Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeTime-series Anomaly Detection via Contextual Discriminative Contrastive Learning

Apr 16, 2023

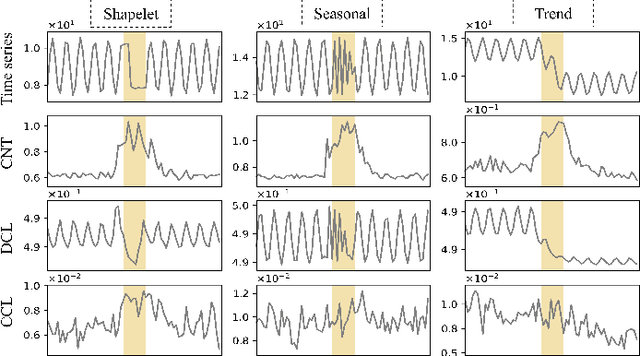

Detecting anomalies in temporal data is challenging due to anomalies being dependent on temporal dynamics. One-class classification methods are commonly used for anomaly detection tasks, but they have limitations when applied to temporal data. In particular, mapping all normal instances into a single hypersphere to capture their global characteristics can lead to poor performance in detecting context-based anomalies where the abnormality is defined with respect to local information. To address this limitation, we propose a novel approach inspired by the loss function of DeepSVDD. Instead of mapping all normal instances into a single hypersphere center, each normal instance is pulled toward a recent context window. However, this approach is prone to a representation collapse issue where the neural network that encodes a given instance and its context is optimized towards a constant encoder solution. To overcome this problem, we combine our approach with a deterministic contrastive loss from Neutral AD, a promising self-supervised learning anomaly detection approach. We provide a theoretical analysis to demonstrate that the incorporation of the deterministic contrastive loss can effectively prevent the occurrence of a constant encoder solution. Experimental results show superior performance of our model over various baselines and model variants on real-world industrial datasets.

Multivariate Time Series Anomaly Detection via Dynamic Graph Forecasting

Feb 04, 2023Anomalies in univariate time series often refer to abnormal values and deviations from the temporal patterns from majority of historical observations. In multivariate time series, anomalies also refer to abnormal changes in the inter-series relationship, such as correlation, over time. Existing studies have been able to model such inter-series relationships through graph neural networks. However, most works settle on learning a static graph globally or within a context window to assist a time series forecasting task or a reconstruction task, whose objective is not tailored to explicitly detect the abnormal relationship. Some other works detect anomalies based on reconstructing or forecasting a list of inter-series graphs, which inadvertently weakens their power to capture temporal patterns within the data due to the discrete nature of graphs. In this study, we propose DyGraphAD, a multivariate time series anomaly detection framework based upon a list of dynamic inter-series graphs. The core idea is to detect anomalies based on the deviation of inter-series relationships and intra-series temporal patterns from normal to anomalous states, by leveraging the evolving nature of the graphs in order to assist a graph forecasting task and a time series forecasting task simultaneously. Our numerical experiments on real-world datasets demonstrate that DyGraphAD has superior performance than baseline anomaly detection approaches.

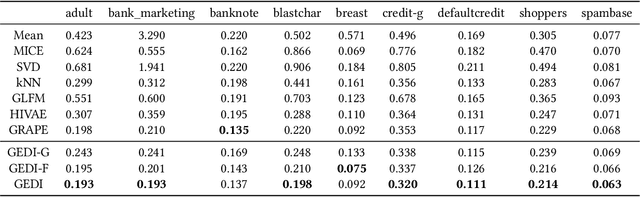

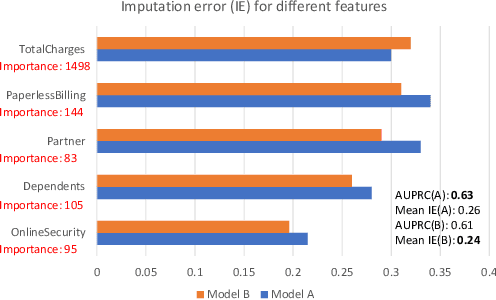

GEDI: A Graph-based End-to-end Data Imputation Framework

Aug 13, 2022

Data imputation is an effective way to handle missing data, which is common in practical applications. In this study, we propose and test a novel data imputation process that achieve two important goals: (1) preserve the row-wise similarities among observations and column-wise contextual relationships among features in the feature matrix, and (2) tailor the imputation process to specific downstream label prediction task. The proposed imputation process uses Transformer network and graph structure learning to iteratively refine the contextual relationships among features and similarities among observations. Moreover, it uses a meta-learning framework to select features that are influential to the downstream prediction task of interest. We conduct experiments on real-world large data sets, and show that the proposed imputation process consistently improves imputation and label prediction performance over a variety of benchmark methods.