Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLearning to Mitigate AI Collusion on Economic Platforms

Feb 15, 2022

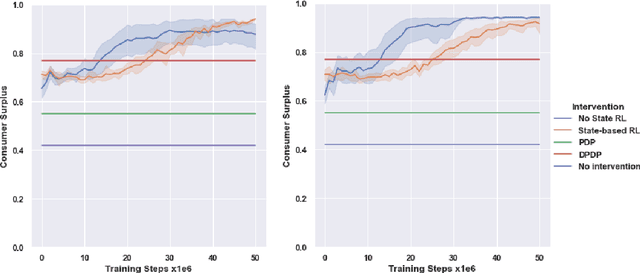

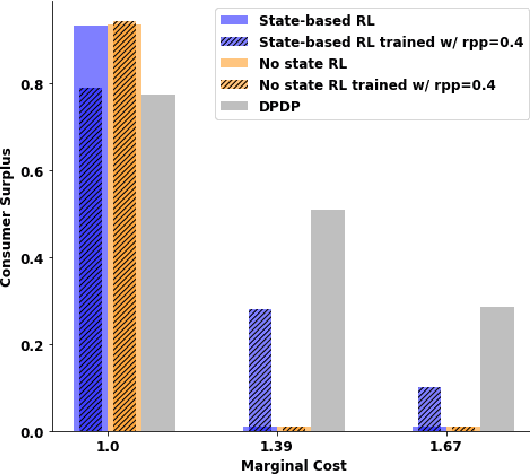

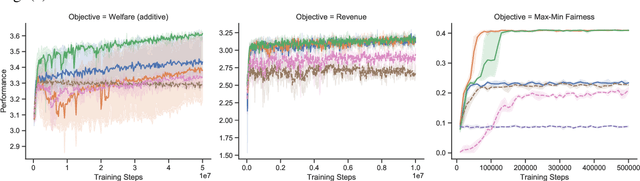

Algorithmic pricing on online e-commerce platforms raises the concern of tacit collusion, where reinforcement learning algorithms learn to set collusive prices in a decentralized manner and through nothing more than profit feedback. This raises the question as to whether collusive pricing can be prevented through the design of suitable "buy boxes," i.e., through the design of the rules that govern the elements of e-commerce sites that promote particular products and prices to consumers. In previous work, Johnson et al. (2020) designed hand-crafted buy box rules that use demand-steering, based on the history of pricing by sellers, to prevent collusive behavior. Although effective against price collusion, these rules effect this by imposing severe restrictions on consumer choice and consumer welfare. In this paper, we demonstrate that reinforcement learning (RL) can also be used by platforms to learn buy box rules that are effective in preventing collusion by RL sellers, and to do so without reducing consumer choice. For this, we adopt the methodology of Stackelberg MDPs, and demonstrate success in learning robust rules that continue to provide high consumer welfare together with sellers employing different behavior models or having out-of-distribution costs for goods.

Reinforcement Learning of Simple Indirect Mechanisms

Oct 02, 2020

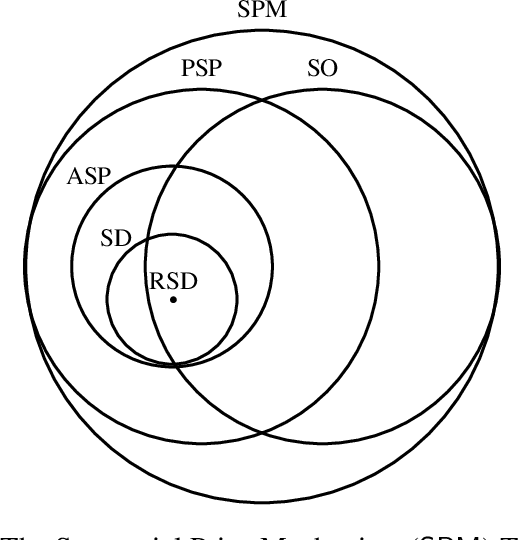

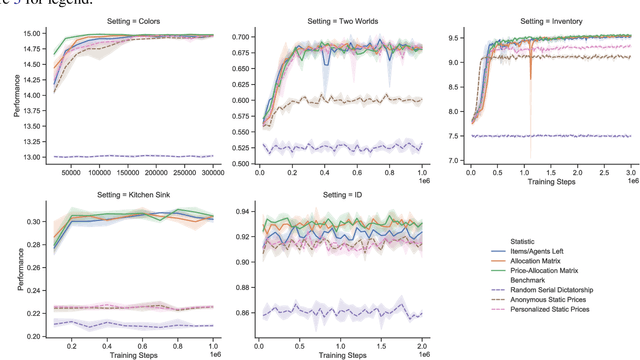

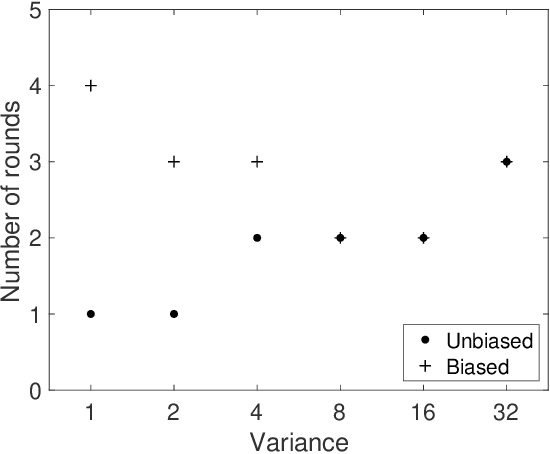

We introduce the use of reinforcement learning for indirect mechanisms, working with the existing class of {\em sequential price mechanisms}, which generalizes both serial dictatorship and posted price mechanisms and essentially characterizes all strongly obviously strategyproof mechanisms. Learning an optimal mechanism within this class forms a partially-observable Markov decision process. We provide rigorous conditions for when this class of mechanisms is more powerful than simpler static mechanisms, for sufficiency or insufficiency of observation statistics for learning, and for the necessity of complex (deep) policies. We show that our approach can learn optimal or near-optimal mechanisms in several experimental settings.

A Bayesian Clearing Mechanism for Combinatorial Auctions

Dec 14, 2017

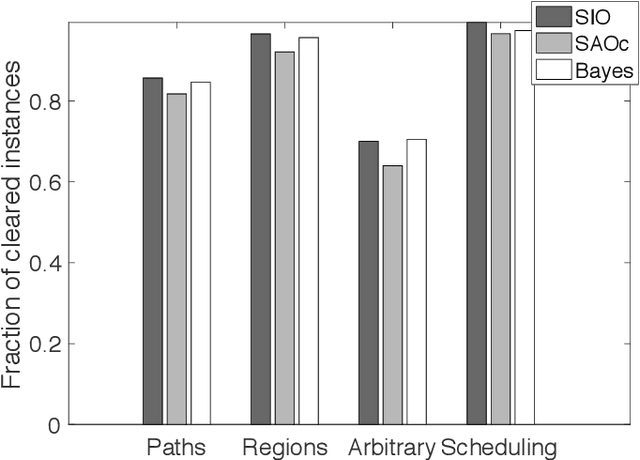

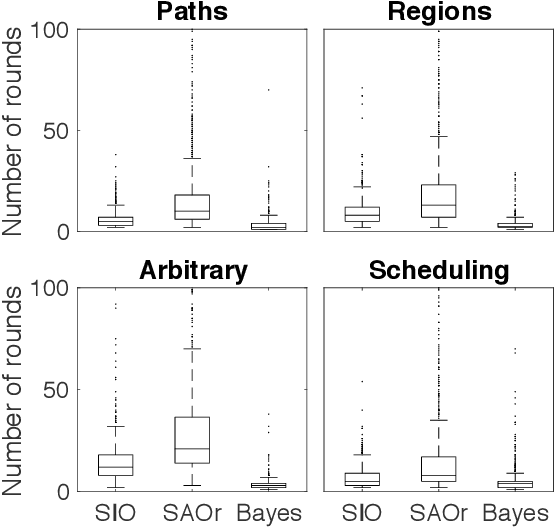

We cast the problem of combinatorial auction design in a Bayesian framework in order to incorporate prior information into the auction process and minimize the number of rounds to convergence. We first develop a generative model of agent valuations and market prices such that clearing prices become maximum a posteriori estimates given observed agent valuations. This generative model then forms the basis of an auction process which alternates between refining estimates of agent valuations and computing candidate clearing prices. We provide an implementation of the auction using assumed density filtering to estimate valuations and expectation maximization to compute prices. An empirical evaluation over a range of valuation domains demonstrates that our Bayesian auction mechanism is highly competitive against the combinatorial clock auction in terms of rounds to convergence, even under the most favorable choices of price increment for this baseline.