Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLearning ECG signal features without backpropagation

Jul 04, 2023

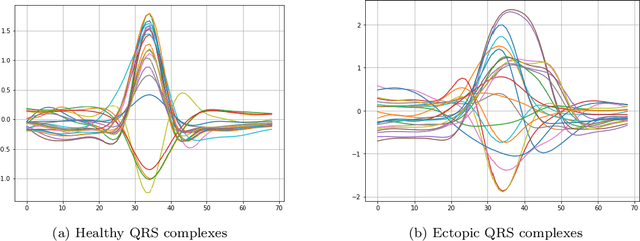

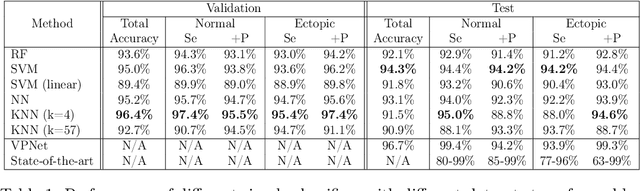

Representation learning has become a crucial area of research in machine learning, as it aims to discover efficient ways of representing raw data with useful features to increase the effectiveness, scope and applicability of downstream tasks such as classification and prediction. In this paper, we propose a novel method to generate representations for time series-type data. This method relies on ideas from theoretical physics to construct a compact representation in a data-driven way, and it can capture both the underlying structure of the data and task-specific information while still remaining intuitive, interpretable and verifiable. This novel methodology aims to identify linear laws that can effectively capture a shared characteristic among samples belonging to a specific class. By subsequently utilizing these laws to generate a classifier-agnostic representation in a forward manner, they become applicable in a generalized setting. We demonstrate the effectiveness of our approach on the task of ECG signal classification, achieving state-of-the-art performance.

Predicting the Price Movement of Cryptocurrencies Using Linear Law-based Transformation

Apr 27, 2023

The aim of this paper is to investigate the effect of a novel method called linear law-based feature space transformation (LLT) on the accuracy of intraday price movement prediction of cryptocurrencies. To do this, the 1-minute interval price data of Bitcoin, Ethereum, Binance Coin, and Ripple between 1 January 2019 and 22 October 2022 were collected from the Binance cryptocurrency exchange. Then, 14-hour nonoverlapping time windows were applied to sample the price data. The classification was based on the first 12 hours, and the two classes were determined based on whether the closing price rose or fell after the next 2 hours. These price data were first transformed with the LLT, then they were classified by traditional machine learning algorithms with 10-fold cross-validation. Based on the results, LLT greatly increased the accuracy for all cryptocurrencies, which emphasizes the potential of the LLT algorithm in predicting price movements.

LLT: An R package for Linear Law-based Feature Space Transformation

Apr 27, 2023

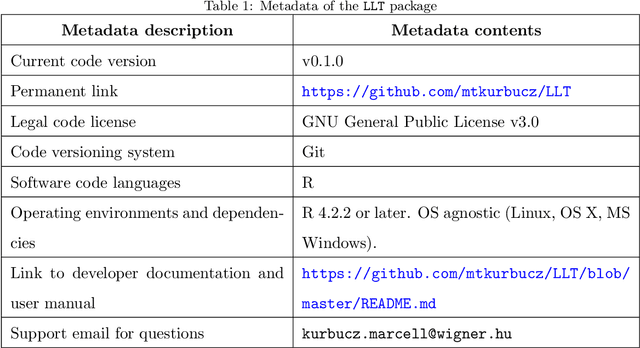

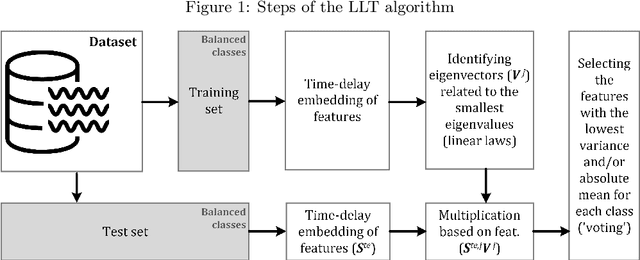

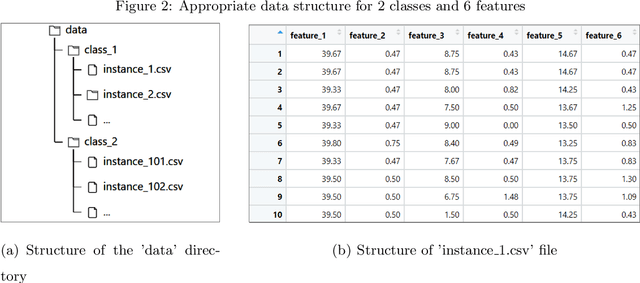

The goal of the linear law-based feature space transformation (LLT) algorithm is to assist with the classification of univariate and multivariate time series. The presented R package, called LLT, implements this algorithm in a flexible yet user-friendly way. This package first splits the instances into training and test sets. It then utilizes time-delay embedding and spectral decomposition techniques to identify the governing patterns (called linear laws) of each input sequence (initial feature) within the training set. Finally, it applies the linear laws of the training set to transform the initial features of the test set. These steps are performed by three separate functions called trainTest, trainLaw, and testTrans. Their application requires a predefined data structure; however, for fast calculation, they use only built-in functions. The LLT R package and a sample dataset with the appropriate data structure are publicly available on GitHub.

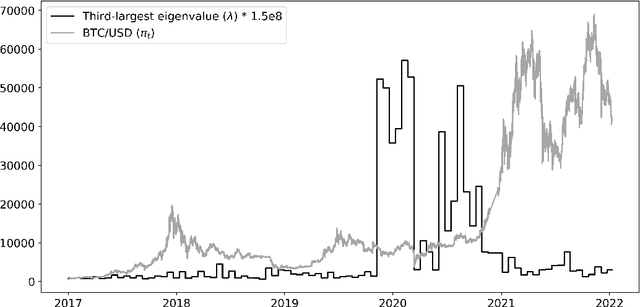

Linear Laws of Markov Chains with an Application for Anomaly Detection in Bitcoin Prices

Jan 24, 2022

The goals of this paper are twofold: (1) to present a new method that is able to find linear laws governing the time evolution of Markov chains and (2) to apply this method for anomaly detection in Bitcoin prices. To accomplish these goals, first, the linear laws of Markov chains are derived by using the time embedding of their (categorical) autocorrelation function. Then, a binary series is generated from the first difference of Bitcoin exchange rate (against the United States Dollar). Finally, the minimum number of parameters describing the linear laws of this series is identified through stepped time windows. Based on the results, linear laws typically became more complex (containing an additional third parameter that indicates hidden Markov property) in two periods: before the crash of cryptocurrency markets inducted by the COVID-19 pandemic (12 March 2020), and before the record-breaking surge in the price of Bitcoin (Q4 2020 - Q1 2021). In addition, the locally high values of this third parameter are often related to short-term price peaks, which suggests price manipulation.