Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeGroup, Extract and Aggregate: Summarizing a Large Amount of Finance News for Forex Movement Prediction

Paper and Code

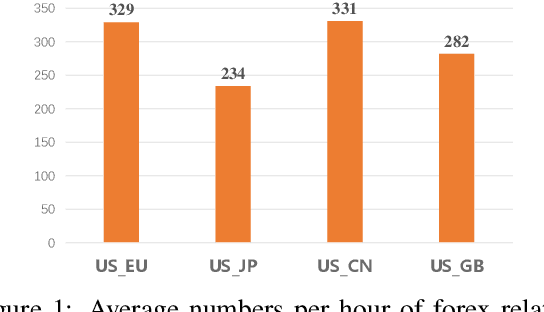

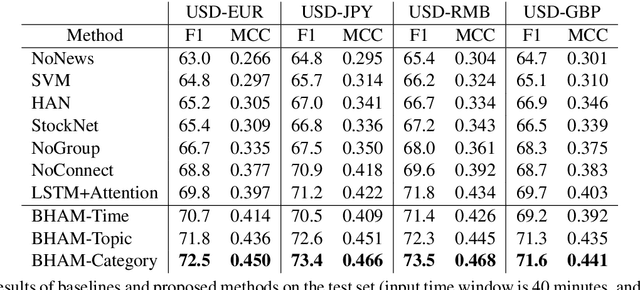

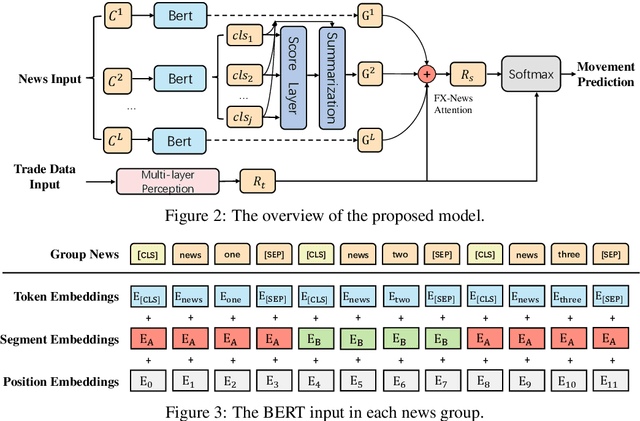

Incorporating related text information has proven successful in stock market prediction. However, it is a huge challenge to utilize texts in the enormous forex (foreign currency exchange) market because the associated texts are too redundant. In this work, we propose a BERT-based Hierarchical Aggregation Model to summarize a large amount of finance news to predict forex movement. We firstly group news from different aspects: time, topic and category. Then we extract the most crucial news in each group by the SOTA extractive summarization method. Finally, we conduct interaction between the news and the trade data with attention to predict the forex movement. The experimental results show that the category based method performs best among three grouping methods and outperforms all the baselines. Besides, we study the influence of essential news attributes (category and region) by statistical analysis and summarize the influence patterns for different currency pairs.