Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLearning Multiple Stock Trading Patterns with Temporal Routing Adaptor and Optimal Transport

Paper and Code

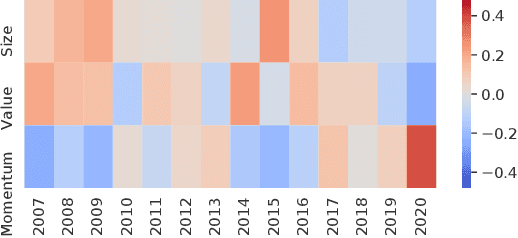

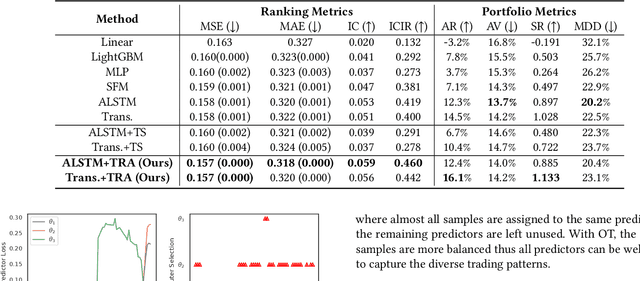

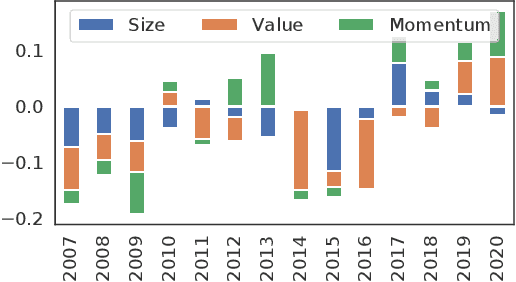

Successful quantitative investment usually relies on precise predictions of the future movement of the stock price. Recently, machine learning based solutions have shown their capacity to give more accurate stock prediction and become indispensable components in modern quantitative investment systems. However, the i.i.d. assumption behind existing methods is inconsistent with the existence of diverse trading patterns in the stock market, which inevitably limits their ability to achieve better stock prediction performance. In this paper, we propose a novel architecture, Temporal Routing Adaptor (TRA), to empower existing stock prediction models with the ability to model multiple stock trading patterns. Essentially, TRA is a lightweight module that consists of a set of independent predictors for learning multiple patterns as well as a router to dispatch samples to different predictors. Nevertheless, the lack of explicit pattern identifiers makes it quite challenging to train an effective TRA-based model. To tackle this challenge, we further design a learning algorithm based on Optimal Transport (OT) to obtain the optimal sample to predictor assignment and effectively optimize the router with such assignment through an auxiliary loss term. Experiments on the real-world stock ranking task show that compared to the state-of-the-art baselines, e.g., Attention LSTM and Transformer, the proposed method can improve information coefficient (IC) from 0.053 to 0.059 and 0.051 to 0.056 respectively. Our dataset and code used in this work are publicly available: https://github.com/microsoft/qlib/tree/main/examples/benchmarks/TRA.