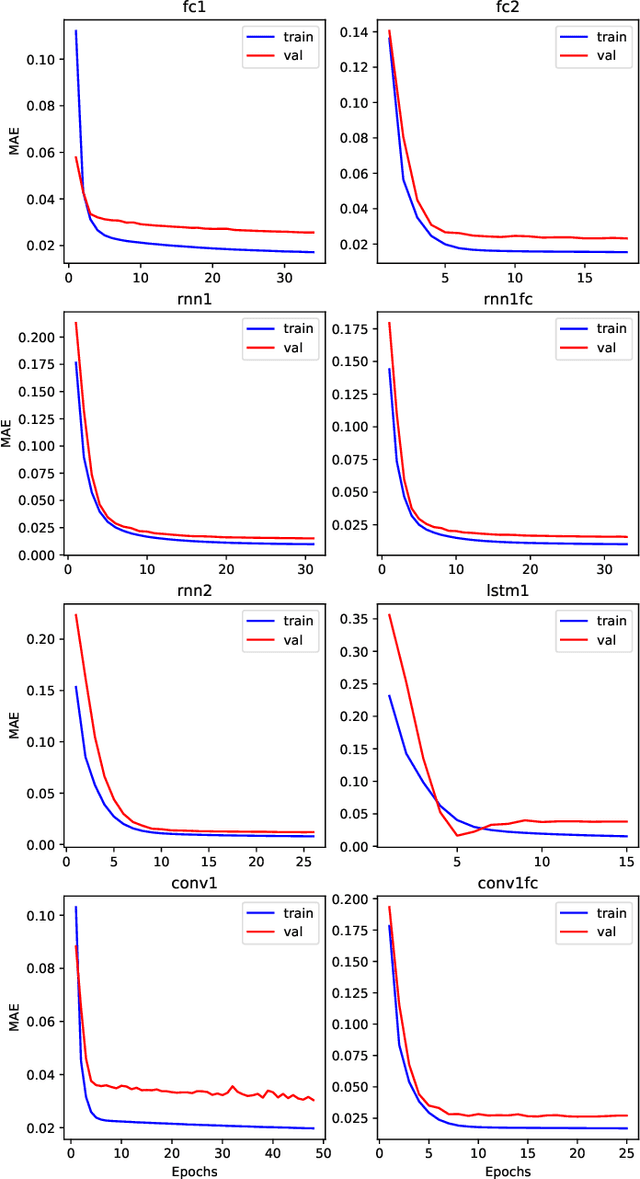

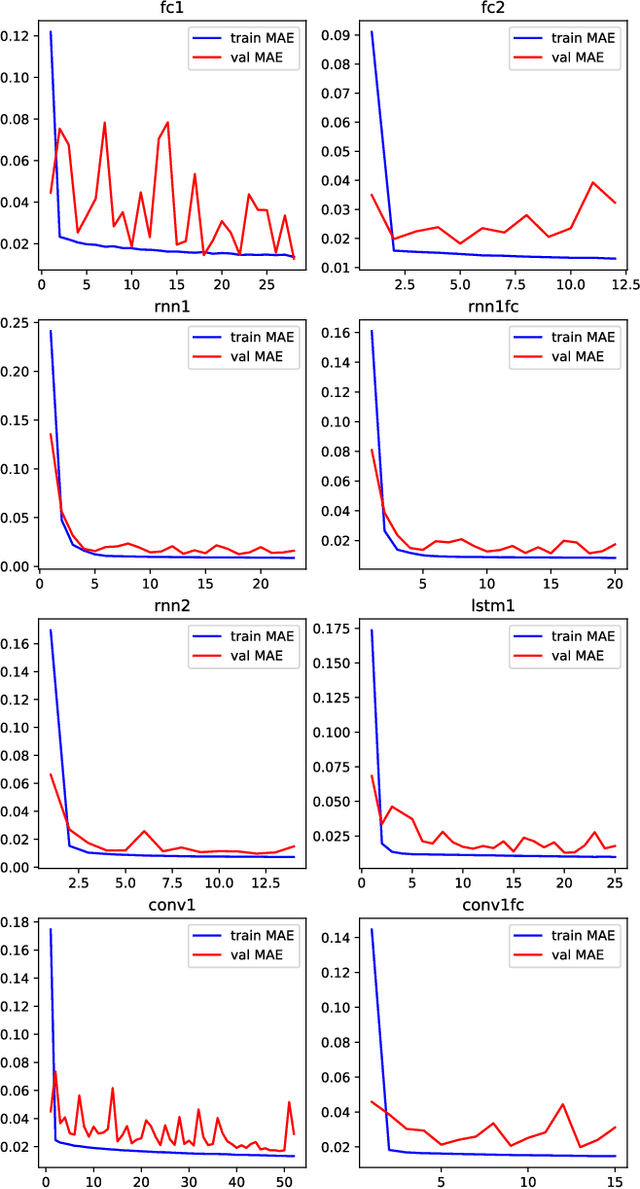

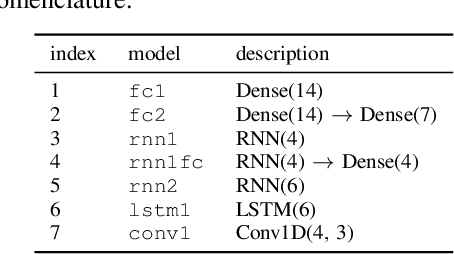

In this paper, we compare various approaches to stock price prediction using neural networks. We analyze the performance fully connected, convolutional, and recurrent architectures in predicting the next day value of S&P 500 index based on its previous values. We further expand our analysis by including three different optimization techniques: Stochastic Gradient Descent, Root Mean Square Propagation, and Adaptive Moment Estimation. The numerical experiments reveal that a single layer recurrent neural network with RMSprop optimizer produces optimal results with validation and test Mean Absolute Error of 0.0150 and 0.0148 respectively.

Forecasting with Deep Learning: S&P 500 index

Mar 21, 2021

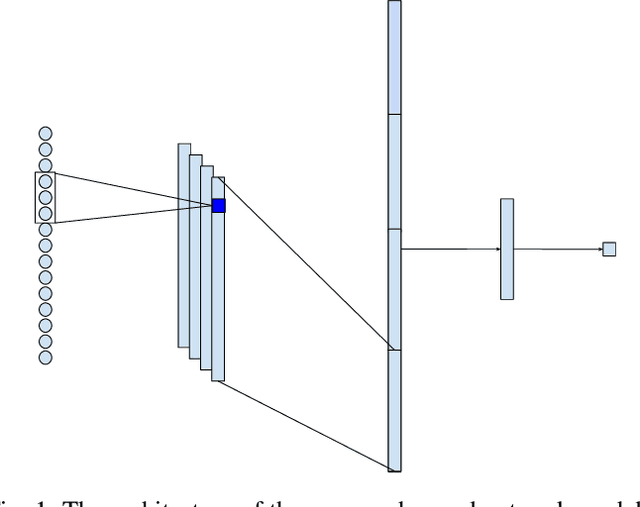

Stock price prediction has been the focus of a large amount of research but an acceptable solution has so far escaped academics. Recent advances in deep learning have motivated researchers to apply neural networks to stock prediction. In this paper, we propose a convolution-based neural network model for predicting the future value of the S&P 500 index. The proposed model is capable of predicting the next-day direction of the index based on the previous values of the index. Experiments show that our model outperforms a number of benchmarks achieving an accuracy rate of over 55%.

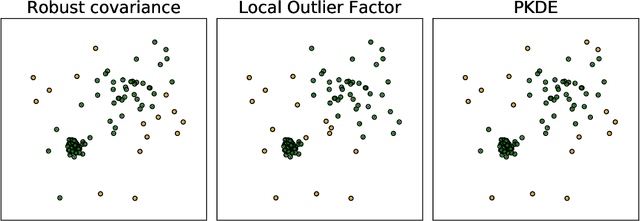

Machine learning based forecasting of significant daily returns in foreign exchange markets

Sep 21, 2020

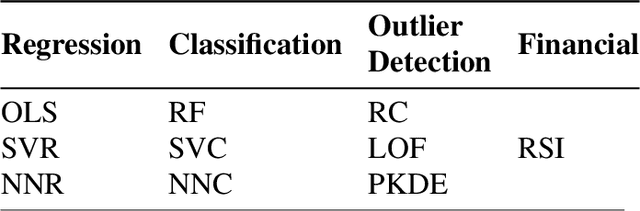

Asset value forecasting has always attracted an enormous amount of interest among researchers in quantitative analysis. The advent of modern machine learning models has introduced new tools to tackle this classical problem. In this paper, we apply machine learning algorithms to hitherto unexplored question of forecasting instances of significant fluctuations in currency exchange rates. We perform analysis of nine modern machine learning algorithms using data on four major currency pairs over a 10 year period. A key contribution is the novel use of outlier detection methods for this purpose. Numerical experiments show that outlier detection methods substantially outperform traditional machine learning and finance techniques. In addition, we show that a recently proposed new outlier detection method PKDE produces best overall results. Our findings hold across different currency pairs, significance levels, and time horizons indicating the robustness of the proposed method.