Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeMonotonic Neural Ordinary Differential Equation: Time-series Forecasting for Cumulative Data

Sep 23, 2023

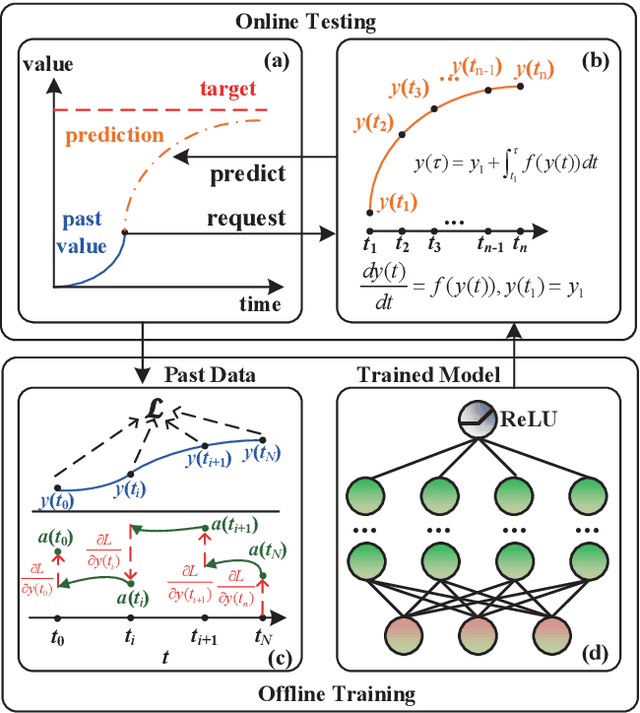

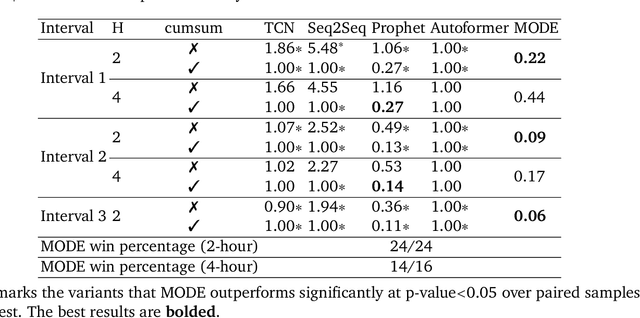

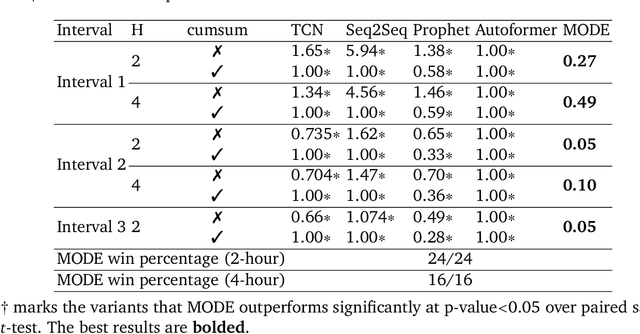

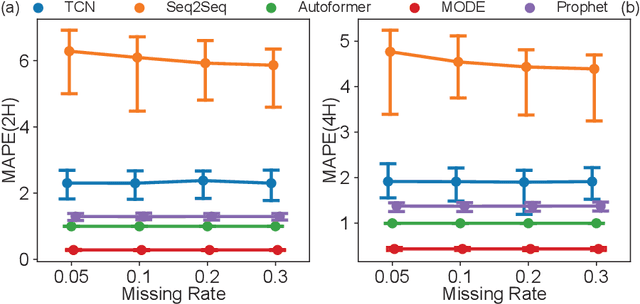

Time-Series Forecasting based on Cumulative Data (TSFCD) is a crucial problem in decision-making across various industrial scenarios. However, existing time-series forecasting methods often overlook two important characteristics of cumulative data, namely monotonicity and irregularity, which limit their practical applicability. To address this limitation, we propose a principled approach called Monotonic neural Ordinary Differential Equation (MODE) within the framework of neural ordinary differential equations. By leveraging MODE, we are able to effectively capture and represent the monotonicity and irregularity in practical cumulative data. Through extensive experiments conducted in a bonus allocation scenario, we demonstrate that MODE outperforms state-of-the-art methods, showcasing its ability to handle both monotonicity and irregularity in cumulative data and delivering superior forecasting performance.