Get our free extension to see links to code for papers anywhere online!Free add-on: code for papers everywhere!Free add-on: See code for papers anywhere!

Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeApproximate Bayesian Inference in Linear State Space Models for Intermittent Demand Forecasting at Scale

Paper and Code

Sep 22, 2017

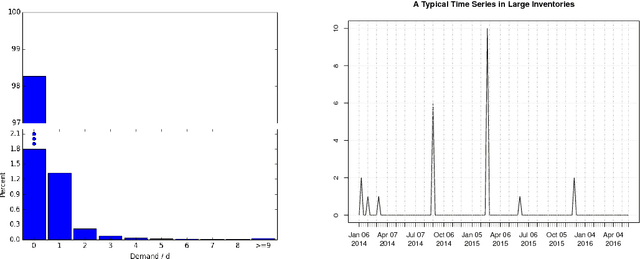

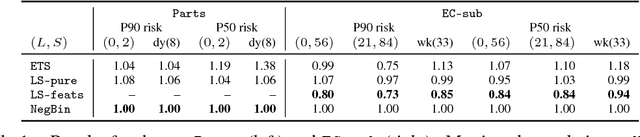

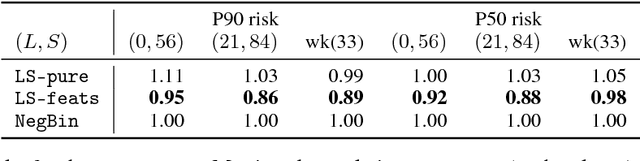

We present a scalable and robust Bayesian inference method for linear state space models. The method is applied to demand forecasting in the context of a large e-commerce platform, paying special attention to intermittent and bursty target statistics. Inference is approximated by the Newton-Raphson algorithm, reduced to linear-time Kalman smoothing, which allows us to operate on several orders of magnitude larger problems than previous related work. In a study on large real-world sales datasets, our method outperforms competing approaches on fast and medium moving items.

View paper on