Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeFortia-FBK at SemEval-2017 Task 5: Bullish or Bearish? Inferring Sentiment towards Brands from Financial News Headlines

Paper and Code

Apr 04, 2017

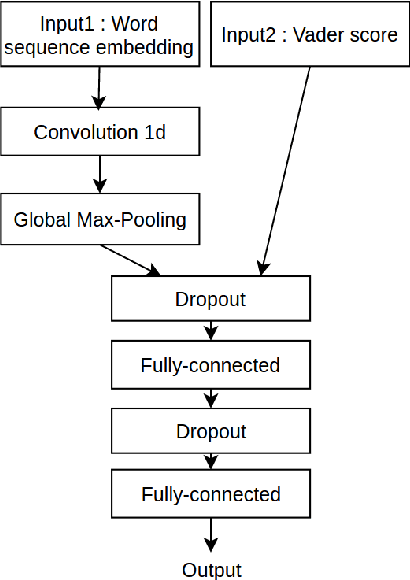

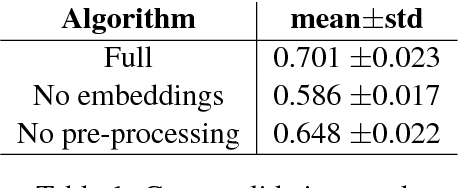

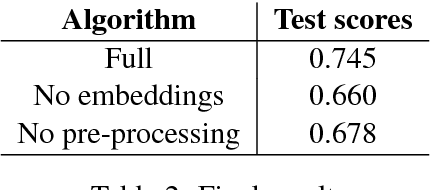

In this paper, we describe a methodology to infer Bullish or Bearish sentiment towards companies/brands. More specifically, our approach leverages affective lexica and word embeddings in combination with convolutional neural networks to infer the sentiment of financial news headlines towards a target company. Such architecture was used and evaluated in the context of the SemEval 2017 challenge (task 5, subtask 2), in which it obtained the best performance.

* 6 pages, 1 figure; accepted for publication at the International

Workshop on Semantic Evaluation (SemEval-2017) to be held in conjunction with

ACL 2017

View paper on