Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDGDNN: Decoupled Graph Diffusion Neural Network for Stock Movement Prediction

Paper and Code

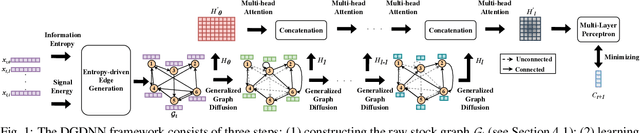

Forecasting future stock trends remains challenging for academia and industry due to stochastic inter-stock dynamics and hierarchical intra-stock dynamics influencing stock prices. In recent years, graph neural networks have achieved remarkable performance in this problem by formulating multiple stocks as graph-structured data. However, most of these approaches rely on artificially defined factors to construct static stock graphs, which fail to capture the intrinsic interdependencies between stocks that rapidly evolve. In addition, these methods often ignore the hierarchical features of the stocks and lose distinctive information within. In this work, we propose a novel graph learning approach implemented without expert knowledge to address these issues. First, our approach automatically constructs dynamic stock graphs by entropy-driven edge generation from a signal processing perspective. Then, we further learn task-optimal dependencies between stocks via a generalized graph diffusion process on constructed stock graphs. Last, a decoupled representation learning scheme is adopted to capture distinctive hierarchical intra-stock features. Experimental results demonstrate substantial improvements over state-of-the-art baselines on real-world datasets. Moreover, the ablation study and sensitivity study further illustrate the effectiveness of the proposed method in modeling the time-evolving inter-stock and intra-stock dynamics.