Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLarge Language Model in Financial Regulatory Interpretation

May 10, 2024This study explores the innovative use of Large Language Models (LLMs) as analytical tools for interpreting complex financial regulations. The primary objective is to design effective prompts that guide LLMs in distilling verbose and intricate regulatory texts, such as the Basel III capital requirement regulations, into a concise mathematical framework that can be subsequently translated into actionable code. This novel approach aims to streamline the implementation of regulatory mandates within the financial reporting and risk management systems of global banking institutions. A case study was conducted to assess the performance of various LLMs, demonstrating that GPT-4 outperforms other models in processing and collecting necessary information, as well as executing mathematical calculations. The case study utilized numerical simulations with asset holdings -- including fixed income, equities, currency pairs, and commodities -- to demonstrate how LLMs can effectively implement the Basel III capital adequacy requirements.

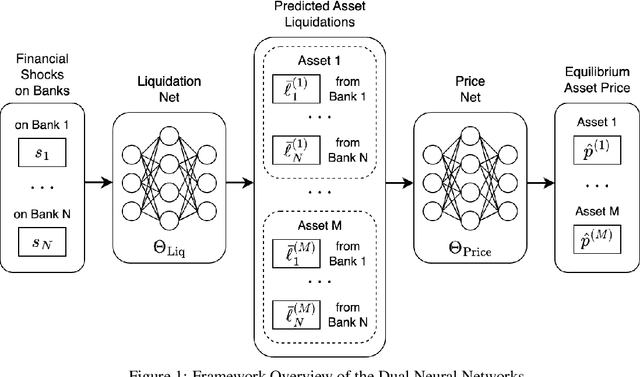

Modeling Inverse Demand Function with Explainable Dual Neural Networks

Jul 26, 2023

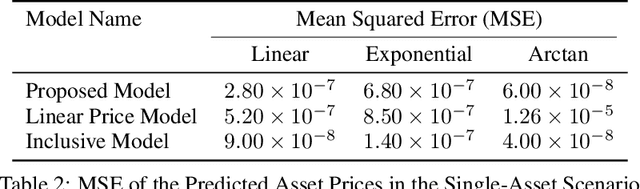

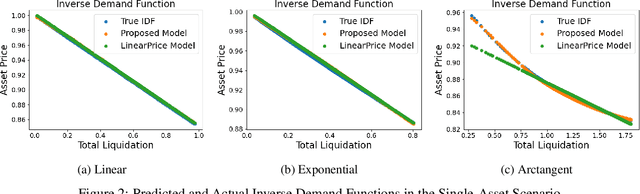

Financial contagion has been widely recognized as a fundamental risk to the financial system. Particularly potent is price-mediated contagion, wherein forced liquidations by firms depress asset prices and propagate financial stress, enabling crises to proliferate across a broad spectrum of seemingly unrelated entities. Price impacts are currently modeled via exogenous inverse demand functions. However, in real-world scenarios, only the initial shocks and the final equilibrium asset prices are typically observable, leaving actual asset liquidations largely obscured. This missing data presents significant limitations to calibrating the existing models. To address these challenges, we introduce a novel dual neural network structure that operates in two sequential stages: the first neural network maps initial shocks to predicted asset liquidations, and the second network utilizes these liquidations to derive resultant equilibrium prices. This data-driven approach can capture both linear and non-linear forms without pre-specifying an analytical structure; furthermore, it functions effectively even in the absence of observable liquidation data. Experiments with simulated datasets demonstrate that our model can accurately predict equilibrium asset prices based solely on initial shocks, while revealing a strong alignment between predicted and true liquidations. Our explainable framework contributes to the understanding and modeling of price-mediated contagion and provides valuable insights for financial authorities to construct effective stress tests and regulatory policies.

Stochastic Cell Transmission Models of Traffic Networks

Apr 23, 2023

We introduce a rigorous framework for stochastic cell transmission models for general traffic networks. The performance of traffic systems is evaluated based on preference functionals and acceptable designs. The numerical implementation combines simulation, Gaussian process regression, and a stochastic exploration procedure. The approach is illustrated in two case studies.

Optimal Network Compression

Aug 20, 2020

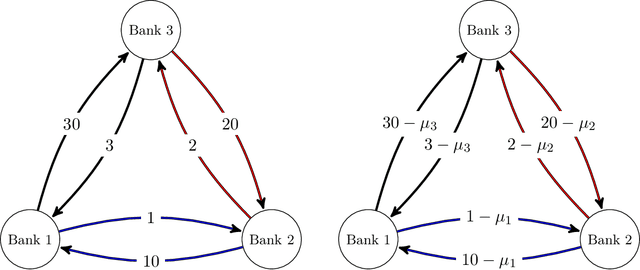

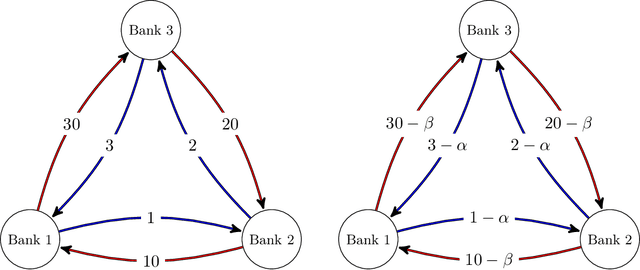

This paper introduces a formulation of the optimal network compression problem for financial systems. This general formulation is presented for different levels of network compression or rerouting allowed from the initial interbank network. We prove that this problem is, generically, NP-hard. We focus on objective functions generated by systemic risk measures under systematic shocks to the financial network. We conclude by studying the optimal compression problem for specific networks; this permits us to study the so-called robust fragility of certain network topologies more generally as well as the potential benefits and costs of network compression.