Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeIntegrating LLM-Generated Views into Mean-Variance Optimization Using the Black-Litterman Model

Paper and Code

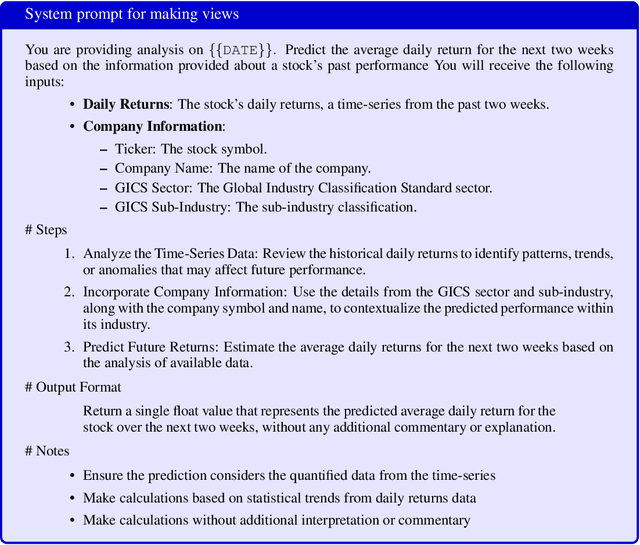

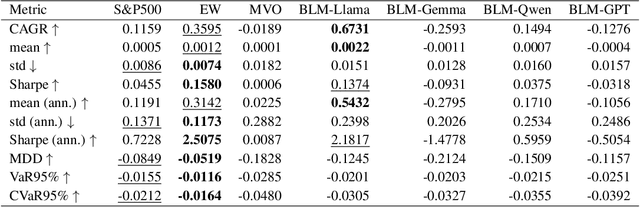

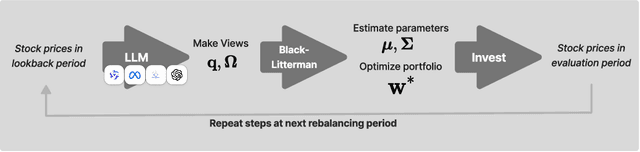

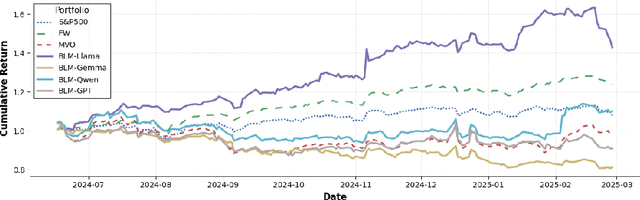

Portfolio optimization faces challenges due to the sensitivity in traditional mean-variance models. The Black-Litterman model mitigates this by integrating investor views, but defining these views remains difficult. This study explores the integration of large language models (LLMs) generated views into portfolio optimization using the Black-Litterman framework. Our method leverages LLMs to estimate expected stock returns from historical prices and company metadata, incorporating uncertainty through the variance in predictions. We conduct a backtest of the LLM-optimized portfolios from June 2024 to February 2025, rebalancing biweekly using the previous two weeks of price data. As baselines, we compare against the S&P 500, an equal-weighted portfolio, and a traditional mean-variance optimized portfolio constructed using the same set of stocks. Empirical results suggest that different LLMs exhibit varying levels of predictive optimism and confidence stability, which impact portfolio performance. The source code and data are available at https://github.com/youngandbin/LLM-MVO-BLM.