Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRepetitive Contrastive Learning Enhances Mamba's Selectivity in Time Series Prediction

Apr 12, 2025Long sequence prediction is a key challenge in time series forecasting. While Mamba-based models have shown strong performance due to their sequence selection capabilities, they still struggle with insufficient focus on critical time steps and incomplete noise suppression, caused by limited selective abilities. To address this, we introduce Repetitive Contrastive Learning (RCL), a token-level contrastive pretraining framework aimed at enhancing Mamba's selective capabilities. RCL pretrains a single Mamba block to strengthen its selective abilities and then transfers these pretrained parameters to initialize Mamba blocks in various backbone models, improving their temporal prediction performance. RCL uses sequence augmentation with Gaussian noise and applies inter-sequence and intra-sequence contrastive learning to help the Mamba module prioritize information-rich time steps while ignoring noisy ones. Extensive experiments show that RCL consistently boosts the performance of backbone models, surpassing existing methods and achieving state-of-the-art results. Additionally, we propose two metrics to quantify Mamba's selective capabilities, providing theoretical, qualitative, and quantitative evidence for the improvements brought by RCL.

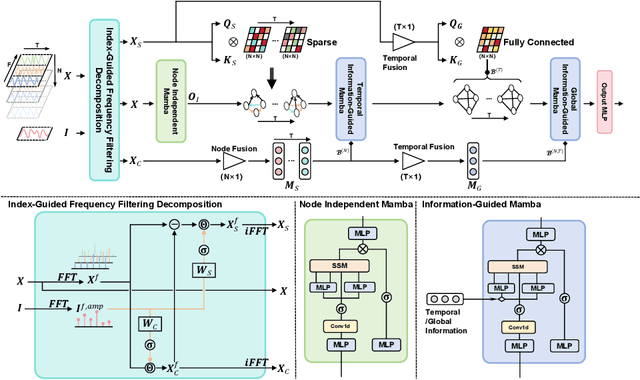

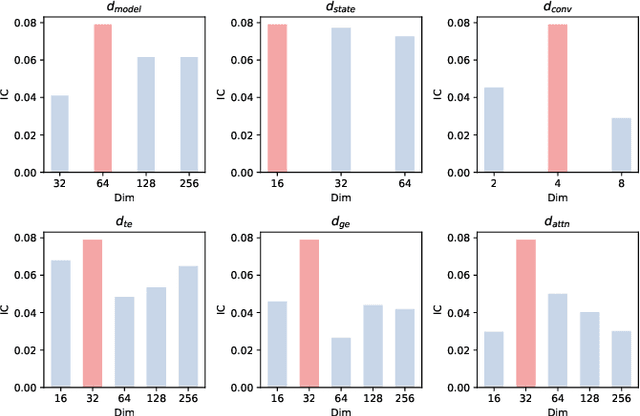

Hierarchical Information-Guided Spatio-Temporal Mamba for Stock Time Series Forecasting

Mar 14, 2025

Mamba has demonstrated excellent performance in various time series forecasting tasks due to its superior selection mechanism. Nevertheless, conventional Mamba-based models encounter significant challenges in accurately predicting stock time series, as they fail to adequately capture both the overarching market dynamics and the intricate interdependencies among individual stocks. To overcome these constraints, we introduce the Hierarchical Information-Guided Spatio-Temporal Mamba (HIGSTM) framework. HIGSTM introduces Index-Guided Frequency Filtering Decomposition to extract commonality and specificity from time series. The model architecture features a meticulously designed hierarchical framework that systematically captures both temporal dynamic patterns and global static relationships within the stock market. Furthermore, we propose an Information-Guided Mamba that integrates macro informations into the sequence selection process, thereby facilitating more market-conscious decision-making. Comprehensive experimental evaluations conducted on the CSI500, CSI800 and CSI1000 datasets demonstrate that HIGSTM achieves state-of-the-art performance.

TCGPN: Temporal-Correlation Graph Pre-trained Network for Stock Forecasting

Jul 26, 2024Recently, the incorporation of both temporal features and the correlation across time series has become an effective approach in time series prediction. Spatio-Temporal Graph Neural Networks (STGNNs) demonstrate good performance on many Temporal-correlation Forecasting Problem. However, when applied to tasks lacking periodicity, such as stock data prediction, the effectiveness and robustness of STGNNs are found to be unsatisfactory. And STGNNs are limited by memory savings so that cannot handle problems with a large number of nodes. In this paper, we propose a novel approach called the Temporal-Correlation Graph Pre-trained Network (TCGPN) to address these limitations. TCGPN utilize Temporal-correlation fusion encoder to get a mixed representation and pre-training method with carefully designed temporal and correlation pre-training tasks. Entire structure is independent of the number and order of nodes, so better results can be obtained through various data enhancements. And memory consumption during training can be significantly reduced through multiple sampling. Experiments are conducted on real stock market data sets CSI300 and CSI500 that exhibit minimal periodicity. We fine-tune a simple MLP in downstream tasks and achieve state-of-the-art results, validating the capability to capture more robust temporal correlation patterns.