Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeE-QRGMM: Efficient Generative Metamodeling for Covariate-Dependent Uncertainty Quantification

Jan 27, 2026Covariate-dependent uncertainty quantification in simulation-based inference is crucial for high-stakes decision-making but remains challenging due to the limitations of existing methods such as conformal prediction and classical bootstrap, which struggle with covariate-specific conditioning. We propose Efficient Quantile-Regression-Based Generative Metamodeling (E-QRGMM), a novel framework that accelerates the quantile-regression-based generative metamodeling (QRGMM) approach by integrating cubic Hermite interpolation with gradient estimation. Theoretically, we show that E-QRGMM preserves the convergence rate of the original QRGMM while reducing grid complexity from $O(n^{1/2})$ to $O(n^{1/5})$ for the majority of quantile levels, thereby substantially improving computational efficiency. Empirically, E-QRGMM achieves a superior trade-off between distributional accuracy and training speed compared to both QRGMM and other advanced deep generative models on synthetic and practical datasets. Moreover, by enabling bootstrap-based construction of confidence intervals for arbitrary estimands of interest, E-QRGMM provides a practical solution for covariate-dependent uncertainty quantification.

Conditional Generative Modeling for Enhanced Credit Risk Management in Supply Chain Finance

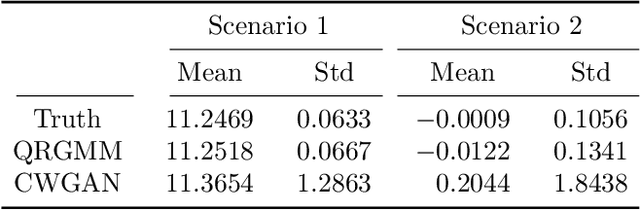

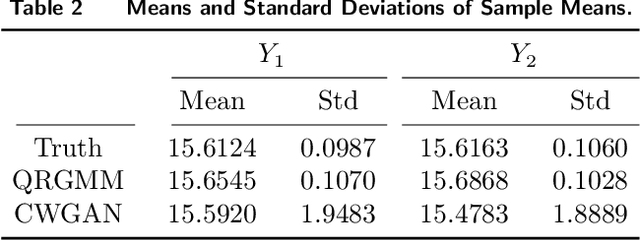

Jun 18, 2025The rapid expansion of cross-border e-commerce (CBEC) has created significant opportunities for small and medium-sized enterprises (SMEs), yet financing remains a critical challenge due to SMEs' limited credit histories. Third-party logistics (3PL)-led supply chain finance (SCF) has emerged as a promising solution, leveraging in-transit inventory as collateral. We propose an advanced credit risk management framework tailored for 3PL-led SCF, addressing the dual challenges of credit risk assessment and loan size determination. Specifically, we leverage conditional generative modeling of sales distributions through Quantile-Regression-based Generative Metamodeling (QRGMM) as the foundation for risk estimation. We propose a unified framework that enables flexible estimation of multiple risk measures while introducing a functional risk measure formulation that systematically captures the relationship between these risk measures and varying loan levels, supported by theoretical guarantees. To capture complex covariate interactions in e-commerce sales data, we integrate QRGMM with Deep Factorization Machines (DeepFM). Extensive experiments on synthetic and real-world data validate the efficacy of our model for credit risk assessment and loan size determination. This study represents a pioneering application of generative AI in CBEC SCF risk management, offering a solid foundation for enhanced credit practices and improved SME access to capital.

Learning to Simulate: Generative Metamodeling via Quantile Regression

Nov 29, 2023

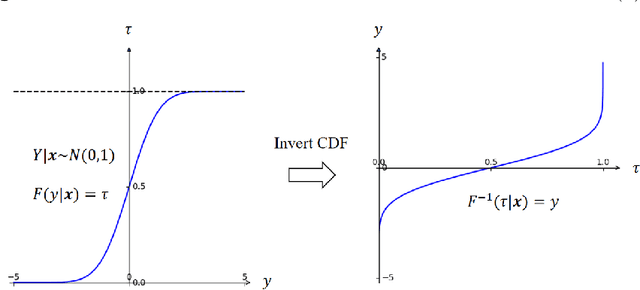

Stochastic simulation models, while effective in capturing the dynamics of complex systems, are often too slow to run for real-time decision-making. Metamodeling techniques are widely used to learn the relationship between a summary statistic of the outputs (e.g., the mean or quantile) and the inputs of the simulator, so that it can be used in real time. However, this methodology requires the knowledge of an appropriate summary statistic in advance, making it inflexible for many practical situations. In this paper, we propose a new metamodeling concept, called generative metamodeling, which aims to construct a "fast simulator of the simulator". This technique can generate random outputs substantially faster than the original simulation model, while retaining an approximately equal conditional distribution given the same inputs. Once constructed, a generative metamodel can instantaneously generate a large amount of random outputs as soon as the inputs are specified, thereby facilitating the immediate computation of any summary statistic for real-time decision-making. Furthermore, we propose a new algorithm -- quantile-regression-based generative metamodeling (QRGMM) -- and study its convergence and rate of convergence. Extensive numerical experiments are conducted to investigate the empirical performance of QRGMM, compare it with other state-of-the-art generative algorithms, and demonstrate its usefulness in practical real-time decision-making.