Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeHierarchical Information-Guided Spatio-Temporal Mamba for Stock Time Series Forecasting

Paper and Code

Mar 14, 2025

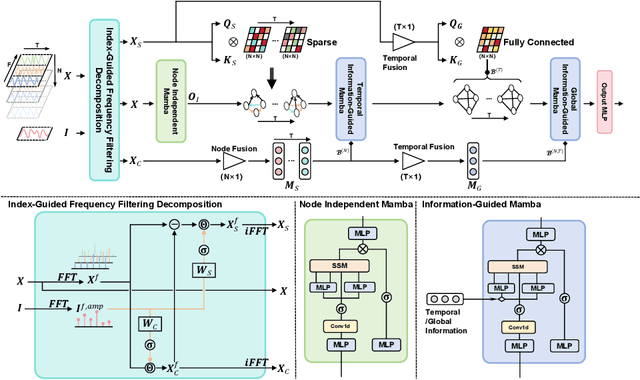

Mamba has demonstrated excellent performance in various time series forecasting tasks due to its superior selection mechanism. Nevertheless, conventional Mamba-based models encounter significant challenges in accurately predicting stock time series, as they fail to adequately capture both the overarching market dynamics and the intricate interdependencies among individual stocks. To overcome these constraints, we introduce the Hierarchical Information-Guided Spatio-Temporal Mamba (HIGSTM) framework. HIGSTM introduces Index-Guided Frequency Filtering Decomposition to extract commonality and specificity from time series. The model architecture features a meticulously designed hierarchical framework that systematically captures both temporal dynamic patterns and global static relationships within the stock market. Furthermore, we propose an Information-Guided Mamba that integrates macro informations into the sequence selection process, thereby facilitating more market-conscious decision-making. Comprehensive experimental evaluations conducted on the CSI500, CSI800 and CSI1000 datasets demonstrate that HIGSTM achieves state-of-the-art performance.