Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeBranches: A Fast Dynamic Programming and Branch & Bound Algorithm for Optimal Decision Trees

Jun 04, 2024

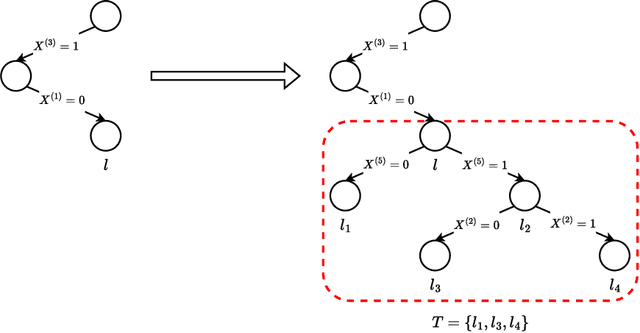

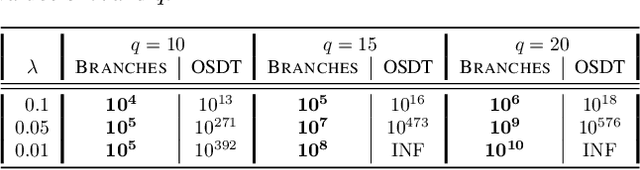

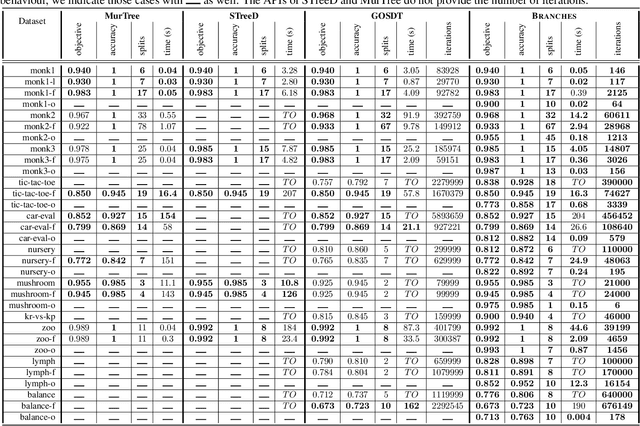

Decision Tree Learning is a fundamental problem for Interpretable Machine Learning, yet it poses a formidable optimization challenge. Despite numerous efforts dating back to the early 1990's, practical algorithms have only recently emerged, primarily leveraging Dynamic Programming (DP) and Branch & Bound (B&B) techniques. These breakthroughs led to the development of two distinct approaches. Algorithms like DL8.5 and MurTree operate on the space of nodes (or branches), they are very fast, but do not penalise complex Decision Trees, i.e. they do not solve for sparsity. On the other hand, algorithms like OSDT and GOSDT operate on the space of Decision Trees, they solve for sparsity but at the detriment of speed. In this work, we introduce Branches, a novel algorithm that integrates the strengths of both paradigms. Leveraging DP and B&B, Branches achieves exceptional speed while also solving for sparsity. Central to its efficiency is a novel analytical bound enabling substantial pruning of the search space. Theoretical analysis demonstrates that Branches has lower complexity compared to state-of-the-art methods, a claim validated through extensive empirical evaluation. Our results illustrate that Branches not only greatly outperforms existing approaches in terms of speed and number of iterations, it also consistently yields optimal Decision Trees.

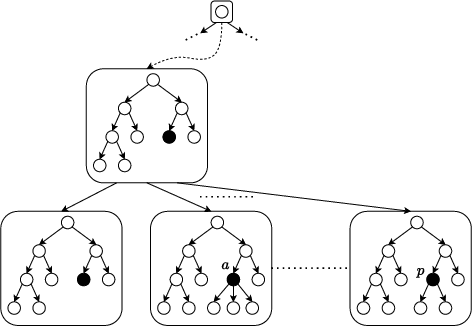

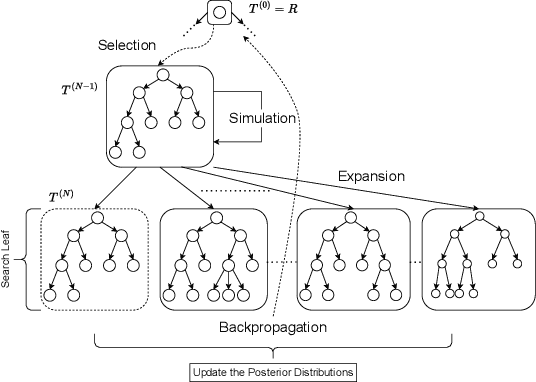

Online Learning of Decision Trees with Thompson Sampling

Apr 09, 2024

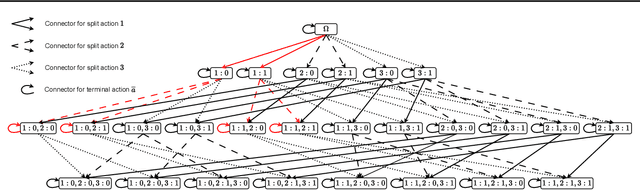

Decision Trees are prominent prediction models for interpretable Machine Learning. They have been thoroughly researched, mostly in the batch setting with a fixed labelled dataset, leading to popular algorithms such as C4.5, ID3 and CART. Unfortunately, these methods are of heuristic nature, they rely on greedy splits offering no guarantees of global optimality and often leading to unnecessarily complex and hard-to-interpret Decision Trees. Recent breakthroughs addressed this suboptimality issue in the batch setting, but no such work has considered the online setting with data arriving in a stream. To this end, we devise a new Monte Carlo Tree Search algorithm, Thompson Sampling Decision Trees (TSDT), able to produce optimal Decision Trees in an online setting. We analyse our algorithm and prove its almost sure convergence to the optimal tree. Furthermore, we conduct extensive experiments to validate our findings empirically. The proposed TSDT outperforms existing algorithms on several benchmarks, all while presenting the practical advantage of being tailored to the online setting.

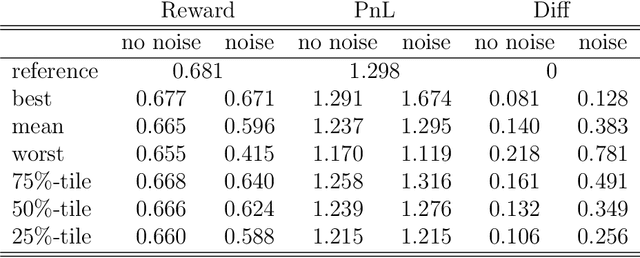

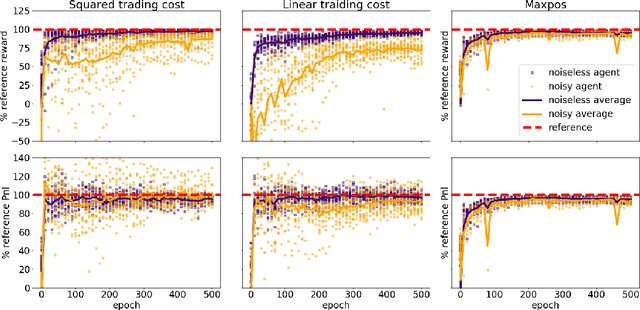

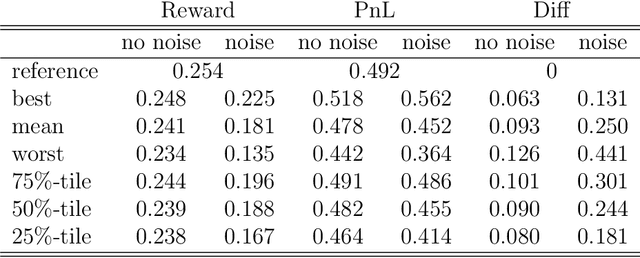

Deep Deterministic Portfolio Optimization

Apr 09, 2020

Can deep reinforcement learning algorithms be exploited as solvers for optimal trading strategies? The aim of this work is to test reinforcement learning algorithms on conceptually simple, but mathematically non-trivial, trading environments. The environments are chosen such that an optimal or close-to-optimal trading strategy is known. We study the deep deterministic policy gradient algorithm and show that such a reinforcement learning agent can successfully recover the essential features of the optimal trading strategies and achieve close-to-optimal rewards.