Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLearning Sampling in Financial Statement Audits using Vector Quantised Autoencoder Neural Networks

Aug 06, 2020

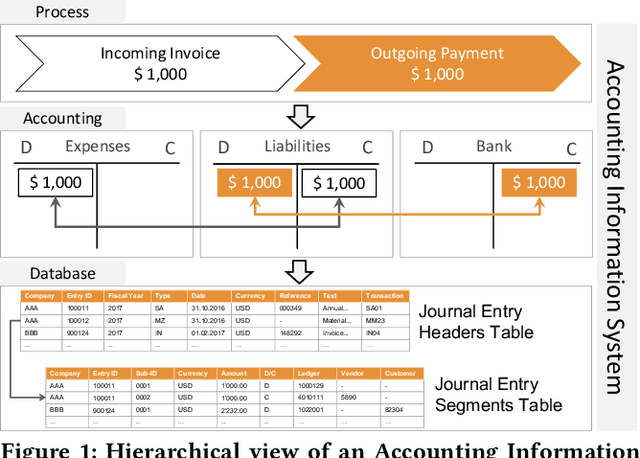

The audit of financial statements is designed to collect reasonable assurance that an issued statement is free from material misstatement 'true and fair presentation'. International audit standards require the assessment of a statements' underlying accounting relevant transactions referred to as 'journal entries' to detect potential misstatements. To efficiently audit the increasing quantities of such entries, auditors regularly conduct a sample-based assessment referred to as 'audit sampling'. However, the task of audit sampling is often conducted early in the overall audit process. Often at a stage, in which an auditor might be unaware of all generative factors and their dynamics that resulted in the journal entries in-scope of the audit. To overcome this challenge, we propose the application of Vector Quantised-Variational Autoencoder (VQ-VAE) neural networks. We demonstrate, based on two real-world city payment datasets, that such artificial neural networks are capable of learning a quantised representation of accounting data. We show that the learned quantisation uncovers (i) the latent factors of variation and (ii) can be utilised as a highly representative audit sample in financial statement audits.

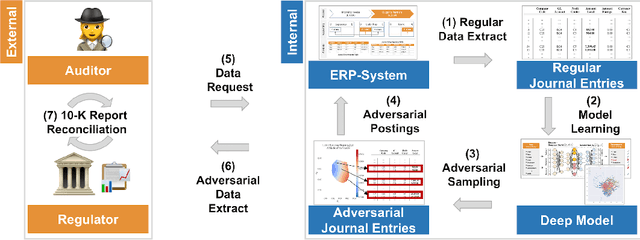

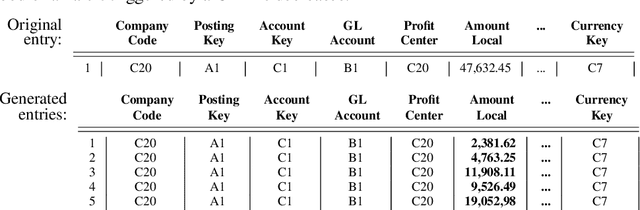

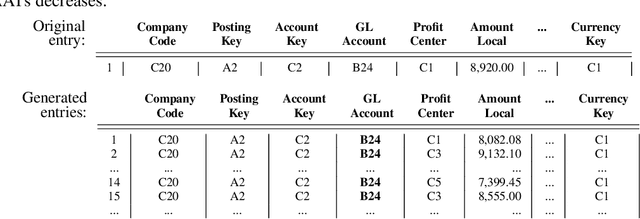

Adversarial Learning of Deepfakes in Accounting

Oct 09, 2019

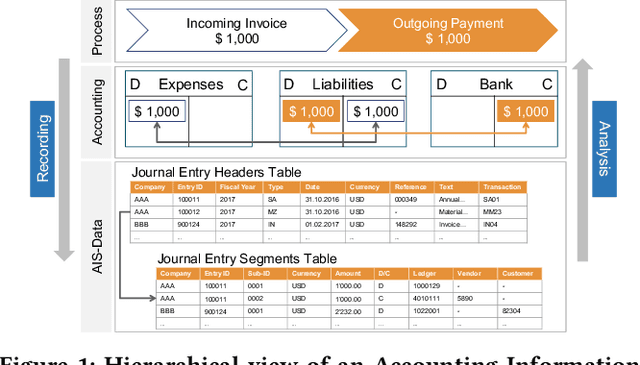

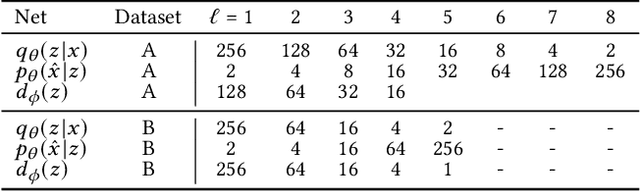

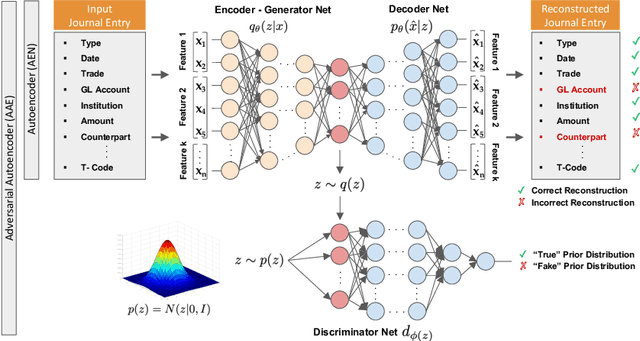

Nowadays, organizations collect vast quantities of accounting relevant transactions, referred to as 'journal entries', in 'Enterprise Resource Planning' (ERP) systems. The aggregation of those entries ultimately defines an organization's financial statement. To detect potential misstatements and fraud, international audit standards demand auditors to directly assess journal entries using 'Computer Assisted AuditTechniques' (CAATs). At the same time, discoveries in deep learning research revealed that machine learning models are vulnerable to 'adversarial attacks'. It also became evident that such attack techniques can be misused to generate 'Deepfakes' designed to directly attack the perception of humans by creating convincingly altered media content. The research of such developments and their potential impact on the finance and accounting domain is still in its early stage. We believe that it is of vital relevance to investigate how such techniques could be maliciously misused in this sphere. In this work, we show an adversarial attack against CAATs using deep neural networks. We first introduce a real-world 'thread model' designed to camouflage accounting anomalies such as fraudulent journal entries. Second, we show that adversarial autoencoder neural networks are capable of learning a human interpretable model of journal entries that disentangles the entries latent generative factors. Finally, we demonstrate how such a model can be maliciously misused by a perpetrator to generate robust 'adversarial' journal entries that mislead CAATs.

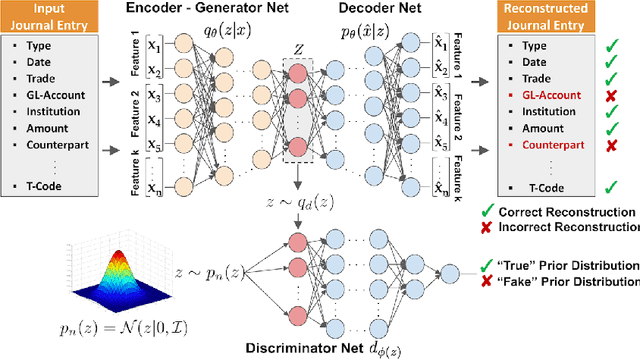

Detection of Accounting Anomalies in the Latent Space using Adversarial Autoencoder Neural Networks

Aug 02, 2019

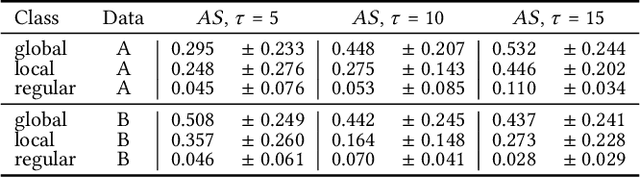

The detection of fraud in accounting data is a long-standing challenge in financial statement audits. Nowadays, the majority of applied techniques refer to handcrafted rules derived from known fraud scenarios. While fairly successful, these rules exhibit the drawback that they often fail to generalize beyond known fraud scenarios and fraudsters gradually find ways to circumvent them. In contrast, more advanced approaches inspired by the recent success of deep learning often lack seamless interpretability of the detected results. To overcome this challenge, we propose the application of adversarial autoencoder networks. We demonstrate that such artificial neural networks are capable of learning a semantic meaningful representation of real-world journal entries. The learned representation provides a holistic view on a given set of journal entries and significantly improves the interpretability of detected accounting anomalies. We show that such a representation combined with the networks reconstruction error can be utilized as an unsupervised and highly adaptive anomaly assessment. Experiments on two datasets and initial feedback received by forensic accountants underpinned the effectiveness of the approach.

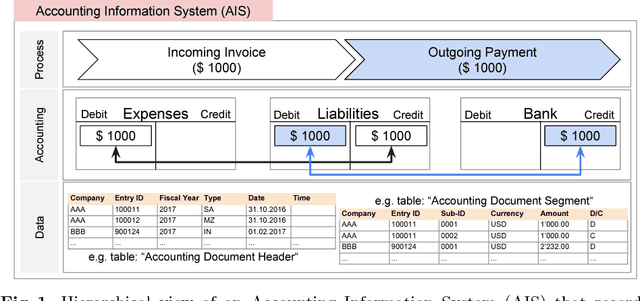

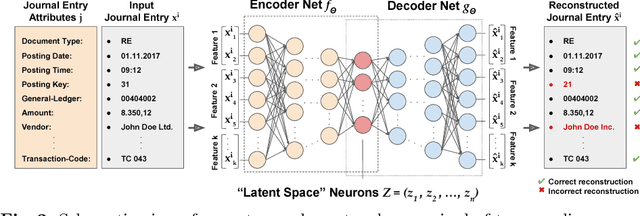

Detection of Anomalies in Large Scale Accounting Data using Deep Autoencoder Networks

Aug 01, 2018

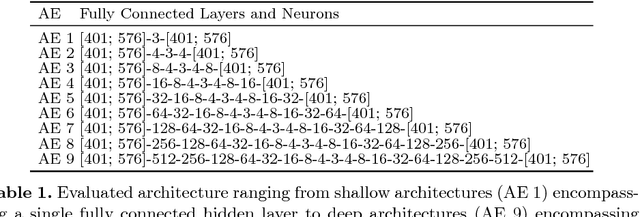

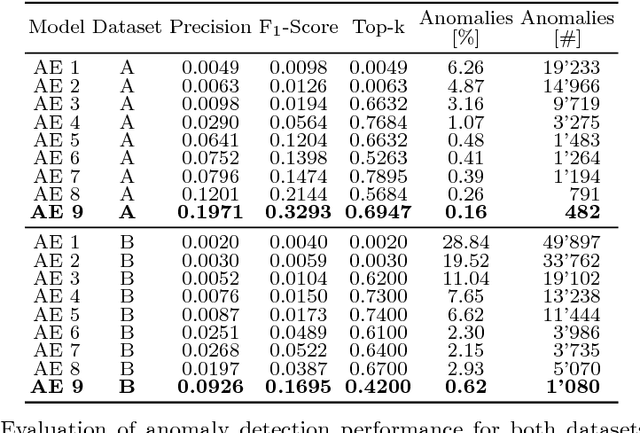

Learning to detect fraud in large-scale accounting data is one of the long-standing challenges in financial statement audits or fraud investigations. Nowadays, the majority of applied techniques refer to handcrafted rules derived from known fraud scenarios. While fairly successful, these rules exhibit the drawback that they often fail to generalize beyond known fraud scenarios and fraudsters gradually find ways to circumvent them. To overcome this disadvantage and inspired by the recent success of deep learning we propose the application of deep autoencoder neural networks to detect anomalous journal entries. We demonstrate that the trained network's reconstruction error obtainable for a journal entry and regularized by the entry's individual attribute probabilities can be interpreted as a highly adaptive anomaly assessment. Experiments on two real-world datasets of journal entries, show the effectiveness of the approach resulting in high f1-scores of 32.93 (dataset A) and 16.95 (dataset B) and less false positive alerts compared to state of the art baseline methods. Initial feedback received by chartered accountants and fraud examiners underpinned the quality of the approach in capturing highly relevant accounting anomalies.