Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeA Few-Shot LLM Framework for Extreme Day Classification in Electricity Markets

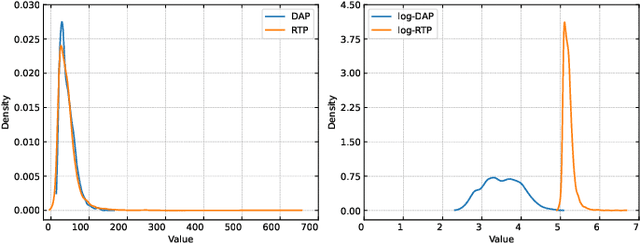

Feb 17, 2026This paper proposes a few-shot classification framework based on Large Language Models (LLMs) to predict whether the next day will have spikes in real-time electricity prices. The approach aggregates system state information, including electricity demand, renewable generation, weather forecasts, and recent electricity prices, into a set of statistical features that are formatted as natural-language prompts and fed to an LLM along with general instructions. The model then determines the likelihood that the next day would be a spike day and reports a confidence score. Using historical data from the Texas electricity market, we demonstrate that this few-shot approach achieves performance comparable to supervised machine learning models, such as Support Vector Machines and XGBoost, and outperforms the latter two when limited historical data are available. These findings highlight the potential of LLMs as a data-efficient tool for classifying electricity price spikes in settings with scarce data.

Conformal Uncertainty Quantification of Electricity Price Predictions for Risk-Averse Storage Arbitrage

Dec 10, 2024

This paper proposes a risk-averse approach to energy storage price arbitrage, leveraging conformal uncertainty quantification for electricity price predictions. The method addresses the significant challenges posed by the inherent volatility and uncertainty of real-time electricity prices, which create substantial risks of financial losses for energy storage participants relying on future price forecasts to plan their operations. The framework comprises a two-layer prediction model to quantify real-time price uncertainty confidence intervals with high coverage. The framework is distribution-free and can work with any underlying point prediction model. We evaluate the quantification effectiveness through storage price arbitrage application by managing the risk of participating in the real-time market. We design a risk-averse policy for profit-maximization of energy storage arbitrage to find the safest storage schedule with very minimal losses. Using historical data from New York State and synthetic price predictions, our evaluations demonstrate that this framework can achieve good profit margins with less than $35\%$ purchases.

Energy Storage Arbitrage in Two-settlement Markets: A Transformer-Based Approach

Apr 26, 2024

This paper presents an integrated model for bidding energy storage in day-ahead and real-time markets to maximize profits. We show that in integrated two-stage bidding, the real-time bids are independent of day-ahead settlements, while the day-ahead bids should be based on predicted real-time prices. We utilize a transformer-based model for real-time price prediction, which captures complex dynamical patterns of real-time prices, and use the result for day-ahead bidding design. For real-time bidding, we utilize a long short-term memory-dynamic programming hybrid real-time bidding model. We train and test our model with historical data from New York State, and our results showed that the integrated system achieved promising results of almost a 20\% increase in profit compared to only bidding in real-time markets, and at the same time reducing the risk in terms of the number of days with negative profits.