Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgePlug-in Regularized Estimation of High-Dimensional Parameters in Nonlinear Semiparametric Models

Paper and Code

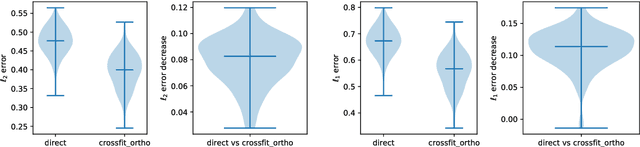

We develop a theory for estimation of a high-dimensional sparse parameter $\theta$ defined as a minimizer of a population loss function $L_D(\theta,g_0)$ which, in addition to $\theta$, depends on a, potentially infinite dimensional, nuisance parameter $g_0$. Our approach is based on estimating $\theta$ via an $\ell_1$-regularized minimization of a sample analog of $L_S(\theta, \hat{g})$, plugging in a first-stage estimate $\hat{g}$, computed on a hold-out sample. We define a population loss to be (Neyman) orthogonal if the gradient of the loss with respect to $\theta$, has pathwise derivative with respect to $g$ equal to zero, when evaluated at the true parameter and nuisance component. We show that orthogonality implies a second-order impact of the first stage nuisance error on the second stage target parameter estimate. Our approach applies to both convex and non-convex losses, albeit the latter case requires a small adaptation of our method with a preliminary estimation step of the target parameter. Our result enables oracle convergence rates for $\theta$ under assumptions on the first stage rates, typically of the order of $n^{-1/4}$. We show how such an orthogonal loss can be constructed via a novel orthogonalization process for a general model defined by conditional moment restrictions. We apply our theory to high-dimensional versions of standard estimation problems in statistics and econometrics, such as: estimation of conditional moment models with missing data, estimation of structural utilities in games of incomplete information and estimation of treatment effects in regression models with non-linear link functions.