Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeDeep Risk Model: A Deep Learning Solution for Mining Latent Risk Factors to Improve Covariance Matrix Estimation

Paper and Code

Jul 12, 2021

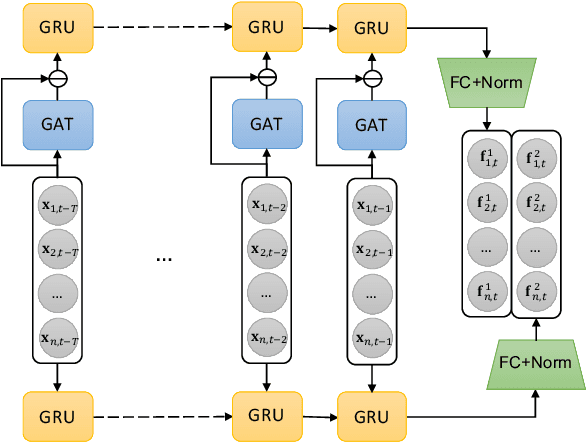

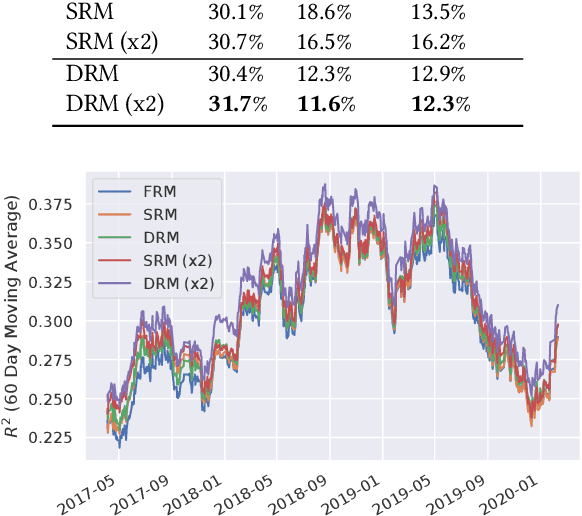

Modeling and managing portfolio risk is perhaps the most important step to achieve growing and preserving investment performance. Within the modern portfolio construction framework that built on Markowitz's theory, the covariance matrix of stock returns is required to model the portfolio risk. Traditional approaches to estimate the covariance matrix are based on human designed risk factors, which often requires tremendous time and effort to design better risk factors to improve the covariance estimation. In this work, we formulate the quest of mining risk factors as a learning problem and propose a deep learning solution to effectively "design" risk factors with neural networks. The learning objective is carefully set to ensure the learned risk factors are effective in explaining stock returns as well as have desired orthogonality and stability. Our experiments on the stock market data demonstrate the effectiveness of the proposed method: our method can obtain $1.9\%$ higher explained variance measured by $R^2$ and also reduce the risk of a global minimum variance portfolio. Incremental analysis further supports our design of both the architecture and the learning objective.