Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeSovereign-by-Design A Reference Architecture for AI and Blockchain Enabled Systems

Feb 05, 2026Digital sovereignty has emerged as a central concern for modern software-intensive systems, driven by the dominance of non-sovereign cloud infrastructures, the rapid adoption of Generative AI, and increasingly stringent regulatory requirements. While existing initiatives address governance, compliance, and security in isolation, they provide limited guidance on how sovereignty can be operationalized at the architectural level. In this paper, we argue that sovereignty must be treated as a first-class architectural property rather than a purely regulatory objective. We introduce a Sovereign Reference Architecture that integrates self-sovereign identity, blockchain-based trust and auditability, sovereign data governance, and Generative AI deployed under explicit architectural control. The architecture explicitly captures the dual role of Generative AI as both a source of governance risk and an enabler of compliance, accountability, and continuous assurance when properly constrained. By framing sovereignty as an architectural quality attribute, our work bridges regulatory intent and concrete system design, offering a coherent foundation for building auditable, evolvable, and jurisdiction-aware AI-enabled systems. The proposed reference architecture provides a principled starting point for future research and practice at the intersection of software architecture, Generative AI, and digital sovereignty.

Forecasting Bitcoin closing price series using linear regression and neural networks models

Jan 04, 2020

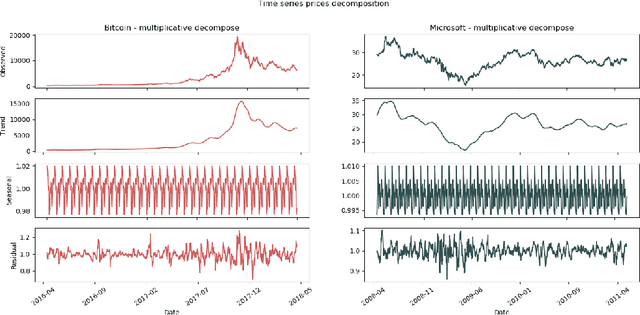

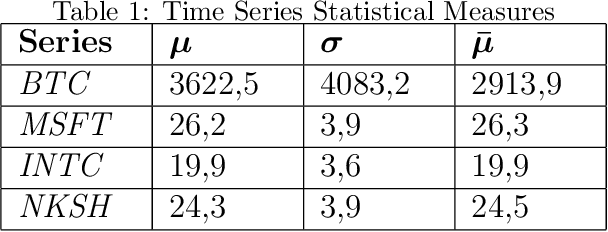

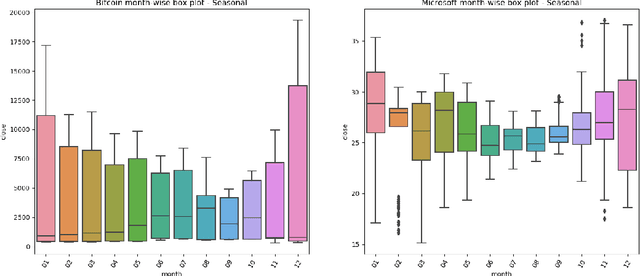

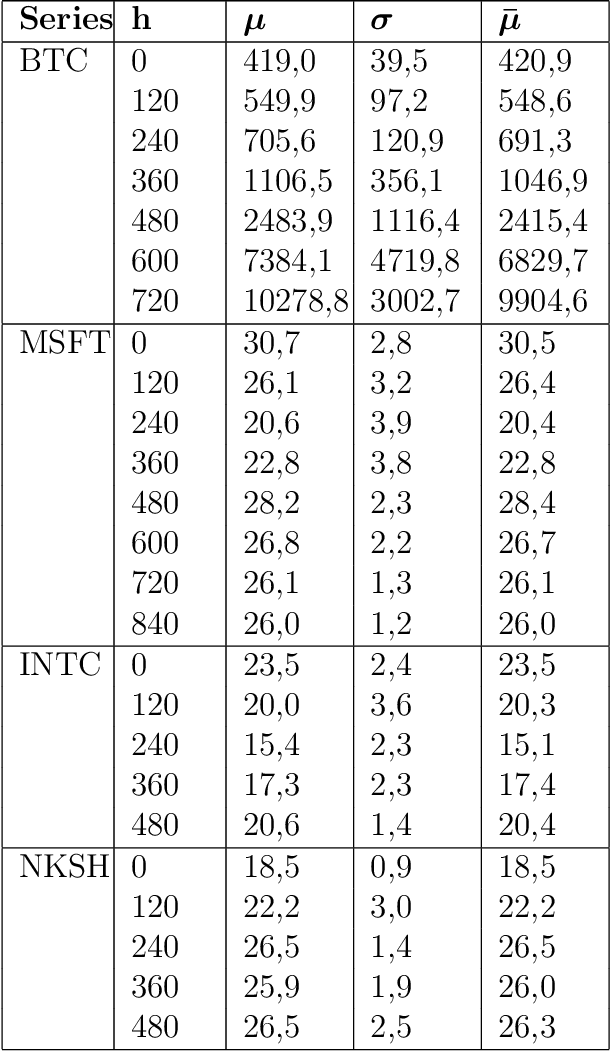

This paper studies how to forecast daily closing price series of Bitcoin, using data on prices and volumes of prior days. Bitcoin price behaviour is still largely unexplored, presenting new opportunities. We compared our results with two modern works on Bitcoin prices forecasting and with a well-known recent paper that uses Intel, National Bank shares and Microsoft daily NASDAQ closing prices spanning a 3-year interval. We followed different approaches in parallel, implementing both statistical techniques and machine learning algorithms. The SLR model for univariate series forecast uses only closing prices, whereas the MLR model for multivariate series uses both price and volume data. We applied the ADF -Test to these series, which resulted to be indistinguishable from a random walk. We also used two artificial neural networks: MLP and LSTM. We then partitioned the dataset into shorter sequences, representing different price regimes, obtaining best result using more than one previous price, thus confirming our regime hypothesis. All the models were evaluated in terms of MAPE and relativeRMSE. They performed well, and were overall better than those obtained in the benchmarks. Based on the results, it was possible to demonstrate the efficacy of the proposed methodology and its contribution to the state-of-the-art.