Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeHigher Order Kernel Mean Embeddings to Capture Filtrations of Stochastic Processes

Sep 29, 2021

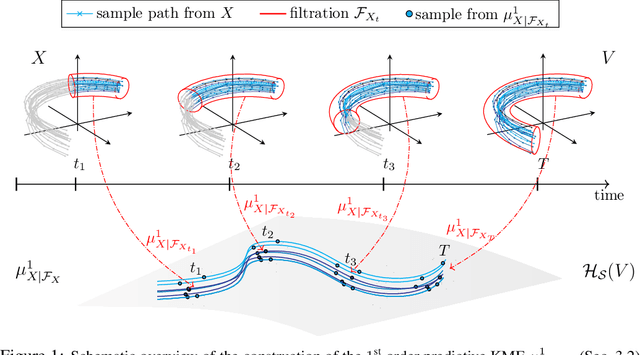

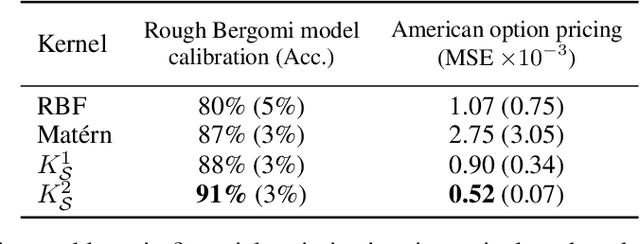

Stochastic processes are random variables with values in some space of paths. However, reducing a stochastic process to a path-valued random variable ignores its filtration, i.e. the flow of information carried by the process through time. By conditioning the process on its filtration, we introduce a family of higher order kernel mean embeddings (KMEs) that generalizes the notion of KME and captures additional information related to the filtration. We derive empirical estimators for the associated higher order maximum mean discrepancies (MMDs) and prove consistency. We then construct a filtration-sensitive kernel two-sample test able to pick up information that gets missed by the standard MMD test. In addition, leveraging our higher order MMDs we construct a family of universal kernels on stochastic processes that allows to solve real-world calibration and optimal stopping problems in quantitative finance (such as the pricing of American options) via classical kernel-based regression methods. Finally, adapting existing tests for conditional independence to the case of stochastic processes, we design a causal-discovery algorithm to recover the causal graph of structural dependencies among interacting bodies solely from observations of their multidimensional trajectories.