Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA novel robust meta-analysis model using the $t$ distribution for outlier accommodation and detection

Paper and Code

Jun 06, 2024

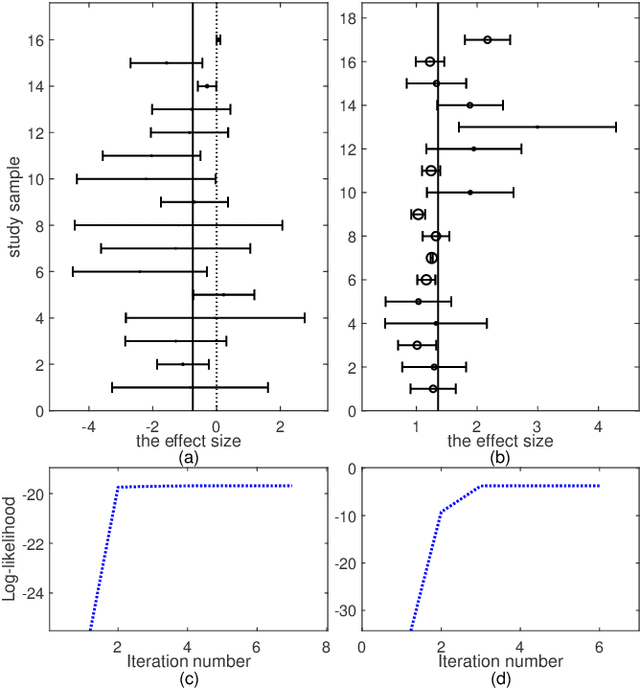

Random effects meta-analysis model is an important tool for integrating results from multiple independent studies. However, the standard model is based on the assumption of normal distributions for both random effects and within-study errors, making it susceptible to outlying studies. Although robust modeling using the $t$ distribution is an appealing idea, the existing work, that explores the use of the $t$ distribution only for random effects, involves complicated numerical integration and numerical optimization. In this paper, a novel robust meta-analysis model using the $t$ distribution is proposed ($t$Meta). The novelty is that the marginal distribution of the effect size in $t$Meta follows the $t$ distribution, enabling that $t$Meta can simultaneously accommodate and detect outlying studies in a simple and adaptive manner. A simple and fast EM-type algorithm is developed for maximum likelihood estimation. Due to the mathematical tractability of the $t$ distribution, $t$Meta frees from numerical integration and allows for efficient optimization. Experiments on real data demonstrate that $t$Meta is compared favorably with related competitors in situations involving mild outliers. Moreover, in the presence of gross outliers, while related competitors may fail, $t$Meta continues to perform consistently and robustly.