Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

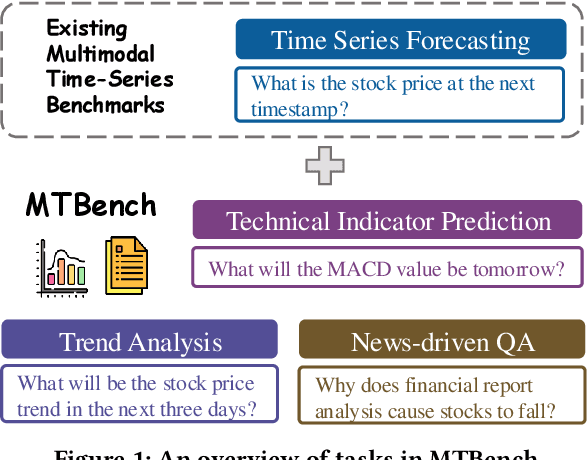

Add to EdgeMTBench: A Multimodal Time Series Benchmark for Temporal Reasoning and Question Answering

Mar 21, 2025

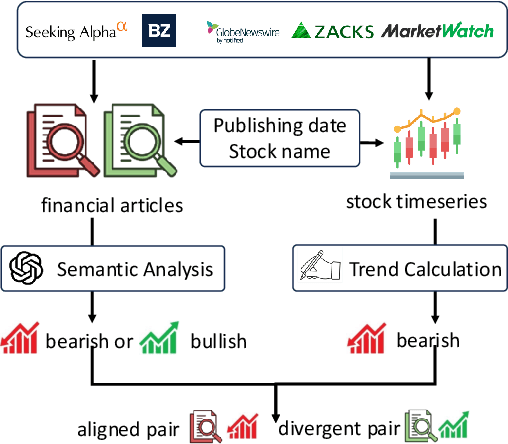

Understanding the relationship between textual news and time-series evolution is a critical yet under-explored challenge in applied data science. While multimodal learning has gained traction, existing multimodal time-series datasets fall short in evaluating cross-modal reasoning and complex question answering, which are essential for capturing complex interactions between narrative information and temporal patterns. To bridge this gap, we introduce Multimodal Time Series Benchmark (MTBench), a large-scale benchmark designed to evaluate large language models (LLMs) on time series and text understanding across financial and weather domains. MTbench comprises paired time series and textual data, including financial news with corresponding stock price movements and weather reports aligned with historical temperature records. Unlike existing benchmarks that focus on isolated modalities, MTbench provides a comprehensive testbed for models to jointly reason over structured numerical trends and unstructured textual narratives. The richness of MTbench enables formulation of diverse tasks that require a deep understanding of both text and time-series data, including time-series forecasting, semantic and technical trend analysis, and news-driven question answering (QA). These tasks target the model's ability to capture temporal dependencies, extract key insights from textual context, and integrate cross-modal information. We evaluate state-of-the-art LLMs on MTbench, analyzing their effectiveness in modeling the complex relationships between news narratives and temporal patterns. Our findings reveal significant challenges in current models, including difficulties in capturing long-term dependencies, interpreting causality in financial and weather trends, and effectively fusing multimodal information.

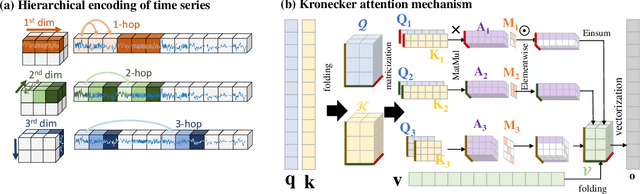

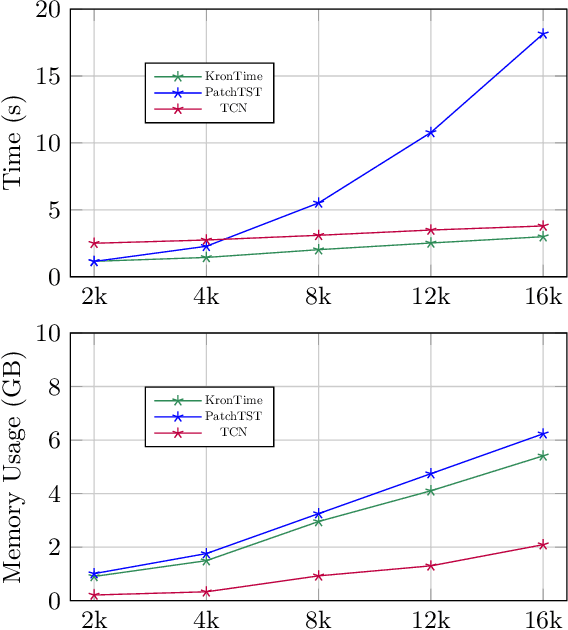

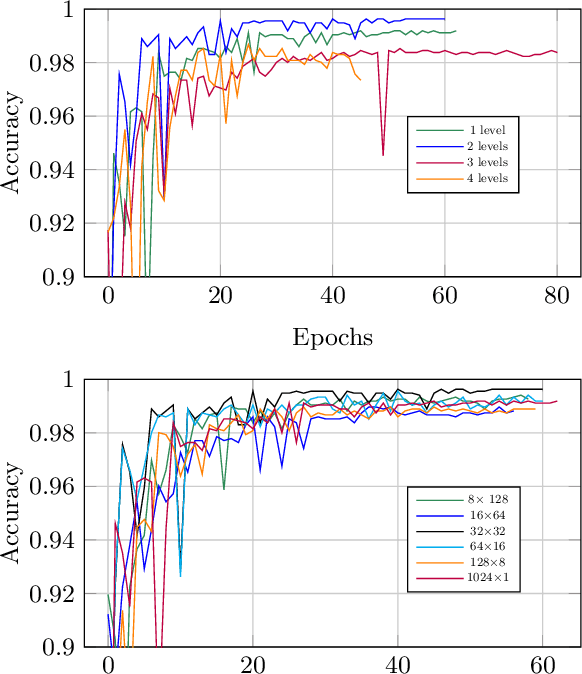

Efficient High-Resolution Time Series Classification via Attention Kronecker Decomposition

Mar 07, 2024

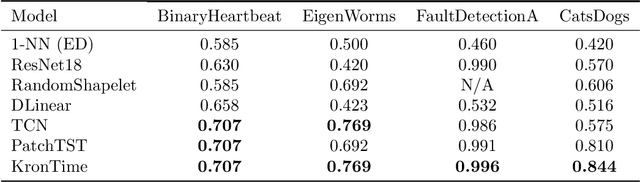

The high-resolution time series classification problem is essential due to the increasing availability of detailed temporal data in various domains. To tackle this challenge effectively, it is imperative that the state-of-the-art attention model is scalable to accommodate the growing sequence lengths typically encountered in high-resolution time series data, while also demonstrating robustness in handling the inherent noise prevalent in such datasets. To address this, we propose to hierarchically encode the long time series into multiple levels based on the interaction ranges. By capturing relationships at different levels, we can build more robust, expressive, and efficient models that are capable of capturing both short-term fluctuations and long-term trends in the data. We then propose a new time series transformer backbone (KronTime) by introducing Kronecker-decomposed attention to process such multi-level time series, which sequentially calculates attention from the lower level to the upper level. Experiments on four long time series datasets demonstrate superior classification results with improved efficiency compared to baseline methods.