Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeNonstationary Portfolios: Diversification in the Spectral Domain

Paper and Code

Jan 31, 2021

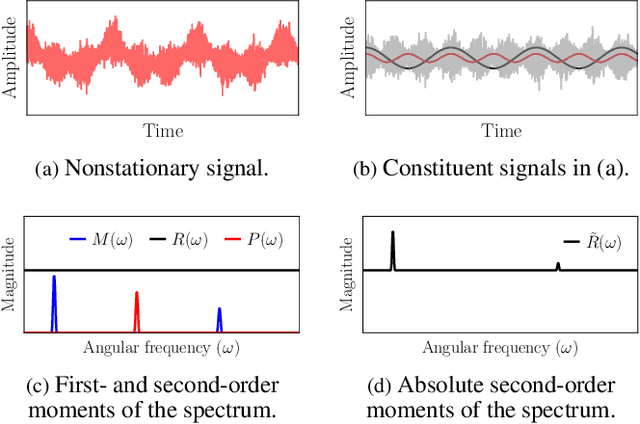

Classical portfolio optimization methods typically determine an optimal capital allocation through the implicit, yet critical, assumption of statistical time-invariance. Such models are inadequate for real-world markets as they employ standard time-averaging based estimators which suffer significant information loss if the market observables are non-stationary. To this end, we reformulate the portfolio optimization problem in the spectral domain to cater for the nonstationarity inherent to asset price movements and, in this way, allow for optimal capital allocations to be time-varying. Unlike existing spectral portfolio techniques, the proposed framework employs augmented complex statistics in order to exploit the interactions between the real and imaginary parts of the complex spectral variables, which in turn allows for the modelling of both harmonics and cyclostationarity in the time domain. The advantages of the proposed framework over traditional methods are demonstrated through numerical simulations using real-world price data.