Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA Distributionally Robust Boosting Algorithm

Paper and Code

May 20, 2019

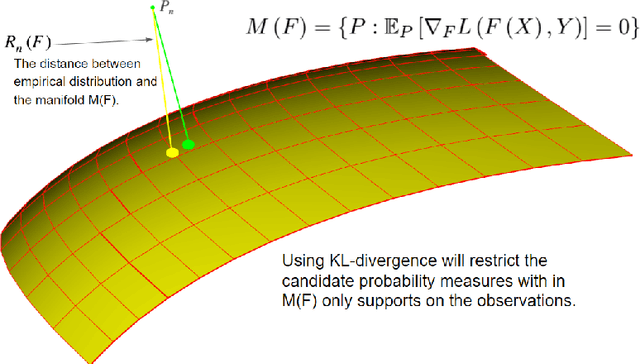

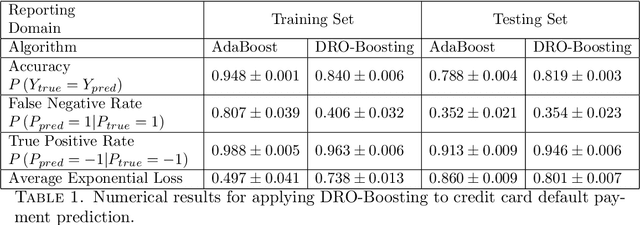

Distributionally Robust Optimization (DRO) has been shown to provide a flexible framework for decision making under uncertainty and statistical estimation. For example, recent works in DRO have shown that popular statistical estimators can be interpreted as the solutions of suitable formulated data-driven DRO problems. In turn, this connection is used to optimally select tuning parameters in terms of a principled approach informed by robustness considerations. This paper contributes to this growing literature, connecting DRO and statistics, by showing how boosting algorithms can be studied via DRO. We propose a boosting type algorithm, named DRO-Boosting, as a procedure to solve our DRO formulation. Our DRO-Boosting algorithm recovers Adaptive Boosting (AdaBoost) in particular, thus showing that AdaBoost is effectively solving a DRO problem. We apply our algorithm to a financial dataset on credit card default payment prediction. We find that our approach compares favorably to alternative boosting methods which are widely used in practice.