Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeZeroS: Zero-Sum Linear Attention for Efficient Transformers

Feb 05, 2026Linear attention methods offer Transformers $O(N)$ complexity but typically underperform standard softmax attention. We identify two fundamental limitations affecting these approaches: the restriction to convex combinations that only permits additive information blending, and uniform accumulated weight bias that dilutes attention in long contexts. We propose Zero-Sum Linear Attention (ZeroS), which addresses these limitations by removing the constant zero-order term $1/t$ and reweighting the remaining zero-sum softmax residuals. This modification creates mathematically stable weights, enabling both positive and negative values and allowing a single attention layer to perform contrastive operations. While maintaining $O(N)$ complexity, ZeroS theoretically expands the set of representable functions compared to convex combinations. Empirically, it matches or exceeds standard softmax attention across various sequence modeling benchmarks.

* Camera-ready version. Accepted at NeurIPS 2025

CAPS: Unifying Attention, Recurrence, and Alignment in Transformer-based Time Series Forecasting

Feb 02, 2026This paper presents $\textbf{CAPS}$ (Clock-weighted Aggregation with Prefix-products and Softmax), a structured attention mechanism for time series forecasting that decouples three distinct temporal structures: global trends, local shocks, and seasonal patterns. Standard softmax attention entangles these through global normalization, while recent recurrent models sacrifice long-term, order-independent selection for order-dependent causal structure. CAPS combines SO(2) rotations for phase alignment with three additive gating paths -- Riemann softmax, prefix-product gates, and a Clock baseline -- within a single attention layer. We introduce the Clock mechanism, a learned temporal weighting that modulates these paths through a shared notion of temporal importance. Experiments on long- and short-term forecasting benchmarks surpass vanilla softmax and linear attention mechanisms and demonstrate competitive performance against seven strong baselines with linear complexity. Our code implementation is available at https://github.com/vireshpati/CAPS-Attention.

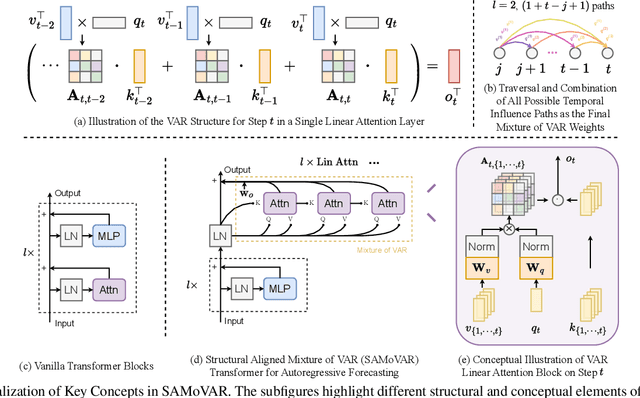

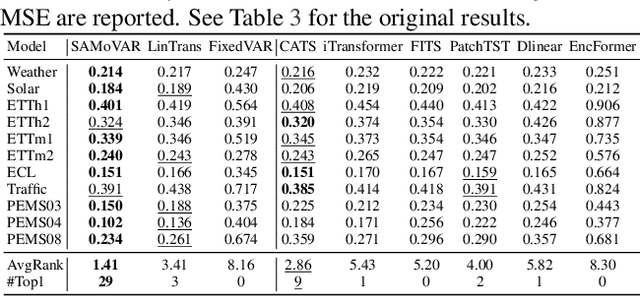

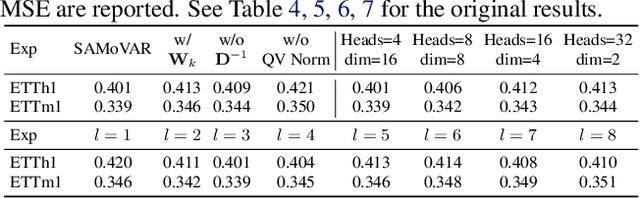

Linear Transformers as VAR Models: Aligning Autoregressive Attention Mechanisms with Autoregressive Forecasting

Feb 11, 2025

Autoregressive attention-based time series forecasting (TSF) has drawn increasing interest, with mechanisms like linear attention sometimes outperforming vanilla attention. However, deeper Transformer architectures frequently misalign with autoregressive objectives, obscuring the underlying VAR structure embedded within linear attention and hindering their ability to capture the data generative processes in TSF. In this work, we first show that a single linear attention layer can be interpreted as a dynamic vector autoregressive (VAR) structure. We then explain that existing multi-layer Transformers have structural mismatches with the autoregressive forecasting objective, which impair interpretability and generalization ability. To address this, we show that by rearranging the MLP, attention, and input-output flow, multi-layer linear attention can also be aligned as a VAR model. Then, we propose Structural Aligned Mixture of VAR (SAMoVAR), a linear Transformer variant that integrates interpretable dynamic VAR weights for multivariate TSF. By aligning the Transformer architecture with autoregressive objectives, SAMoVAR delivers improved performance, interpretability, and computational efficiency, comparing to SOTA TSF models.

Autoregressive Moving-average Attention Mechanism for Time Series Forecasting

Oct 04, 2024

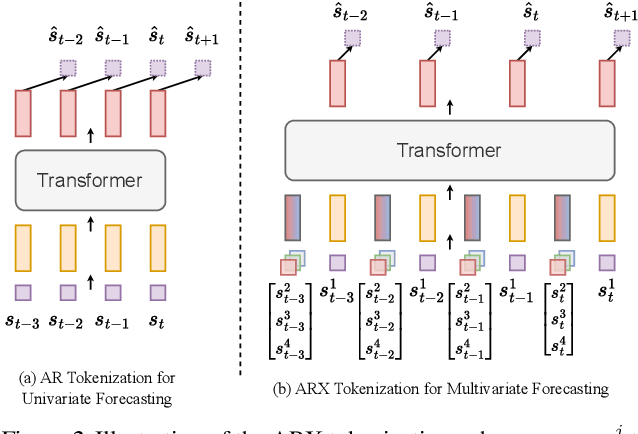

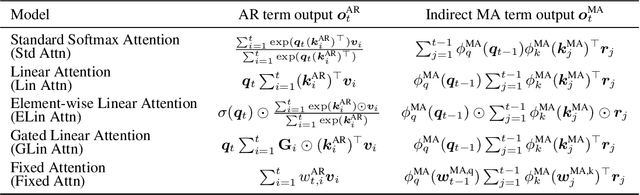

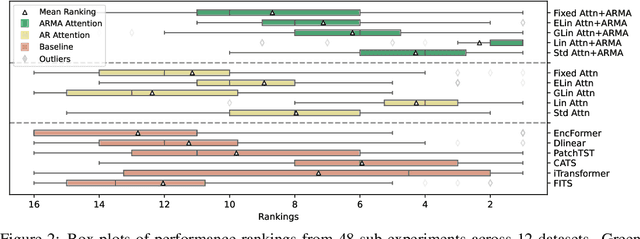

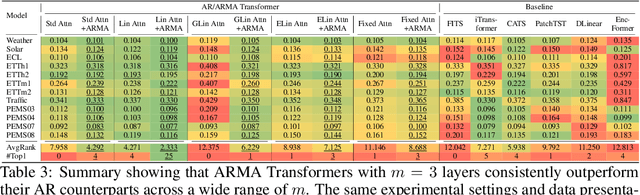

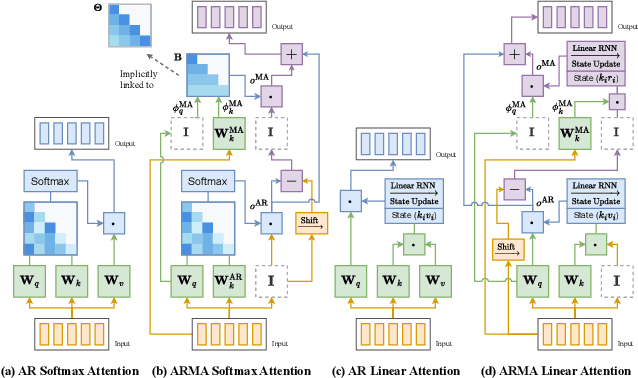

We propose an Autoregressive (AR) Moving-average (MA) attention structure that can adapt to various linear attention mechanisms, enhancing their ability to capture long-range and local temporal patterns in time series. In this paper, we first demonstrate that, for the time series forecasting (TSF) task, the previously overlooked decoder-only autoregressive Transformer model can achieve results comparable to the best baselines when appropriate tokenization and training methods are applied. Moreover, inspired by the ARMA model from statistics and recent advances in linear attention, we introduce the full ARMA structure into existing autoregressive attention mechanisms. By using an indirect MA weight generation method, we incorporate the MA term while maintaining the time complexity and parameter size of the underlying efficient attention models. We further explore how indirect parameter generation can produce implicit MA weights that align with the modeling requirements for local temporal impacts. Experimental results show that incorporating the ARMA structure consistently improves the performance of various AR attentions on TSF tasks, achieving state-of-the-art results.

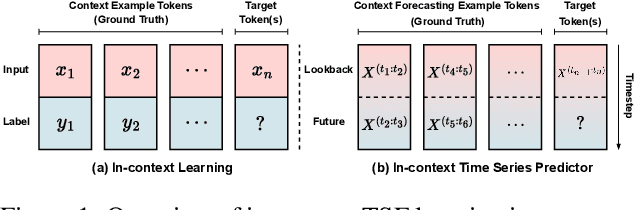

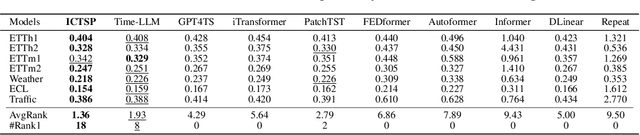

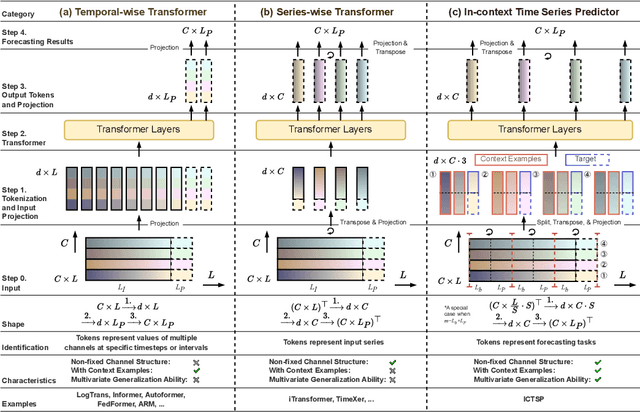

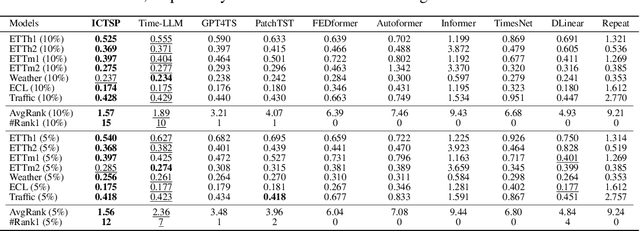

In-context Time Series Predictor

May 23, 2024

Recent Transformer-based large language models (LLMs) demonstrate in-context learning ability to perform various functions based solely on the provided context, without updating model parameters. To fully utilize the in-context capabilities in time series forecasting (TSF) problems, unlike previous Transformer-based or LLM-based time series forecasting methods, we reformulate "time series forecasting tasks" as input tokens by constructing a series of (lookback, future) pairs within the tokens. This method aligns more closely with the inherent in-context mechanisms, and is more parameter-efficient without the need of using pre-trained LLM parameters. Furthermore, it addresses issues such as overfitting in existing Transformer-based TSF models, consistently achieving better performance across full-data, few-shot, and zero-shot settings compared to previous architectures.

CATS: Enhancing Multivariate Time Series Forecasting by Constructing Auxiliary Time Series as Exogenous Variables

Mar 04, 2024For Multivariate Time Series Forecasting (MTSF), recent deep learning applications show that univariate models frequently outperform multivariate ones. To address the difficiency in multivariate models, we introduce a method to Construct Auxiliary Time Series (CATS) that functions like a 2D temporal-contextual attention mechanism, which generates Auxiliary Time Series (ATS) from Original Time Series (OTS) to effectively represent and incorporate inter-series relationships for forecasting. Key principles of ATS - continuity, sparsity, and variability - are identified and implemented through different modules. Even with a basic 2-layer MLP as core predictor, CATS achieves state-of-the-art, significantly reducing complexity and parameters compared to previous multivariate models, marking it an efficient and transferable MTSF solution.

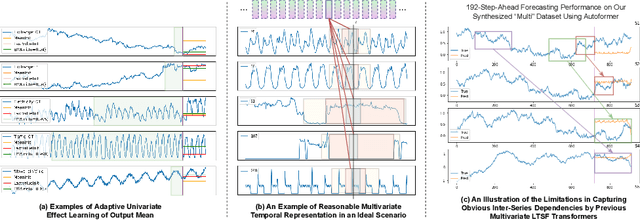

ARM: Refining Multivariate Forecasting with Adaptive Temporal-Contextual Learning

Oct 14, 2023

Long-term time series forecasting (LTSF) is important for various domains but is confronted by challenges in handling the complex temporal-contextual relationships. As multivariate input models underperforming some recent univariate counterparts, we posit that the issue lies in the inefficiency of existing multivariate LTSF Transformers to model series-wise relationships: the characteristic differences between series are often captured incorrectly. To address this, we introduce ARM: a multivariate temporal-contextual adaptive learning method, which is an enhanced architecture specifically designed for multivariate LTSF modelling. ARM employs Adaptive Univariate Effect Learning (AUEL), Random Dropping (RD) training strategy, and Multi-kernel Local Smoothing (MKLS), to better handle individual series temporal patterns and correctly learn inter-series dependencies. ARM demonstrates superior performance on multiple benchmarks without significantly increasing computational costs compared to vanilla Transformer, thereby advancing the state-of-the-art in LTSF. ARM is also generally applicable to other LTSF architecture beyond vanilla Transformer.