Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeOn the Identifiability of Regime-Switching Models with Multi-Lag Dependencies

Jan 06, 2026Identifiability is central to the interpretability of deep latent variable models, ensuring parameterisations are uniquely determined by the data-generating distribution. However, it remains underexplored for deep regime-switching time series. We develop a general theoretical framework for multi-lag Regime-Switching Models (RSMs), encompassing Markov Switching Models (MSMs) and Switching Dynamical Systems (SDSs). For MSMs, we formulate the model as a temporally structured finite mixture and prove identifiability of both the number of regimes and the multi-lag transitions in a nonlinear-Gaussian setting. For SDSs, we establish identifiability of the latent variables up to permutation and scaling via temporal structure, which in turn yields conditions for identifiability of regime-dependent latent causal graphs (up to regime/node permutations). Our results hold in a fully unsupervised setting through architectural and noise assumptions that are directly enforceable via neural network design. We complement the theory with a flexible variational estimator that satisfies the assumptions and validate the results on synthetic benchmarks. Across real-world datasets from neuroscience, finance, and climate, identifiability leads to more trustworthy interpretability analysis, which is crucial for scientific discovery.

Data-driven analysis of central bank digital currency projects drivers

Feb 23, 2021

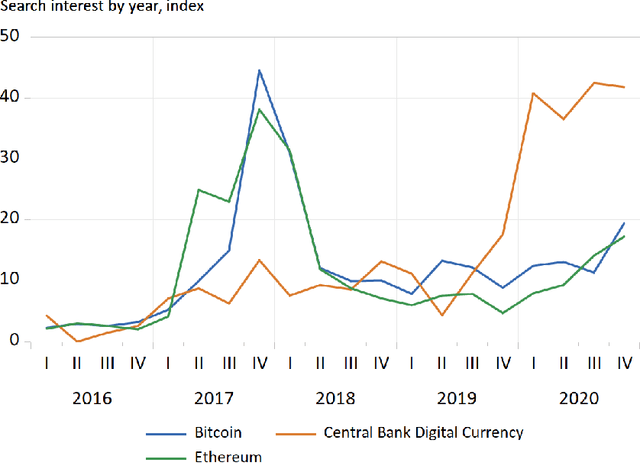

In this paper, we use a variety of machine learning methods to quantify the extent to which economic and technological factors are predictive of the progression of Central Bank Digital Currencies (CBDC) within a country, using as our measure of this progression the CBDC project index (CBDCPI). We find that a financial development index is the most important feature for our model, followed by the GDP per capita and an index of the voice and accountability of the country's population. Our results are consistent with previous qualitative research which finds that countries with a high degree of financial development or digital infrastructure have more developed CBDC projects. Further, we obtain robust results when predicting the CBDCPI at different points in time.