Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLabel Unbalance in High-frequency Trading

Mar 13, 2025

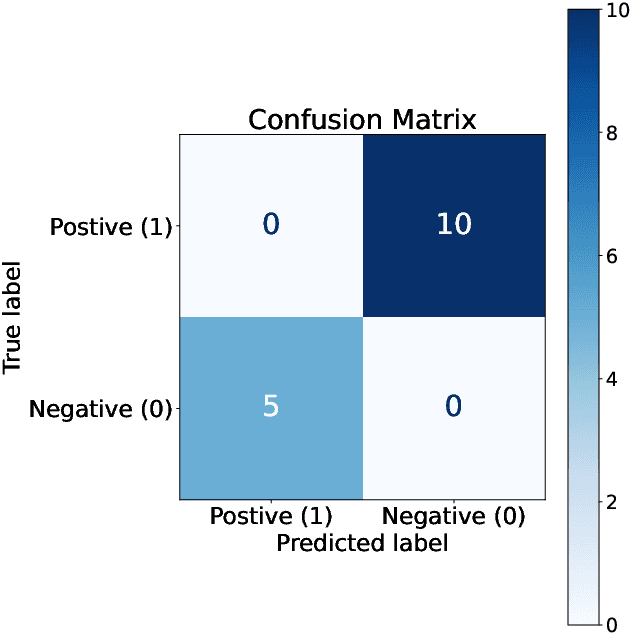

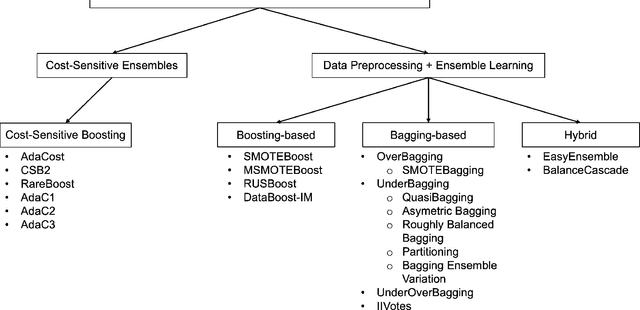

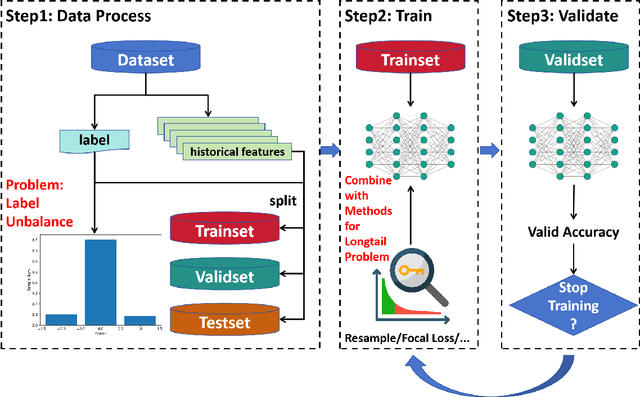

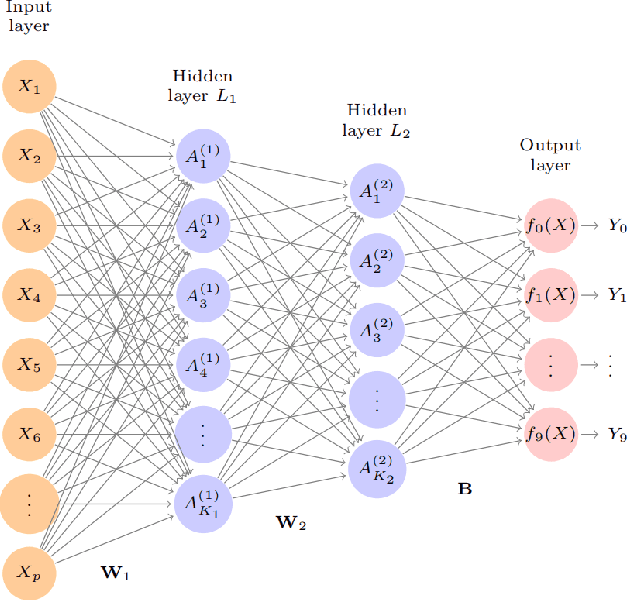

In financial trading, return prediction is one of the foundation for a successful trading system. By the fast development of the deep learning in various areas such as graphical processing, natural language, it has also demonstrate significant edge in handling with financial data. While the success of the deep learning relies on huge amount of labeled sample, labeling each time/event as profitable or unprofitable, under the transaction cost, especially in the high-frequency trading world, suffers from serious label imbalance issue.In this paper, we adopts rigurious end-to-end deep learning framework with comprehensive label imbalance adjustment methods and succeed in predicting in high-frequency return in the Chinese future market. The code for our method is publicly available at https://github.com/RS2002/Label-Unbalance-in-High-Frequency-Trading .