Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeGenerative Adversarial Network (GAN) and Enhanced Root Mean Square Error (ERMSE): Deep Learning for Stock Price Movement Prediction

Nov 30, 2021

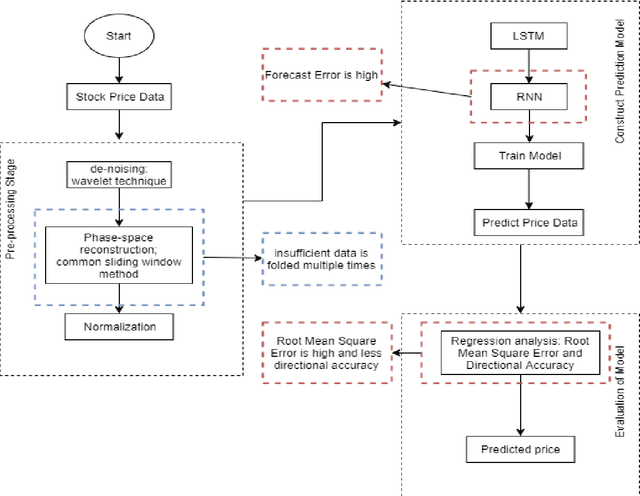

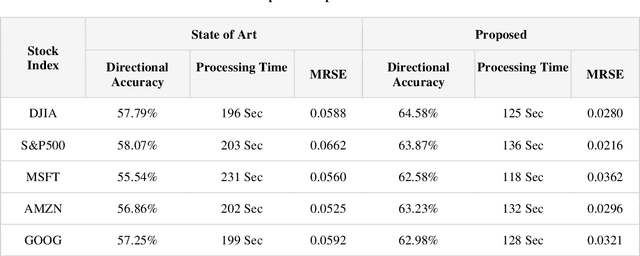

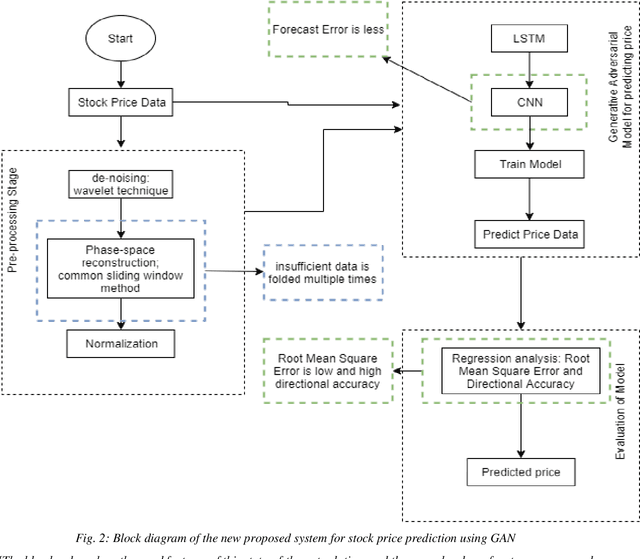

The prediction of stock price movement direction is significant in financial circles and academic. Stock price contains complex, incomplete, and fuzzy information which makes it an extremely difficult task to predict its development trend. Predicting and analysing financial data is a nonlinear, time-dependent problem. With rapid development in machine learning and deep learning, this task can be performed more effectively by a purposely designed network. This paper aims to improve prediction accuracy and minimizing forecasting error loss through deep learning architecture by using Generative Adversarial Networks. It was proposed a generic model consisting of Phase-space Reconstruction (PSR) method for reconstructing price series and Generative Adversarial Network (GAN) which is a combination of two neural networks which are Long Short-Term Memory (LSTM) as Generative model and Convolutional Neural Network (CNN) as Discriminative model for adversarial training to forecast the stock market. LSTM will generate new instances based on historical basic indicators information and then CNN will estimate whether the data is predicted by LSTM or is real. It was found that the Generative Adversarial Network (GAN) has performed well on the enhanced root mean square error to LSTM, as it was 4.35% more accurate in predicting the direction and reduced processing time and RMSE by 78 secs and 0.029, respectively. This study provides a better result in the accuracy of the stock index. It seems that the proposed system concentrates on minimizing the root mean square error and processing time and improving the direction prediction accuracy, and provides a better result in the accuracy of the stock index.